Worried About Rising Rates? Here’s Why You Shouldn’t Be

Should tighter monetary policy on both sides of the Atlantic worry bond investors? We don’t think so. Bonds have historically delivered positive returns when interest rates rise—particularly when they rise gradually.

Of course, we appreciate investors’ concerns. After the global financial crisis, central banks provided unprecedented life support for markets and the global economy by cutting interest rates to record lows and buying trillions of dollars’ worth of bonds. Ending such massive monetary stimulus won’t be easy.

But that doesn’t mean it has to be painful or disruptive, either. We expect central banks to withdraw this extraordinary support very slowly.

Interest rates are rising in the US, but the Federal Reserve is moving at a snail’s pace—it has hiked rates just four times in 18 months. The Fed will probably reduce its balance sheet slowly, too—likely by letting some of its bonds mature each month without reinvesting the proceeds. Fed Chair Janet Yellen predicted that the reduction, far from roiling markets, would be about as exciting as “watching paint dry.”

The European Central Bank, meanwhile, is nowhere near ready to raise interest rates. But with eurozone growth improving, it has signaled that it may soon begin reducing the amount of bonds it buys each month. Again, though, we expect that policymakers will be in no hurry to end purchases altogether.

WHY YOU SHOULD WANT RATES TO RISE

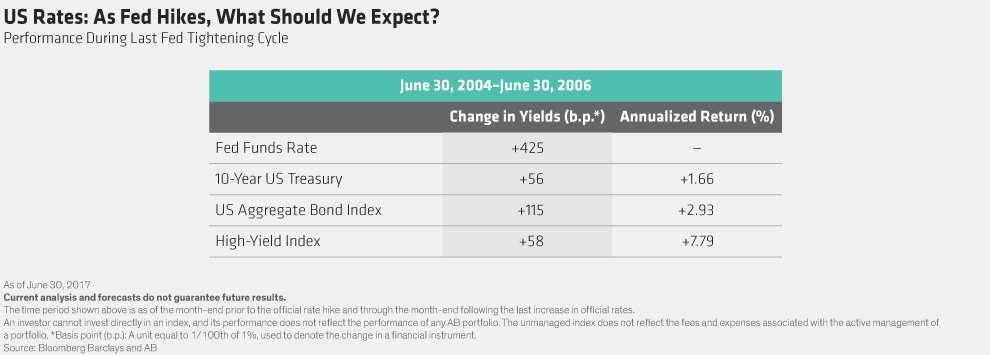

To get a sense of what might be in store for the bond market, it helps to recall the Fed’s last tightening cycle, where 17 quarter-percentage-point rate hikes were spread over a two-year period. Both the 10-year US Treasury Index and the US high-yield bond market produced positive annualized returns (Display).

How was this possible? Aren’t bonds highly sensitive to interest-rate movements? Yes, but as long as they don’t default, bonds also produce a steady stream of income. And when rates rise, investors can reinvest the proceeds of their maturing bonds in newer—and higher-yielding—bonds. This often outweighs any short-term losses from rising rates and increases total return.

In other words, investors who rely on their bond portfolios to provide income over a long time period should be rooting for higher rates.

A rapid—and unexpected—rise in rates can be harder for investors to navigate. In 1994, inflation worries prompted the Fed to lift rates at a much faster clip over a shorter period of time—and without advance notice. The 10-year US Treasury Index lost nearly 4% during that cycle.

US high yield, however, was up 1.4%—evidence that active bond managers can still deliver positive returns even when Treasury prices fall, by using insights on valuation and credit quality to choose bonds that can withstand broader market downturns.