Weighing the Week Ahead: Is a Market-Friendly Policy Agenda in Peril?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsOnce again, the expected quiet summer week was instead filled with action. With analysts of all stripes analyzing every aspect of the changes in the Trump Administration, the financial punditry will do the same. Ignoring the politics and personalities, we are still left with a question that is important to investors:

Is a Market-Friendly Policy Agenda Now in Peril?

Last Week Recap

My notion that last week would be all about Korea and a possible correction was only half right. The Charlottesville events, the aftermath, and the President’s reactions took center stage. The turmoil once again offered a reason to sell. Once again this occurred despite a good week for economic data.

The Story in One Chart

I always start my personal review of the week by looking at this great chart from Doug Short via Jill Mislinski.

Doug has a special knack for pulling together all the relevant information. His charts save more than a thousand words! Read the entire post for several more charts providing long-term perspective, including the size and frequency of drawdowns.

The Silver Bullet

As I indicated recently I am moving the Silver Bullet award to a standalone feature, rather than an item in WTWA. I hope that readers and past winners, listed here, will help me in giving special recognition to those who help to keep data honest. As always, nominations are welcome!

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

The economic news last week was generally positive.

The Good

- North Korea backed off from a threatened missile launch toward Guam. There were some signs that diplomacy might prevail over military escalation.

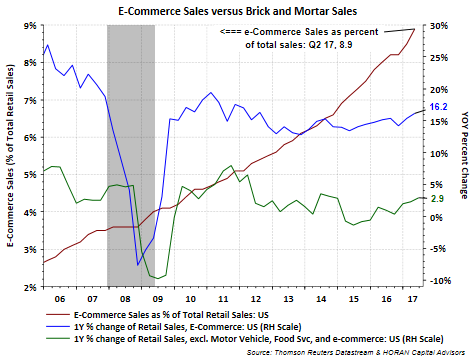

- Retail sales increased 0.5%, handily beating expectations of 0.3%. New Deal Democrat notes both the strength and upward revisions to prior numbers. Steven Hansen (GEI) confirms the interpretation with his year-over-year, rolling average approach. E-commerce sales continued to lead, growing 16.2% year-over-year. Horan Capital Advisors has more detail, including this chart.

- LA port traffic is the busiest ever. (Calculated Risk).

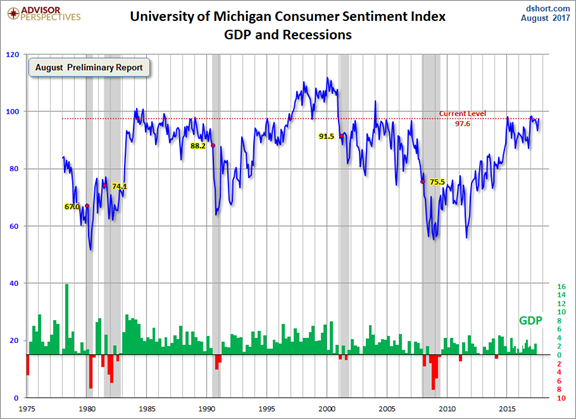

- Michigan sentiment jumped to 97.6. Doug Short’s great chart shows how this compares with past highs and with GDP.

- NAHB housing market index moved much higher (68 v last month’s 64) and handily beat expectations of 65.

- Leading indicators, jobless claims and industrial production matched the positive expectations.

The Bad

-

Rail traffic remains in contraction when analyzed without coal and grain. Steven Hansen (GEI).

-

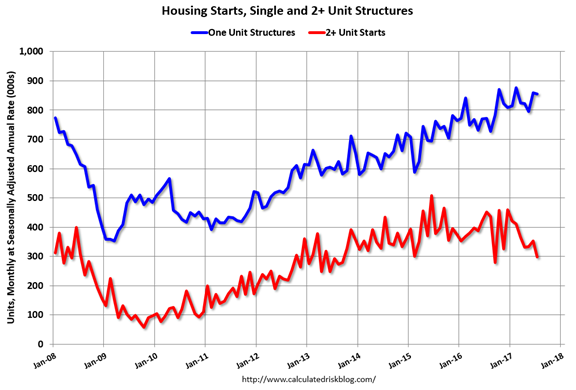

Building permits and housing starts both declined and missed expectations. Calculated Risk notes that multi-family is volatile, mostly moving sideways, but down 35% year-over-year. Single-family starts are up 10.9% year-over-year.

The Ugly

The cholera outbreak in Yemen has now spread to 500,000 people in the last four months. Stat provides perspective and describes the struggle to fight this disease. 30,000 health care workers have not been paid in more than a year.

Noteworthy

Better Congressional procedures would encourage more efficient attention to legislation. The Bipartisan Policy Center does a six-month review of the 115th Congress. Questions like number of days worked, use of committees, and delays are part of this analysis.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

The Calendar

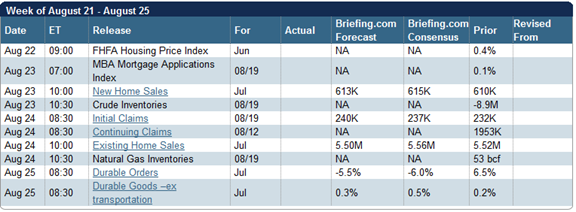

It is a modest economic calendar, with continuing summer vacations for many. Will there finally be a quiet week? I am especially interested in New Home Sales.

The Kansas City Fed’s annual Jackson Hole Economic Policy Symposium begins on Friday. Chair Yellen is the headline speaker, with the topic of “financial stability.” ECB President Mario Draghi will attend, but is not scheduled to speak.

Briefing.com has a good U.S. economic calendar for the week (and many other good features which I monitor each day). Here are the main U.S. releases.

Next Week’s Theme

Once again, the idea of a slow summer week, with Presidential and Congressional vacations, was completely wrong! The Charlottesville story is vitally important, but not so much for financial markets. The Administration’s controversial handling of the issue pushed it front and center. We can expect a focus on a specific threat:

Will the Trump team turmoil threaten the legislative agenda?

Last week’s decline proved to be a dip. Will this week be the same? Opinions differ sharply.

I forced myself to listen to pundit speculation, just so I could summarize the wild range. Please remember that our interest is not about the political and personal ramifications of events. My concern here is what this means for financial markets and our investments. Here is the speculation:

-

The Trump Administration has been crippled, preventing any progress on his important agenda.

-

The loss of key advisors will leave the Administration without needed expertise. (This was often cited as the proximate cause of mid-week market weakness).

-

The Bannon departure improved the chances for cooperation with Congress. (This was cited as the cause of Friday’s short-lived rebound. It was even cheered on the NYSE floor by the largely Republican traders).

-

The Bannon departure would weaken the Administration because he would now attack from outside. He could also pressure members of Congress who could face primary challenges from the right.

-

And finally, anyone who has been calling for a correction will inform you that “the time is now.” The claim is that a correction-ready market simply needs an excuse.

Last week I cited some sound, dependable sources about Korea – material worth reading. This week you will be bombarded with viewpoints whether you want to be or not. Play golf. Go fishing. See a ball game. Spend time with your family. Most of the commentary serves a specific political or market viewpoint.

As usual, I’ll have more in my Final Thought, emphasizing the key issues we should be watching.

Quant Corner

We follow some regular featured sources and the best other quant news from the week.

Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update.

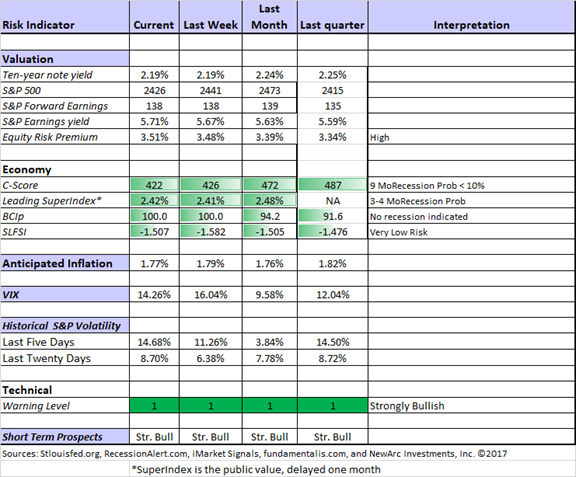

The Indicator Snapshot

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score.

RecessionAlert: Strong quantitative indicators for both economic and market analysis.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

Doug Short: Regular updating of an array of indicators. Great charts and analysis.

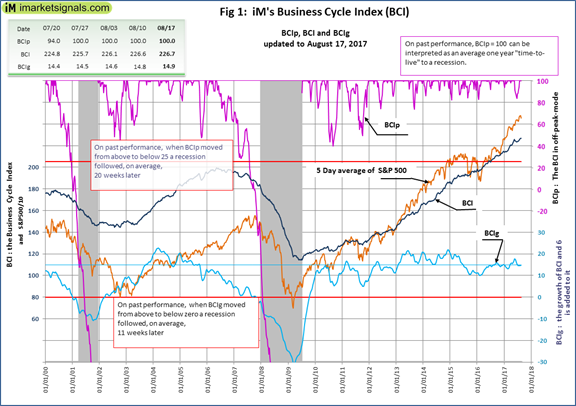

Georg Vrba: Business cycle indicator and market timing tools. It is a good time to show the chart with the business cycle indicator.

James Picerno’s business cycle work also has a positive, data-driven conclusion.

The US economy continued to exhibit a moderate growth bias through July. Although the monetary backdrop still presents a mild headwind, the majority of key indicators published to date suggest that recession risk remains low.

Near-term projections of the macro trend also point to a low probability that the economy will suffer a dramatic deterioration. The eight-year-old US expansion, in short, still looks resilient at the moment.

Insight for Traders

We have not quit our discussion of trading ideas. The weekly Stock Exchange column is bigger and better than ever. We combine links to trading articles, topical themes, and ideas from our trading models. This week’s post, Is the Bull Market Slowing?, showed how traders are coping. Blue Harbinger has taken the lead role on this post, using information from me and from the models. He is doing a great job.

Insight for Investors

Investors should have a long-term horizon. They can often exploit trading volatility!

Best of the Week

If I had to pick a single most important source for investors to read this week it would be the clear and calming words of the Fear and Greed Trader. He writes as follows:

With the major indices at or near all-time highs, low volatility, and everyone clamoring for a correction, the discussion has been ramped up about bubbles, stock market tops, etc. We’ve heard quite a bit of chatter about the bull market’s end being near. It’s too old and tired, its time has come. These calls have come and gone as the bull market has aged over the years.

The rhetoric gets ramped up the higher stock prices go by those that perceive something has to give, be it sooner or later. The perceived bubble has to burst. Therefore, the incessant “There is a stock market crash coming soon” comments portray a perception that is dealing with imagination and speculation rather than facts.

His work, as usual, has plenty of sound data, charts, and good sources. Like me, he is willing to change viewpoints with the evidence, but not when the economy is solid (Atlanta GDP now at 3.8%) and recession chances small.

As I note in today’s Final Thought, it is difficult to reach the right conclusion if you start with a misperception of the facts!

Stock Ideas

Chuck Carnevale has a fascinating post on Warren Buffett’s decision to sell General Electric (GE) and buy Synchrony Financial (SYF). Chuck has done prior research on GE under the tenure of the two most-recent CEO’s. He provides some insight into why a value investor might well prefer the spinoff financial company.

John Rhodes reaches a similar conclusion, shifting some assets to Synchrony from American Express (AXP). Besides its status as the largest private-label card, he cites some of their business relationships.

Steve Castellano likes Dollar General (DG), which he sees as competing successfully against Wal-Mart (WMT).

Peter F. Way uses his market maker hedging approach to compare CVS and Walgreens. While both have reasonable levels of safety, his method highlights some retail choices that investors might prefer.

Dividends and Yield

David Fish highlights seven champions expected to boost dividends before the end of October. His post describes the amazing record of these companies and adds some valuation analysis.

Mark Hines likes Omega Health Care (OHI), making it his “idea of the month.”

Personal Finance

Seeking Alpha Senior Editor Gil Weinreich has an interesting topic every day. His own commentary adds insight and ties together key current articles. My favorite this week was Success Through Booms, Crashes, Inflation And Recession. (Close runner-up is about not botching your retirement!) As is customary in this daily column there is something good for advisors as well as individual investors. He also recommended Cullen Roche’s excellent explanation of current household debt data. This has a lot of information that most neglect along with some excellent charts.

Strategy and Outlook

Ben Carlson has seven strategies for investing at market tops, although that is not what he is predicting. This inspired me to generalize my own thoughts on rebalancing portfolios as conditions change.

Eddy Elfenbein notes the increase in volatility while emphasizing the quiet background – his usual calm and wise advice.

Horan Capital Advisors explains why the economy still has upside via an increase in labor force participation.

Ralph Vince remains bullish.

Watch out for….

…Your bond fund? Morningstar warns that it might be riskier than it looks. The analysis describes risk changes, using the Sharpe ratio, in recent years versus data starting in 2002. Very interesting.

Final Thoughts

Where you end up depends a lot on where you start.

If you think that the post-election rally is all about Trump, you see the market as imperiled by changes in his team. If you see stocks as dependent upon the Administration’s ability to steer a specific agenda through Congress, you watch each twist and turn with bated breath.

If, like me, you had the following view:

- Expecting a post-election rally whomever won, just because uncertainty would be removed. (It is what I said at the time).

- Analyzing the Trump agenda in terms of the potential for compromise. This has also been consistent and accurate.

3. Evaluating the market on important factors that have been correct since the move from Dow 10K to Dow 20K.

- Valuation compared to alternatives – positive

- Valuation compared to inflation – positive

- Risk of recession – extremely low

- Financial stress – extremely low

- Market skepticism – extremely high

- Viewing some issues (debt ceiling change) as a threat and others (tax reform) as significant upside. The balances are positive.

With that background, the pending questions and conclusions gain some clarity.

The punditry on Friday was comical. CNBC ran multiple charts explaining each 50-basis point move in the market with some “breaking news.” The market was soft. Bannon was going to be fired, so markets rallied. Bannon might go on the attack against Trump. Markets declined.

Those trading on a time frame of a few minutes had to react to such action, but for the average investor it is complete nonsense. What should you be watching?

Most important is any sign of bipartisan compromise. This is the key indicator of the prospects for a market-friendly agenda.

Another possibility is a reduced possibility of a trade war. (Bannon was one of the most vigorous on trade issues). A tax cut might even be made retroactive (The Hill).

[Some readers might enjoy my recent short paper, Getting Back in the Market. This has more specific suggestions about attractive stock sectors and good tactics. The Top Twelve Investor Pitfalls will help with your plan. Understanding Risk might also be of interest. All are free at your request from info at newarc dot com].

What worries me…

- Perceptions about the upcoming debt limit issue. No signs of progress so far, and it will be hitting the headlines.

- Similarly, perceptions about leadership. If enough people conclude that there is a problem, there will be a problem.

…and what doesn’t

- The Fed. That includes both rate increases at a reasonable pace and the planned balance sheet reduction. Expect these worries to be heating up this week, before the annual Jackson Hole conclave.

- Recession worries. Nothing peps up a dull story like a headline which includes “Next Recession is Looming.”

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits