Weighing the Week Ahead: What Can be Done to Create More Jobs at Better Pay?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWe have the biggest data calendar of the year, climaxing with the employment report. It is right before the Labor Day weekend. It is a natural setup for politicians and pundits alike. Expect many to be asking:

How Can We Create More Jobs and Better Pay?

Last Week Recap

My expectation that last week would focus on the state of the economic policy agenda was pretty accurate. While the overall weekly change in the market was modest, the moves came from an evaluation of the agenda potential. Monday saw an expectation of more Congressional cooperation. Tuesday night’s campaign-style speech brought fears of a government shutdown. The economic announcements, while pretty good, seemed to have little effect on trading.

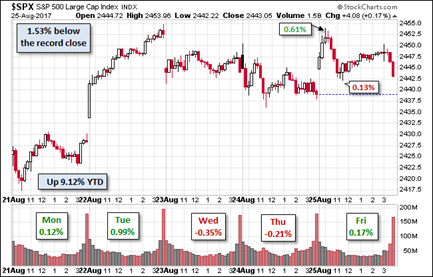

The Story in One Chart

I always start my personal review of the week by looking at this great chart from Doug Short via Jill Mislinski. She notes the overall weekly gain of 0.73% as well as the relationship to the record close and the daily action. The only thing missing? Highlights noting the tweet of the day!

Doug has a special knack for pulling together all the relevant information. His charts save more than a thousand words! Read the entire post for several more charts providing long-term perspective, including the size and frequency of drawdowns.

The Silver Bullet

As I indicated recently I am moving the Silver Bullet award to a standalone feature, rather than an item in WTWA. I hope that readers and past winners, listed here, will help me in giving special recognition to those who help to keep data honest. As always, nominations are welcome!

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

The economic news last week was generally positive. Even those that missed expectations were not too bad.

The Good

-

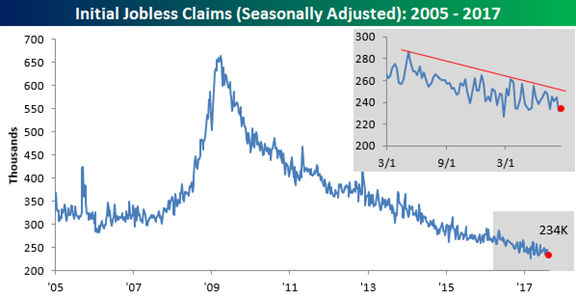

Initial jobless claims remain low. Bespoke notes that anything below 300K used to be regarded as very good. Now, they say, 250K is the new 300K.

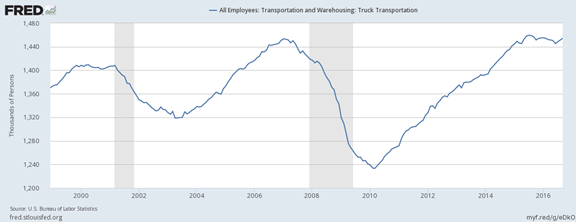

- Railroad traffic has improved on key metrics. Steven Hansen (GEI) provides his customary thorough look. He also analyzes the improvement in truck traffic, describing and comparing several competing indicators. Check out his reasons for preferring the CASS index, including the consistency with sector employment.

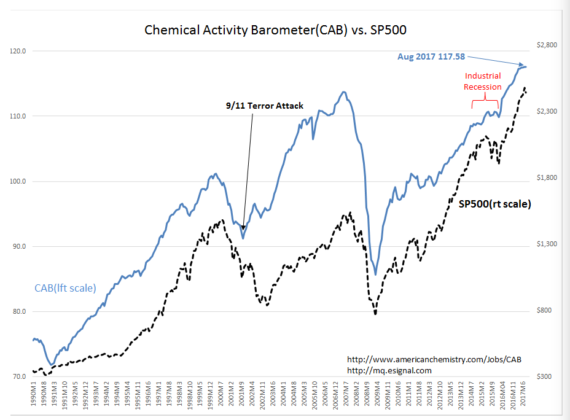

- Chemical activity barometer shows continued strength. “Davidson” (via Todd Sullivan) follows this closely, showing the relationship with other important indicators. This chart shows why understanding the economy is critical to understanding stock prices, but the full article is well worth a read.

- Sentiment has turned more bearish (a contrary indicator). Charts and analysis from David Templeton at HORAN.

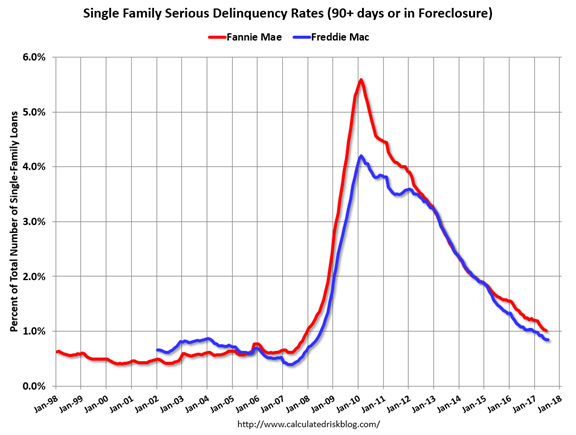

- The serious mortgage delinquency rate remains low, close to long-term normal levels at 0.85%. (Calculated Risk). Foreclosure inventory is below 400,000 for the first time since 2007.

- The earnings picture remains strong. Dr. Ed Yardeni’s recent post confirms Brian Gilmartin’s analysis, frequently reported here. Yardeni writes:

- S&P 500 forward revenues per share, which tends to be a weekly coincident indicator of actual earnings, continued its linear ascent into record-high territory through the week of August 10.

- S&P 500 forward operating earnings per share, which works well as a 52-week leading indicator of four-quarter-trailing operating earnings, has gone vertical since March 2016. It works great during economic expansions, but terribly during recessions. If there is no recession in sight, then the prediction of this indicator is that four-quarter-trailing earnings per share is heading from $126 currently (through Q2) to $140 over the next four quarters.

The Bad

-

New home sales declined to a SAAR of 571K, missing expectations of 615K and down from 630K in June. New Deal Democrat views this as part of a larger decline – no high in the 3-month moving average since March.Calculated Risk notes the large increase in values for the prior three months and calls this a “decent report.”

-

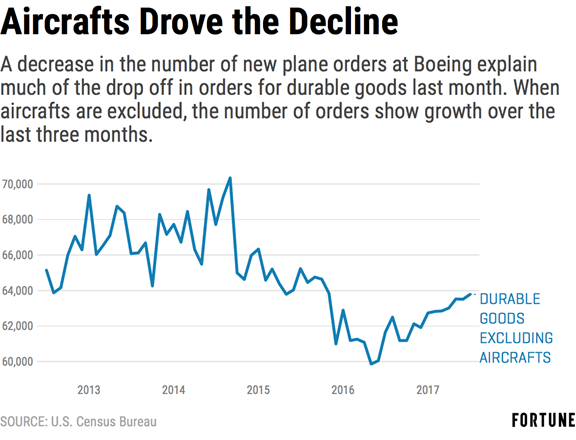

Durable goods declined dramatically over the prior month, down 6.8% instead of up 6.4%. The series is less volatile when you look at the ex-transportation value. That was an increase of 0.5%, in line with expectations. As Fortune explains, the big change was due to Boeing effects. Here is the history ex-aircraft.

-

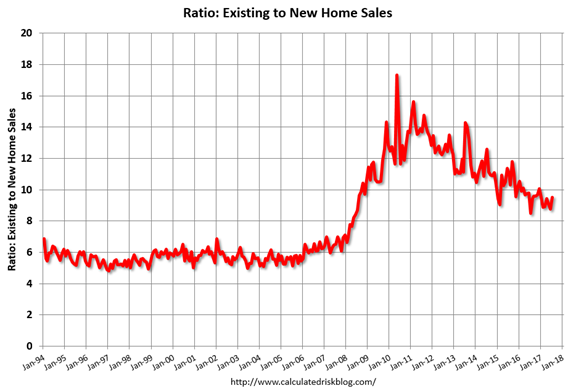

Existing home sales recorded a SAAR of 5.44M, a decline from 5.51 million. This also missed expectations by the same margin. Analysts site low inventory levels as the biggest factor in slow sales. Calculated Risk has a first-rate explanation of the linkage between new and existing sales. One needs to understand the effect of foreclosures, the rate and price of new construction, and the relationship for the existing sale market. The easiest way to see this is this chart, where Bill expects a gradual reduction to long-term levels. It has been a slow and gradual process.

The Ugly

Traffickers using Facebook video of torture to extort ransoms from migrant families. The Sunday Times (London).

And an update on the shoddy care within “five-star” addiction centers. (Stat)

Noteworthy

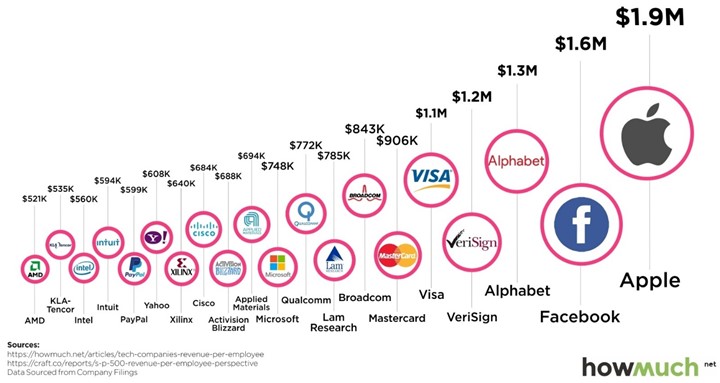

A two-part question that is enjoyable and revealing (no peeking). First, what are three technology companies in terms of revenue per employee. Not earnings, revenue). Second, what is this level? Mrs. OldProf nailed two of the top three, but even she missed on the level of revenue per employee. This is not a metric most people think about. How did you do?

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

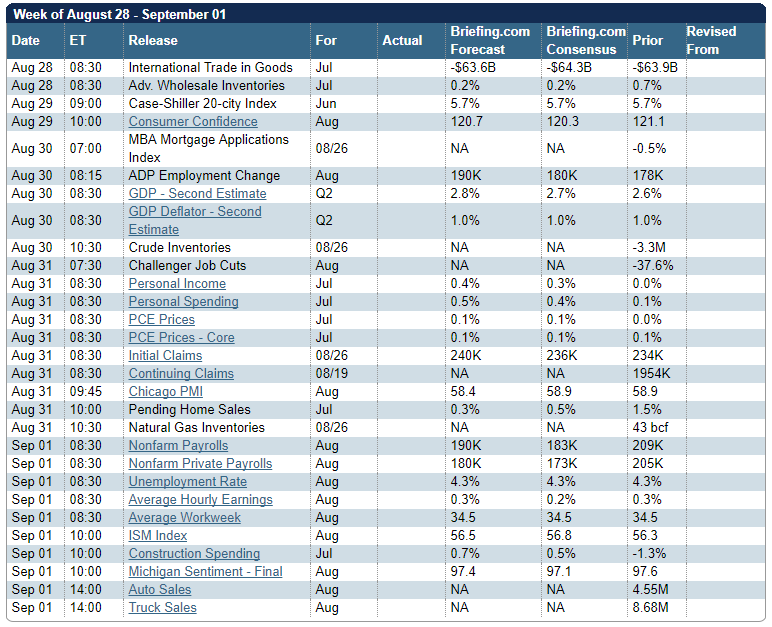

The Calendar

We have a jam-packed economic calendar, probably the biggest of the year. Personal income and spending, auto sales, and consumer confidence readings are all important. The employment report claims the spotlight on Friday, with the ADP private employment change announced Wednesday.

President Trump is expected to visit Texas, and also to kick off his campaign for tax reform with a trip to Missouri.

Briefing.com has a good U.S. economic calendar for the week (and many other good features which I monitor each day). Here are the main U.S. releases.

Next Week’s Theme

Unlike the last few weeks we have a cornucopia of new information and also a symbolic focal point. With Congressional representatives still in their home districts, and the President pushing for tax reform, we have a natural preamble to Labor Day. Expect a week where everyone will be wondering:

What can be done to create more jobs with better pay?

Friday morning’s data will be the climax. And then…. most will take off for a long weekend.

The questions around employment have many important dimensions. It is fertile ground for debate and interpretation. The policy choices rest upon core values, one’s estimation of the current economy, and the analysis of each change. I have tried to lay out some key issues and viewpoints, but it is certainly not a comprehensive list.

-

The economy is in reasonable shape. Job growth is enough to absorb new entrants.

- The high voluntary quit rate reflects economic strength.

- Increased job openings signal a tightening labor market.

-

The economy is weak, with plenty of employment slack.

- The low level of labor force participation shows that employment never really recovered from the Great Recession.

- Wage gains have been modest and slow.

- Productivity growth has lagged the normal rate during an expansion.

-

Fed tightening pace rests upon the tightness of labor markets.

- Employment changes can signal incipient inflation.

- Has the non-accelerating inflation rate of employment (NAIRU) changed?

-

Is the minimum wage too low?

- Raising the minimum wage is the most direct way to help low-income workers.

- Raising the minimum wage may help some workers, but will reduce employment.

-

Improved employment gains rest on policy changes.

- Cutting taxes, especially on business, will stimulate investment and growth.

- Reducing immigration will open more jobs for the existing work force.

- Spending on new infrastructure projects will create more jobs.

- The employment picture is much weaker than thought because of unreliable government data and media distortions.

As usual, I’ll have more in my Final Thought, emphasizing my own conclusions.

Quant Corner

We follow some regular featured sources and the best other quant news from the week.

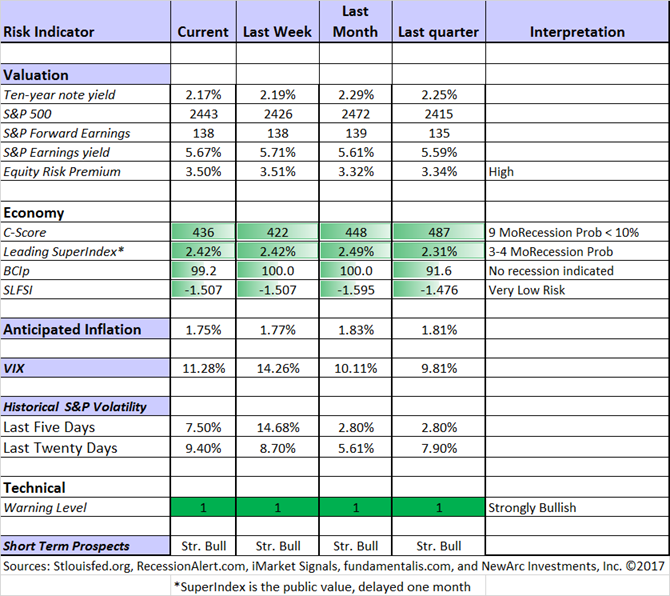

Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update.

The Indicator Snapshot

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score.

RecessionAlert: Strong quantitative indicators for both economic and market analysis.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

Doug Short: Regular updating of an array of indicators. Great charts and analysis.

Georg Vrba: Business cycle indicator and market timing tools. It is a good time to show the chart with the business cycle indicator.

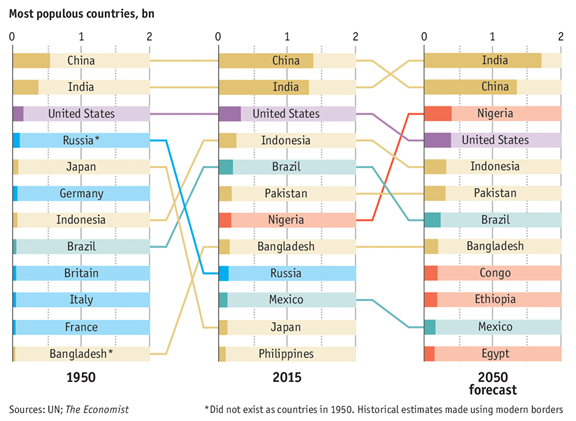

The Visual Capitalist has a great comparison of population dynamics for China and India. The dramatic effect of the “one child” policy is well worth noting and tracking. I cannot do justice to the animation of this comparison, so you need to check it out. I can show the projected dynamics over the next thirty years. Can you guess the three most populous countries in 2050?

Insight for Traders

We have not quit our discussion of trading ideas. The weekly Stock Exchange column is bigger and better than ever. We combine links to trading articles, topical themes, and ideas from our trading models. This week’s post covered stops and other methods for disciplined entry and exit. Blue Harbinger has taken the lead role on this post, using information from me and from the models. He is doing a great job.

Insight for Investors

Investors should have a long-term horizon. They can often exploit trading volatility!

Best of the Week

If I had to pick a single most important source for investors to read this week it would be Chuck Carnevale’s comprehensive analysis of how to analyze a stock like Nvidia (NVDA). Chuck takes you through the process of analyzing fundamentals, considering the company’s products, past versus future growth, and simulating alternative future cases. In addition to the article, there is a great video explanation. Even if you are not especially interested in NVDA, some time spent with this post and video is like a great class in stock analysis. Here is a key part of his thinking, the role of forward earnings estimates:

To my way of thinking, the only logical reason I would ever want to own any stock (business) is because I believe that the company is a profitable enterprise. Furthermore, this is not just about growth in the past, or growth in the present, but most importantly, growth in the future. After all, and as I previously stated, future profits will be the source of any long-term return expectations I might have. Moreover, the growth of those profits will be a primary contributor to the total annualized return I can expect the investment to produce on my behalf.

Therefore, I believe as investors, we cannot escape the obligation to forecast future earnings and/or cash flows because our results depend on it. Furthermore, we should not guess, nor should we simply play hunches. Instead, we must attempt to calculate reasonable probabilities based on all the information that we can assemble. Then we should apply analytical methods based upon our earnings and/or cash flow driven rationale that provide us reasons to believe that the relationships producing earnings and/or cash flow growth will persist in the future. In other words, we must strive to forecast future earnings and/or cash flow as accurately as we possibly can. On the other hand, we should simultaneously realize that perfection is not to be expected.

As an aside, there are many who criticize or even claim that we should eschew utilizing forward earnings and/or cash flow forecasts when trying to determine fair value, or even when trying to decide what stock to own. I find these positions rather bizarre. I cannot think of any logical reason why anyone would invest in a business unless they had a reasonable expectation of that business’s ability to generate future growth.

Stock Ideas

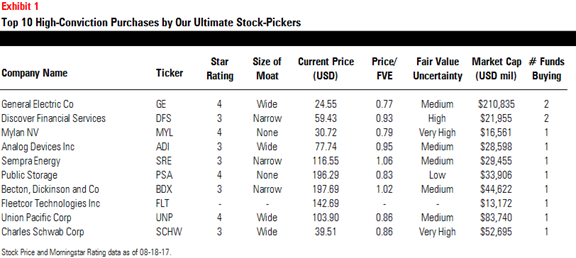

Morningstar’s list of the top high conviction picks from their “ultimate stock pickers.” Check out the full post for the methodology and analysis.

Barron’s sees 16% upside in PayPal (PYPL). Key drivers are the many new partners – twenty in the last eighteen months – and product innovation. Their peer-to-peer payment platform, Venmo, is popular with millennials. It can be used either to buy merchandise or to transfer money.

Brian Gilmartin provides counterpoint to some bearish predictions about Amazon (AMZN). Unlike most, he shares data so that you can do your own checking.

Eddy Elfenbein provides regular market commentary and close analysis of his “buy list,” which you can own via his innovative and inexpensive ETF (CWS). When one of his stocks has a dip, he helps you to decide whether to buy more (Smucker? SJM). You cannot find a more honest and transparent process. Best of all, the choices regularly beat the market.

Time for gold? For those seeking a “haven” Merrill Lynch has some buy-rated gold stocks. (Lee Jackson).

Dividends and Yield

David Fish identifies some dividend streaks that are in danger.

Simply Safe Dividends likes Air Products and Chemicals (APD), a dividend aristocrat.

Personal Finance

Seeking Alpha Senior Editor Gil Weinreich has an interesting topic every day. His own commentary adds insight and ties together key current articles. My favorite this week was Retire Your Debt Before You Retire. He does a fine, well-sourced analysis of issues, including excessive reliance on Social Security, increasing health care costs, and modest retirement assets. As he typically does, Gil raises a point that is interesting both for individual investors and for financial advisors. I read his work every day.

Abnormal Returns has a different topic each day. I read them all, but individual investors might find the Wednesday focus most relevant. This week I especially appreciated the pointer to Bloomberg for how far $1 million will take you in retirement, with state-by-state advice.

Strategy

Ben Carlson takes up the question of when to sell your investments. It is a great list of considerations, quite close to what we do. He begins by dismissing the slogans and then gets to some key considerations:

What kind of investor are you?

What’s your time horizon?

Why did you buy in the first place?

The wonderful and terrifying thing about investing is that you have two opportunities to be right and two opportunities to be wrong on every trade or investment — when you buy and when you sell.

An intelligent investor spends some time up front before the buy occurs to consider when or why they would sell a holding. If you don’t have some pre-established rules, guidelines or systems in place to understand what your sell trigger will be you’re just guessing.

Read the full post to see the very helpful advice.

Watch out for….

… a bond surge? Brian Gilmartin analyzes TLT and notes the implied risk for stocks.

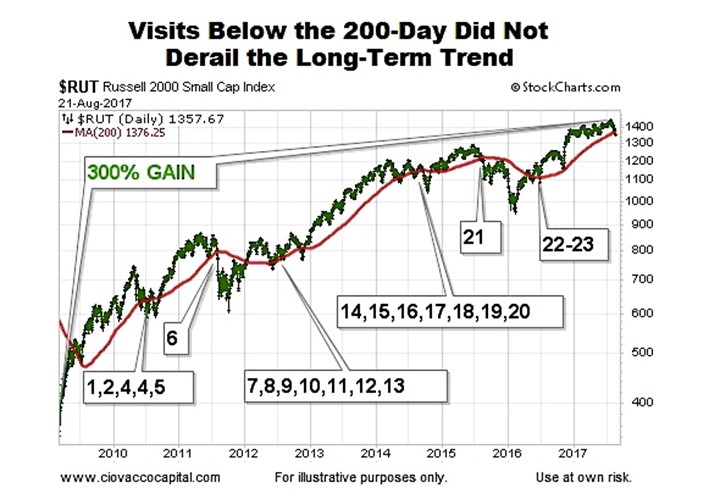

Noise. The two key articles are difficult to lay out here, so I urge you to read them in full. One comes up with the typical laundry list of “worries.”Chris Ciovacco provides the refutation. This stuff happens almost every day with a costly effect on the individual investor. The relative weakness in small stocks, or transports or whatever is seen as a dangerous divergence. If small stocks lead, the market is “frothy.” Here is one example from the posts:

Final Thoughts

Employment is the most important economic indicator — not because we have the best data, but because it hits so close to home. A job is part of one’s identity, sense of self-worth, and satisfaction with life. Concern about employment can be a constant stress, clearly affecting your spending and future plans.

Most people do not understand the overall magnitude of job losses. Since the monthly focus is on net job changes, we often ignore the underlying gross amounts. Nearly 30 million jobs are lost during a year. Even though more are created, the stress is under-estiamted. If you expand the effect to friends and family, the impact is even clearer.

So, what about the key questions? As usual in my “opinion” section, I will be frank about what I have personally concluded, but cannot cite all of the evidence. Most of this draws upon my past posts.

- The economy is still running below trend, but there is almost no recession risk. State and local employment remains low. Some fiscal stimulus would be helpful

- Tax changes can be part of an improved economic package. The problem is to create something sufficiently broad. Lower rates and fewer deductions helps to encourage marginal activity. It is nearly impossible to provide corporate assistance without addressing individual taxes. The pass through for partnerships solidly links the two, at least for small businesses.

- There is a political consensus for some changes, like the repatriation of funds. Unless this is tied to other policies, it probably will not help much.

- Solutions like a minimum wage increase are obvious to many—someone who works full time should earn more than the poverty level. That is the value proposition. The economic proposition recognizes the marginal cost of each employee. The minimum wage should be higher, but the exact level and pace of increase is a tough question. If we want a social safety net for low-income workers, there are other methods.

- The Fed is correct to watch the tightness of the labor market. I hope they do it well.

- I am very worried about the government data question. The idea of falsified data is completely wrong. There is a current idea about slashing the budget for key agencies. It is one thing to choose not to use experts in current decisions. It is another to cripple analysis for future generations.

[Some readers might enjoy my recent short paper, Getting Back in the Market. This has more specific suggestions about attractive stock sectors and good tactics. The Top Twelve Investor Pitfalls will help with your plan.Understanding Risk might also be of interest. All are free at your request from info at newarc dot com].

What worries me…

- Misleading signals from ETF trading. People infer too much from small market moves and the attendant media coverage. It is mostly a game – and one which benefits the astute individual investor. I explained the dynamic here.

- The debt ceiling game of chicken. Congressional leaders have confidence. Administration officials emphasize the importance of a “clean bill.” The President seems willing to use this as a bargaining chip. The Democrats are not saying much. I expect a solution, probably starting with an extension, but the participants are making it scary – just as in 2011.

…and what doesn’t

- The Fed. That includes both rate increases at a reasonable pace and the planned balance sheet reduction. This week I updated my theoretical analysis of the balance sheet with a strong example. If you missed it, please take a look.

- A near-term or seasonal market “correction”. Yes, it might happen, especially if investors are frightened. Worry is unprofitable because any seasonal effects are less important than the positive fundamentals. Most importantly, no one has a good record of accurately predicting corrections.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits