The US Department of Labor (DOL) has cut financial advisors some slack in getting ready to comply with its new fiduciary rule. But defined contribution (DC) plan sponsors don’t have the same luxury.

That’s because plan sponsors have been subject to Employee Retirement Income Security Act (ERISA) fiduciary rules since 1974, whether they know it or not. And based on the results of our latest survey, many don’t know it.

According to ERISA, fiduciary duty requires DC plan sponsors to comply with a set of core standards of conduct. These include:

- Acting in the best interests of plan participants

- Paying only necessary and reasonable expenses for administering the plan

- Performing duties with the care, skill, prudence and diligence of a person knowledgeable in the field

- Minimizing large investment losses by offering a diverse investment menu

- Adhering to the terms of documents governing the plan

- Avoiding any self-dealing or conflicts of interest

KNOWLEDGE IS POWER (IGNORANCE ISN’T BLISS)

Those fiduciary requirements may seem daunting, especially when plan sponsors have wider responsibilities in their company—or if they’re “just part of” an investment committee or plan administrative committee.

But all plan sponsors are on the hook for core standards of conduct. So it’s always a good time for everyone connected with the operation of their company’s DC plan to review the who and what of fiduciary responsibilities. It may also make sense to do it now, because more outside advisors and consultants will soon become fiduciaries, too.

There’s another timely reason: our latest survey, Inside the Minds of Plan Sponsors, indicates that too many plan sponsors don’t realize their fiduciary status—and the legal obligation it puts on them.

We surveyed more than 1,000 plan sponsors, all of whom qualified as fiduciaries through initial screening questions. However, when respondents were asked directly if they were fiduciaries, nearly half (49%) said no. Only 44% were certain of their fiduciary status, and roughly 6% said they didn’t know or weren’t sure. No one should be guessing about this, given their fiduciary status and responsibilities to the plan, to participants and even to their own personal liability.

There’s another cause for concern: fiduciary awareness is declining. In 2011, 61% of our respondents knew they were fiduciaries. So a drop to only 44%—17 percentage points lower—calls for a deeper look at how to make plan sponsors more aware.

FOR FIDUCIARIES, THERE IS AN “I” IN “TEAM”

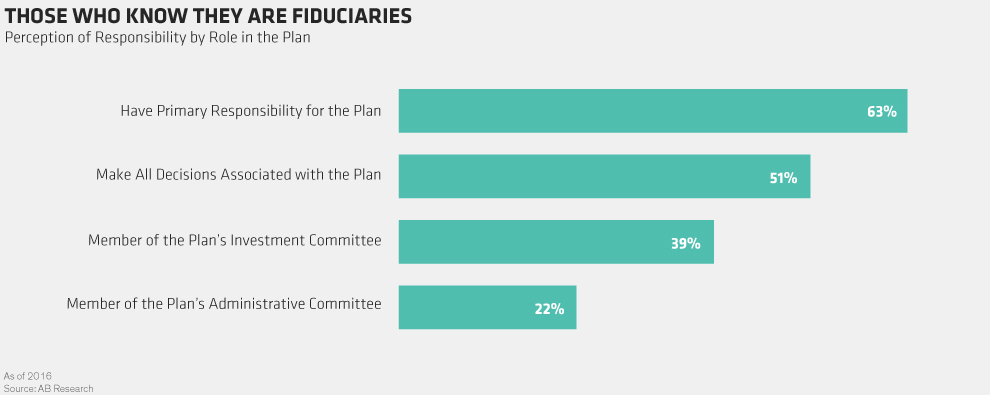

Roles likely explain part of the disconnect between plan sponsors and their fiduciary awareness. Broadly speaking, four categories of sponsors qualify as fiduciaries (Display):

1) Those with primary responsibility for the plan

2) Those who make all decisions associated with the plan

3) Members of a plan’s investment committee

4) Members of a plan’s administrative committee

A lot of awareness depends on “the buck stops here”: How close or far away does the individual sponsor feel from overall plan responsibility?

The first category of sponsors—those with primary responsibility for the plan—are most likely to know their fiduciary status (63%). Awareness drops significantly for the next category—those who make all plan decisions—although it’s still more than half (51%). The problematic statistics are for the two categories of plan sponsors who belong to a committee.

Committee members may think there’s safety in numbers, which may be why so few members of investment and administrative committees see themselves as fiduciaries. Less than four in 10 (39%) members of investment committees know they have fiduciary status, and even fewer administrative committee members recognize their legal responsibility as fiduciaries.

TIME FOR TRAINING…AND TRAINERS

Fiduciary training could help improve awareness, and the good news is that two-thirds of plans offer fiduciary training programs. Unfortunately, about half of the respondents who have access to a training program don’t think it’s comprehensive. And while 80% say their plans document the fiduciary process—a crucial step—more than half say the process could be improved.

Lack of resources and of internal expertise can be obstacles. While many larger plans have access to in-house resources, that’s less likely to be the case for plans with less than $50 million in assets––and could be too costly to staff full-time. For these smaller plans, working with a financial advisor or consultant can help boost fiduciary awareness.

Outside advisors can provide a variety of benefits, including an objective check on advice received from other service providers, fiduciary investment advice, and plan documentation and due diligence services. The good news is that two-thirds of smaller plans do use a financial advisor or consultant.

It’s possible that receiving these critical services from external resources may contribute to the sense that plan sponsors aren’t on the hook as fiduciaries. That would be unfortunate, because plan sponsors and the advisors working with them are co-fiduciaries. Both are liable for a breach of fiduciary duty by another fiduciary.

That’s all the more reason for plan sponsors to brush up on their fiduciary responsibilities. And it’s much more likely that smaller plans using advisors actually have improved fiduciary awareness among their sponsors. Our respondents who use financial advisors/consultants are twice as likely to feel that fiduciary responsibility reviews are important.

With today’s greater focus on fiduciary issues, a few timely actions can help plan sponsors raise their fiduciary awareness and lower their exposure to risk.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

© 2017 AllianceBernstein L.P.

© AllianceBernstein

Read more commentaries by AllianceBernstein