The early optimism that President Trump would be able to reinvigorate domestic economic growth has faded as Congress struggled to pass health care legislation and confusion exists around Trump’s political agenda. There is a growing divergence between the fundamentals supporting the domestic economy and company valuations in the domestic equity market. We believe that in the absence of meaningful tax reform and financial regulatory reform, the economy will likely slow dramatically.

Yet, the bond market and the domestic stock market are telling investors two different things. As equity prices climb higher, the market has focused on a mixed bag of earnings growth and has ignored most negative news. At the same time, bond yields remain low and we do not see much of a breakout higher as the Fed signals further tightening in monetary policy. It appears that stock prices are discounting economic prosperity while bond prices are discounting a slowing economy.

It is truly puzzling to us that the geo-political events including the increased tensions with North Korea, China, Russia and the Middle East combined with the uncertainty around Great Britain leaving the European Union are not impacting market volatility or appear to be discounted in equity prices. As a clearing house for the price of risk, markets can be either efficient or inefficient in that pricing function.

Given the divergence between stock and bond valuations coupled with the coordinated simulative monetary policies of the global central banks, we are uncomfortable with the sustainability of the current elevated equity valuations.

As we review our portfolio structure and the investment opportunities in the market, we are struck by another observation. From a more macro perspective, we are living through tectonic shifts in corporate America that will impact revenue models in specific companies and sectors for decades to come. This is making the investment analysis and investment decision more difficult because the uncertainty around the sustainability of a company’s business model. For those who can remember, think about how quickly typewriters became obsolete in our offices and home.

Today, one of the most obvious examples of this paradigm shift is the increased use of on-line shopping which is impacting the profitability of brick-and-mortar stores. The traditional retail sector is going through a harsh decline in foot traffic and sales as more and more consumers shop on-line. In a similar vein, electric cars are a growing part of the domestic auto market, and consumers have embraced electric and hybrid autos as a cost-effective alternative to traditional carbon burning engines. Changes in how media content is delivered to the home is also going through massive changes today. The traditional cable provider is being challenged by “skinny bundles” through services like Apple TV and Sling. In addition, subscription services from companies like Netflix and Amazon Prime are now providing original content which historically was provided by the networks. The increased popularity of Airbnb is having an impact on the hotel industry. And, the growing popularity of Uber and Lyft are having a negative impact on the traditional car rental business like Hertz and Avis. Many of these established companies are now challenged to adapt to the changing competitive landscape. As investors, we have to recognize these shifts and understand how management is adapting to the changes in the marketplace. Where management has been slow to adapt, shareholders have suffered.

The Economy

If we simply focus on the fundamentals that are driving the domestic economy, we believe that the economy is experiencing slow and steady growth of around 2.6%. We are eight years into a domestic economic expansion, one of the longest since World War II. Yet, in spite of dramatic monetary stimulus following the Financial Crisis in 2008 and the recent declining unemployment, we are not experiencing a significant acceleration in domestic growth as might be expected. The consumer sector is healthy; however, we believe that growing signs of weakness in auto sales, the growing overhang of auto and student loan debt, and a sharp decline in bank lending signal the risks to the economy are to the downside.

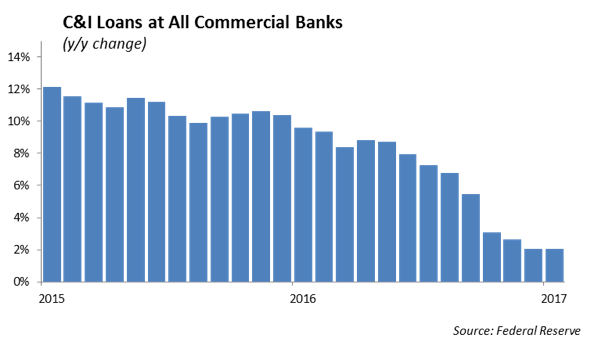

Private credit expansion is the lifeblood of the economy and bank loans are the largest form of credit. Growth in consumer and industrial loans, which have grown steadily at 8% since 2015, experienced a sharp decline in November of last year and are now growing at a mere 2.1%. This tells us that small business sector is still having trouble accessing credit through banks. Growth in credit card, auto loans and real estate has also declined over the same period. The difficulty that small business have obtaining loans remains a significant impediment to economic growth.

The U.S. banking system is well capitalized; however, the banks’ willingness to extend credit to small and medium size businesses remains limited. Slow loan growth is at the heart of slow economic growth and is hampered by regulatory issues. Historically, the small business sector is the biggest source of job growth in our economy. There is a growing chorus around reducing the regulatory burden for banks which grew under the Dodd-Frank Act, however, it remains to be seen what exactly that will look like.

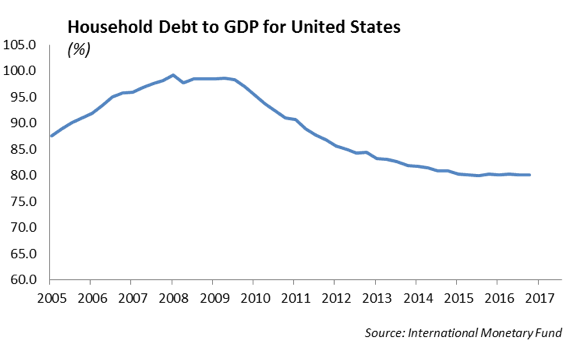

Consumer’s balance sheets are generally in good shape. Household debt levels, which peaked at nearly 100% of Gross Domestic Product in 2008, have declined to 80%. However, with the increase in auto leases as opposed to outright purchases, we believe that this debt measure underestimates the true amount of credit in the system. We see evidence of this with consumer credit as a share of disposable income which recently hit a record high of 26.6%, even with credit card debt and mortgage debt levels declining over the past ten years. Within the consumer sector, we are concerned with the recent increase in credit-card and sub-prime auto loan delinquency rates.

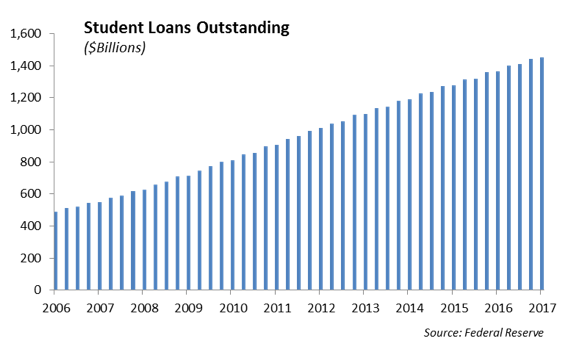

Student loan debt continues to grow and is now over $1.41 trillion outstanding. The rising trend in college tuition appears to be slowing but the use of student loan debt to fund college expenses continues to be problematic for several reasons. First, the level of debt is not calibrated and students can end up with $100,000 of debt and an entry level job which doesn’t pay enough to service the debt. Second, most of these loans are co-signed by parents, many of whom end up supporting the debt service, which impacts consumption. In addition, while there are government programs that will help to reduce the amount of student loan debt, it cannot be restructured through a bankruptcy and ultimately stays with the student throughout their life until it is retired. This acts as an anchor for consumption for a growing part of the population and is a cancer within the economy.

We are seeing early signs of wage growth which bodes well for the household sector and consumption. While overall consumer credit shows a healthier picture since the financial crisis, if and when economic growth slows, we expect to see problems surface in consumer credit which will impact consumption.

Global manufacturing has been stable with domestic industrial production in the U.S. rising steadily over the past six months. This is due, in a large part, to an increase in oil and gas production following the collapse in oil prices in early 2016. Manufacturing has been the consistent bright spot in the domestic economic recovery and has added over 580,000 jobs in the second quarter of this year.

Monetary Policy

We expect the Federal Reserve will continue its move toward tightening monetary policy during the second half of the year; however, progress may be slower than the Fed is leading us to believe. The key drivers for their decision are the pace of inflation and employment. Both are showing improvement which gives us encouragement that the Fed will begin to extract its invisible hand from the market this year.

The Federal Reserve has inched the Fed Funds rate up 0.25% again so that it is now resting at a range of 1.0% to 1.25%. The Fed has successfully pushed short term interest rates higher following several years of a 0.0% Fed Funds rate. With the unemployment rate at 16 year low, the rate of domestic inflation appears to be decelerating and falling below the 2% target. We continue to see evidence of declining price pressures in commodity prices, oil prices, growing auto inventories, and sagging retail sales.

However, we are starting to see increased pressure on wages on both the low end and the high end of the wage spectrum. Unemployment has moved down to 4.3% from 4.9% earlier this year. The economy is producing roughly 194,000 jobs a month over the past quarter and employers are reporting difficulty filling jobs in both skilled and unskilled fields. Average hourly earnings have increased 2.5% over the past year and we expect that to continue to increase in the second half of this year. As unemployed and discouraged workers find jobs, the slack in the labor market continues to decline. This combination of low unemployment and reduced slack in the labor market should help to improve productivity and, in turn, put upward pressure on inflation and interest rates.

The Federal Reserve has signaled that it is getting closer to the time where it will begin to reduce the size of its bond portfolio. As part of its monetary policy tool kit following the Financial Crisis, the Fed purchased over $4.5 trillion in bonds in the open market. This had the effect of lowering interest rates along the yield curve which, in turn, allowed businesses that could access the public bond markets to lower their borrowing costs. This proved to be a powerful tool to lubricate the gears of the economy through the corporate sector. It was also market manipulation on a huge scale and we are card carrying free-market capitalists. Until we see evidence of a sustained increase in the rate of inflation, we believe the Fed will be slow to unwind its bond portfolio. The Fed has indicated it may begin to shrink its bond holdings as early as September, however we expect a slower more cautious approach toward unwinding its balance sheet.

Whenever there is excessive monetary stimulus, there are “bubbles” that appear in the capital markets and economy. In 2007 for example, we saw a bubble in sub-prime and residential mortgages. The question we are asking is: “where is there a bubble?” While we do not expect to see proof of the bubble until it pops, we believe there are legitimate concerns of excesses in domestic equity prices and commercial real estate. We are seeing the use of margin and other collateral lending in individual stock accounts has increased. Goldman Sachs announced a new partnership with Fidelity last month to provide loans secured by their investment accounts to Americans who want to borrow up to $25 million. Bank lending has been reasonable in commercial real estate, but we are stunned at how low cap rates have fallen in some regions of the country. At the same time, there is a glut of retail space as grocery store chains consolidate and shopping mall vacancies increase.

Why the Price of Oil Matters

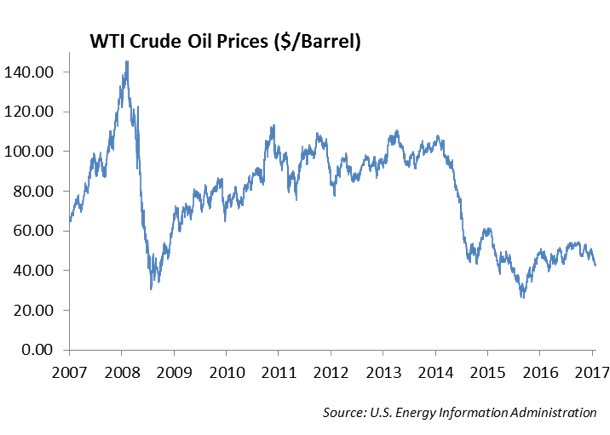

The energy sector is a significant component of the U.S. economy and is important for job creation and capital investment. During the quarter, the price of U.S. crude oil declined from a high near $51 to $46 per barrel at the end of June, a decline of nearly 20%. While OPEC announced production cuts last month totaling 1.8 million per day, not surprisingly, crude oil shipments from the United States are approaching 2 million barrels per day. The U.S. oil rig count rose to its highest level in two years. Operators have now put more than 100 rigs back to work from Oklahoma to North Dakota in the past quarter. If oil remains stable around $50 per barrel, we believe this will help to support domestic economic growth and maintain the fracking at current levels. However, volatility around the price of oil adds uncertainty to capital investment and will have a negative impact on growth. However, the risk is that the recent OPEC production cuts will not hold and that eventually there will be downward pressure on oil prices as OPEC production normalizes to pre-cut levels. The U.S., which now legally can export oil, has become the swing producer and is projected to have the infrastructure to ship close to 3 million barrels a day next year. Ironically, China will potentially be one of the largest purchasers of U.S. light crude oil.

Global Economic Growth Appears Stable

In spite of consistent revisions lower by the International Monetary Fund and World Bank over the past two years, global economic growth appears to be stable. The European economy appears to be experiencing growth; however, inflation in Europe is falling short of the 2% target set by the European Central Bank. European Central Bank President Mario Draghi has indicated that ECB monetary policy will stay the course with €60 billion per month in bond purchases through the end of 2017. However, we suspect that the ECB, like the Fed, would lean toward reducing bond purchases and allow markets to adjust to a more normalized conditions. Following the Financial Crisis, the European banks are better capitalized today. As a result, we expect that credit flows to emerging economies will increase which will help support economic growth.

Economic weakness persists in Brazil, much of Latin America and the Middle East. Stabilizing commodity prices following the plunge in 2014 have helped developing economies including China and Russia. China’s construction and mining sectors appear to be showing surging growth again as the country has put much of its financial turmoil behind it for now.

Investment Strategy

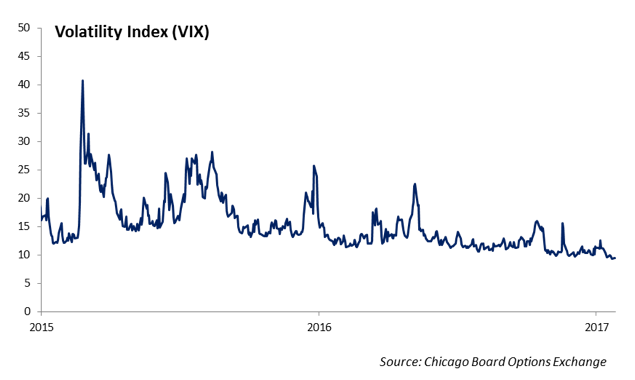

Volatility has declined to its lowest levels since 1960 and the expected returns on publicly traded stocks and bonds are compressed at low levels. The result for investors remains a conundrum. Since both volatility and correlation calculations are ex-post, the low volatility reflects the historic risk profile of the assets in a portfolio. In a diversified portfolio of publicly traded securities, equity risk will be an outsized proportion of the total risk. One of the major non-correlated asset classes to domestic equity is domestic fixed income. But, the expected horizon returns for fixed income over the next three to five years are in the 3 to 5% range. In a diversified portfolio, any allocation to fixed income will be challenging on an absolute return basis. However, on a total rate of return basis, fixed income is a necessity in a portfolio in order to reduce risk and improve relative performance.

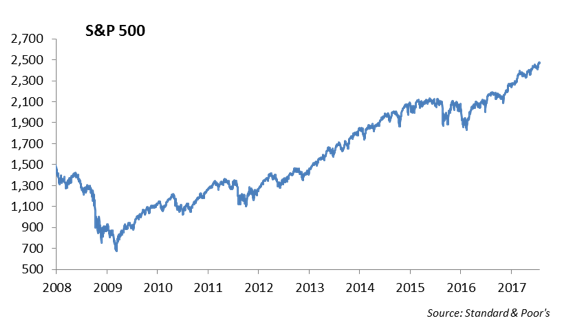

The equity market continues to pierce new record levels. However, the performance of the indices are being carried by the performance of a small number of stocks. As the Dow Jones Industrial Average reaches 22,000, the surge has been led by only a few stocks including Apple, Boeing and United Healthcare. Similarly, the surge in the S&P 500 past 2,400 has been led by the technology, financial, and healthcare stocks. Rising interest rates were a significant boon to bank earnings this past quarter lending increased in both consumer and commercial businesses and net interest margins increased. Whether its price to earnings, price to cash flow, or other valuation metrics, we remain concerned that domestic equity valuations are excessive at current prices. We do not see evidence that there is a broad market rally in stocks which raises concerns with the sustainability of valuations at current levels.

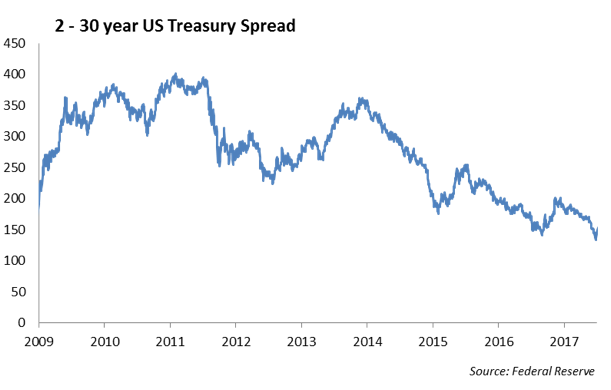

The yield curve is flattening as the spread between the two year US Treasury and the thirty year US Treasury narrows. At the beginning of 2015 the 2-30 year spread was close to 250 basis points. Today, that same spread is roughly 150 basis points. This makes investing in debt further out the yield curve more challenging as investors are less compensated for the risk of extending into longer maturities. We lean to the “old school” and believe that the flattening yield curve foreshadows an eventual slowing in economic growth.

Domestic investment grade credit spreads have tightened significantly over the past year driven by a surge in foreign buying particularly from Japan and Taiwan Insurance companies. Tight spreads and low volatility are helping to support positive returns form fixed income assets in the face of rising interest rates. The contraction in credit spreads was most pronounced in noninvestment grade credits which has pushed high yield valuations to extremely high levels. The margin of error for investors increases with tighter credit spreads. This is the time to move up in quality in credit since the cost is cheaper. We are reducing high yield exposure given the tighter spreads over the past quarter.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2017 Winthrop Capital Management

Read more commentaries by Winthrop Capital Management