The S&P 500: Just Say No

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsPension Trustee Smith: I recommend to the committee that we liquidate our International equity assets and index our equity exposure to the S&P 500. US stocks have outperformed for the last 20 years, and I see no reason why that should not continue. Everyone knows that the US is the strongest economy and market in the world.

This is a somewhat fictionalized version of a comment or conversation that has gone on in many committee discussions over the last several years in one form or another. And why wouldn’t it? Being a US equity investor over the past several years has felt glorious. The S&P 500 has trounced the competition provided by other major developed and emerging equity markets. Over the last 7 years, the S&P is up 173% (15% annualized in nominal terms) versus MSCI EAFE (in USD terms), which is up 71% (8% annualized), and poor MSCI Emerging, which is up only 30% (4% annualized). Every dollar invested in the S&P has compounded into $2.72 versus MSCI EAFE’s $1.70 and MSCI Emerging’s $1.30. Diversification theoretically sounds good, but as Yogi Berra said, “In theory there is no difference between theory and practice, in practice there is.” Diversification in this particular instance seems good in theory but not so much in practice.

So, shouldn’t we agree with Trustee Smith and throw in the towel, index all of our equity exposure to the S&P 500, and call it a day? If our goal is compounding capital for the long term, which it is, we would not just say “No,” but something akin to “Hell no!”

Valuation of the S&P 500

The bedrock of everything we do is valuation, so let’s begin addressing Trustee Smith’s concerns with a look at the current valuation of the S&P 500. We will start our tour of valuation by examining our own framework. This in turn starts by understanding the drivers of return.

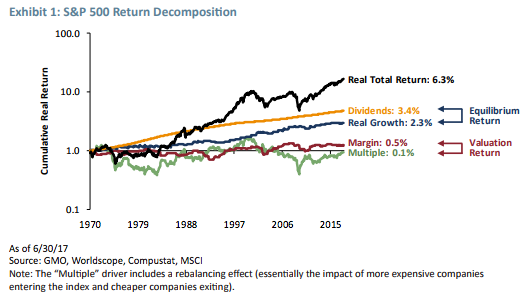

For any equity market, the return achieved can be broken down into four component parts. In the long term, the return is almost exclusively driven by dividends (growth and yield). Equity owners need to be compensated for providing capital to companies to help fund their long-term investments. That compensation comes from the cash flows the companies generate from their risky investments via earnings and dividends.

The two other ways to make money from owning an equity asset class are from multiple (P/E) or margin expansion (collectively we call these elements the valuation components). Together these four components make an identity – we can (ex post) always decompose returns into these factors. In Exhibit 1, we show a return decomposition for the S&P 500 since 1970 based on these four factors (earnings, dividends, margins, and P/Es). Margins and P/Es are basically flat over this very long time period. As we stated above, over the long term, the returns achieved have been delivered largely by dividends.

Using this same decomposition over the last seven years, we see quite a different story in Exhibit 2. Earnings and dividends have grown as one would expect, but P/E and margin expansion have significantly contributed to returns with multiple expansion actually providing the biggest boost of the four. This is typical of short-term periods, where the volatility of returns is dominated by shifts in the valuation components.

If earnings and dividends are remarkably stable (and they are), to believe that the S&P will continue delivering the wonderful returns we have experienced over the last seven years is to believe that P/Es and margins will continue to expand just as they have over the last seven years. The historical record for this assumption is quite thin, to put it kindly. It is remarkably easy to assume that the recent past should continue indefinitely but it is an extremely dangerous assumption when it comes to asset markets. Particularly expensive ones, as the S&P 500 appears to be.

GMO’s S&P 500 forecast

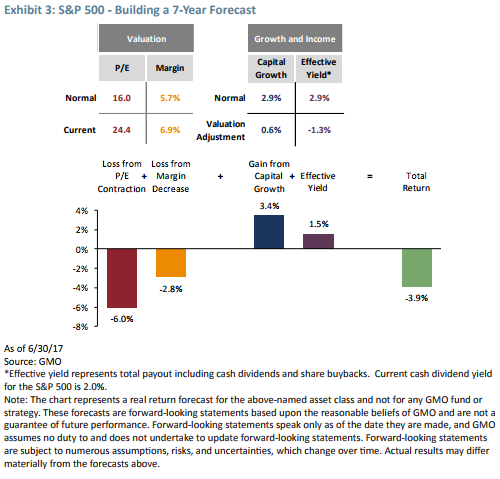

To go from the above accounting identity to a framework for forecasting returns requires some statement about the way the four elements will evolve over time. Our forecasts are similar in spirit to a cyclically-adjusted P/E1 but we try to account for the cyclicality of earnings a bit differently. We look at trailing P/Es and then make an adjustment to margins where we look at multiple proxies for returns on economic capital. We assume that whatever level P/Es and margins are trading at today, that at the end of seven years they will mean revert to equilibrium levels. This isn’t to say that in exactly seven years’ time we expect everything to be back to normal; rather, given how difficult it is to see seven years into the future, assuming a return to normal is a pretty good starting point. We then factor in earnings growth and income (dividends and buybacks) that we receive as equity owners.

Of course, there is some art and judgment associated with this model (unfortunately, social systems like markets are not beholden to such things as physical laws of nature). This framework is a great starting point for a conversation (at least it is if you find conversations about the likely returns to investments stimulating). If someone comes to you and says, “I think US equities will deliver 10% real per year from now on” you can ask them how. Does he think P/Es and margins will continue to expand? Does he have some rampantly bullish view on growth? Or perhaps an odd view on yield? Likewise, if you think our assumptions are daft, you can insert your own. We update this model every month and you can see the current dilemma in Exhibit 3.

This simple model does a very nice job of figuring out what we think the S&P 500 is worth and allows us to ask risk management questions around where the model could be wrong. From our perspective, one has to make some fairly heroic assumptions to believe that the S&P is even remotely close to fair value. Holding all else constant, an equilibrium P/E of 31 would make the S&P look fairly valued today. However, to believe that a “normal” market valuation is 28x earnings brings us back to the logic provided in the dot com bubble – Dow Jones 36,000 anyone? Similarly, we are just off the highs of the highest profit margins we have seen in the post WWII era. Equilibrium levels for profit margins would have to be almost doubled to make today’s elevated levels look fairly valued, again holding all else constant. As the old Maine expression goes, “You can’t get there from here.”

Other lenses

While we think our framework is pretty sound, we like to employ other lenses to see if they give similar signals. [Reader’s note: If you are in agreement that the S&P is expensive, this section is basically more confirmation bias so please feel free to skip to the next section where we begin to discuss the implications.] A simple perspective, which we believe to be useful, is a Shiller (or Graham and Dodd or Cyclically Adjusted) P/E. This represents a straightforward way of normalizing earnings from their current value to something that approximates trend by using a 10-year moving average of earnings.2 Exhibit 4 plots this series. As even a cursory glance at the chart reveals, this is the third most expensive market in history. The only times we have seen more expensive US equity markets were 1929 and 1999. Strangely enough, we do not hear many exhortations to buy US equities because it is just like 1929 or 1999.

Now this measure has its detractors – from those who worry about distorted earnings from 2008, to those who argue that shifts in payouts have invalidated the measure. However, none of these criticisms has yet swayed us. For instance, correcting for the shift in payouts does little to alter the conclusion reached above.

For those who worry about the inclusion of a bad year for earnings like 2008 in the decade average, another measure paints a very similar picture. We have called this measure the Hussman P/E, after John Hussman, its creator. It is spiritually very similar to the Shiller P/E, but rather than normalizing to the 10-year average earnings, it normalizes to peak earnings. This obviously gets rid of the bad year problem. As Exhibit 5 shows, using this methodology indicates that this isn’t the third most expensive US stock market in history: It is the second most expensive US stock market in history. Only the period of the TMT bubble surpasses the expensiveness of the current market.

Now, perhaps one could argue that we should forget all this top-down valuation nonsense and look at the situation through the lens of a stock picker. The first way we could think about this perspective is to look at the valuation of the average (median) firm. Exhibit 6 shows both the median price to sales ratio for stocks in the S&P 500 and the P/E 10 (Shiller) for the median stock in the S&P. The median price to sales data reveal something quite extraordinary – the average US stock has never been more expensive than it is currently, even at the height of the insanity that was the TMT bubble of the late 1990s. We have never seen such broad-based overvaluation of US equities. While not quite as extreme, the median P/E 10 also shows the median stock is about as expensive as it was prior to the TMT bubble and the Global Financial Crisis. Either way, these stock level measures show essentially the same conclusion as the overall top-down measures. We are facing an exceptionally expensive stock market.

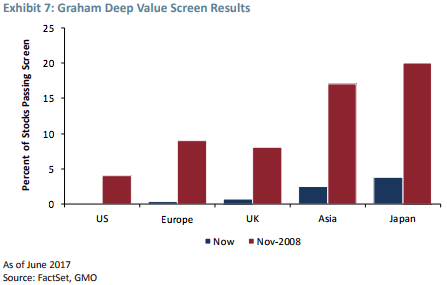

An alternative measure of the scale of the opportunity set is afforded by using a screen developed by Ben Graham.3 He suggested a deep value screen based on four criteria: 1) the stock’s earnings yield should be at least twice the AAA bond yield; 2) the stock’s dividend yield should be at least two-thirds of the AAA bond yield; 3) the issue should have total debt of less than two-thirds the tangible book value; and 4) the stock should have a Graham and Dodd P/E (price divided by 10-year earnings) of less than 16x.

Exhibit 7 shows the results of running this screen across a variety of markets at two points in time: late 2008 and today. In late 2008, the screen was finding lots of cheap stocks – 20% of Japan and the Asian markets were passing the screen; 10% of stocks in the UK and Europe were “deep value” cheap; and, even in the US, 5% of stocks were being thrown up as deep value (including the likes of Microsoft!). Now, fast forward to today. In Japan and Asia only around 5% of stocks are showing up as extremely cheap; in Europe and the UK the number drops to 1% to 2%; in the US not a single stock passes the screen. Not one single solitary stock can be called deep value.

As Graham noted, “True bargains have repeatedly become scarce in bull markets…Perhaps one could even have determined whether the market level was getting too high or too low by counting the number of issues selling below working capital value. When such opportunities have virtually disappeared, past experience indicates that investors should have taken themselves out of the stock market and plunged up to their necks in US Treasury bills.”

Not permabears – just valuation-driven

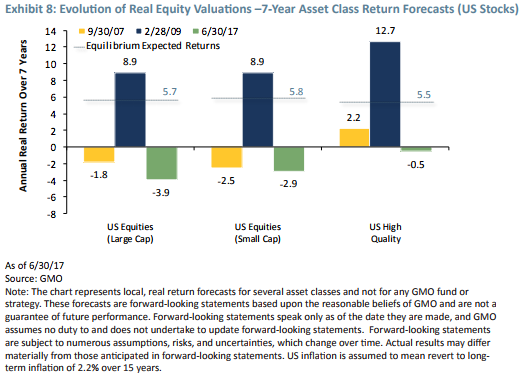

Please do not mistake us for members of that species known as permabears. We don’t always hate US equities as a matter of principle. We are just governed by the precepts of valuation. For instance, Exhibit 8 shows that in 2009 our valuation measures were saying that the US equity market was offering pretty attractive returns (other markets were even more attractive at that stage). So we aren’t a stopped clock, but we tend to follow Keynes’ apocryphal advice, “When the facts change, I change my mind. What do you do, sir?”

The S&P 500 has done even better than our bullish forecasts of 2009. And if we adhere strictly to our seven-year time horizon, our forecasts have fared much worse. Our forecast for the S&P in December of 2009 was a return of 1.3% real for the next seven years.4 As we observed in our opening, the S&P has done much, much better than that. The methodology that seems to have done a good job of anticipating the brutal bear market of 2008-09 and signaling great opportunities in February of 2009 appears to have run fallow or is broken (as is often the case in the middle of a cycle). So, what happened?

Our forecasts assume mean reversion of both P/Es and margins over a seven-year horizon, and clearly that has not been the case over the past seven years. P/Es have remained elevated and profit margins have risen, hit cyclical highs, and remained elevated. We have spent an enormous amount of time questioning our assumptions. While we can make arguments5 for a somewhat higher P/E than what we have seen historically or what we use currently in our forecasting methodology, we cannot get our heads around the sustainability of current levels for multiples. Likewise, we are currently doing research on the impact of increased industry concentration in the US (greater monopolistic tendencies within industries) and how this may affect the level and speed of the mean reversion of profit margins. Jeremy Grantham in the 1Q 2017 Quarterly Letter questioned the traditional assumptions of the mean reversion of profit margins and warned “it’s different this time” due to the effects of, among other things, increased industry concentration. We are doing additional empirical work to see how this may impact our forecasting assumptions. However, Jeremy most certainly is in agreement that the US market, even despite his quite rare “it’s different this time” admonition, is not cheap and much prefers international and emerging market stocks to the US (more on this topic later in this paper).

Going passive is an active decision

Human nature is to extrapolate the recent past. It is easy to see, given the strong performance of US equities in both absolute and relative terms, why many are suggesting they are the only asset you need to own. And the cheapest way of owning them is passively.

However, the decision to be passive is still an active decision – and we would suggest one with important risks that investors are not paying adequate attention to today. As more and more investors turn to passively-managed mandates, the opportunity set for active management increases.6 A decision to allocate to a passive S&P 500 index is to say that you are ignoring what we believe is the most important determinant of long-term returns: valuation. At this point, you are no longer entitled to refer to yourself as an investor. You may call yourself a speculator, but not an investor. Going passive eliminates the ability of an active investor to underweight the most egregiously overpriced securities in the index (we obviously prefer a valuation-based approach for stock selection as well). When faced with the third most expensive US equity market of all time, maintaining a normal weight in a passive index seems to us to be a decision that will likely be very costly. Yet despite this, it remains a popular path, with around 30% of all assets in the US equity market in the hands of passive indexers (see Exhibit 9).

The ultimate question for Trustee Smith and his recommendation to double down on the S&P 500 is: From a fundamental perspective, what does he believe justifies owning this market? Using our framework, you need to believe that growth in earnings and dividends are going to be significantly higher than what they have been historically. This argument and others7 seem like an enormous stretch to us. Earnings and the dividends from earnings have their roots in the growth of the economy, and it certainly does not appear as though the US economy is going to be rocketing back to the type of growth that we saw in the 60s and mid-90s. But if extraordinary fundamental growth is what you are relying upon to justify owning your S&P 500 index fund today, well…good luck to you, Trustee Smith.

If you, Trustee Smith, believe that P/Es and margins are going to stay high, allowing for earnings and dividends to do their normal thing, thus generating a decent return, you again are making some extraordinary assumptions that are certainly not based in anything related to the historic record of P/Es and margins. If you believe P/Es and margins are going to expand from today’s levels, creating another seven years similar to those we have just experienced, it becomes difficult to argue with you as at this point because you are defying all reason and logic. Or, more likely, you, Trustee Smith, are really a closet momentum investor extrapolating current market conditions well beyond their historical bounds and committing 17 other cardinal sins of behavioral finance that will ultimately wreak significant havoc on the portfolio you are charged with overseeing.

The (relative) good news

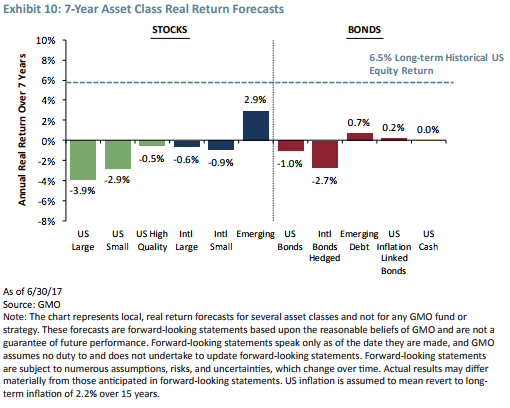

The cruel reality of today’s investment opportunity set is that we believe there are no good choices from an absolute viewpoint – that is, everything is expensive (see Exhibit 10). You are reduced to trying to pick the least potent poison.

This is fine if you have to invest relative to a benchmark or strategic objective. There are still some relative opportunities around – if you are willing to break Trustee Smith’s parochial frame. The last thing you should want to do is concentrate your portfolio in the world’s most expensive assets…which is, of course, what Trustee Smith is urging you to do.

Let’s return once again to valuation to make the case for non-US equities. As we look at our forecasts for international (EAFE) equities, we get a forecast of -0.6% real in local currency terms.8 EAFE Value is a bit better at 0.3%. EAFE suffers from a similar fate as US equities – elevated P/Es and profit margins but just much less so than their US counterparts. In absolute terms, EAFE is ugly, but just not as ugly as the US.

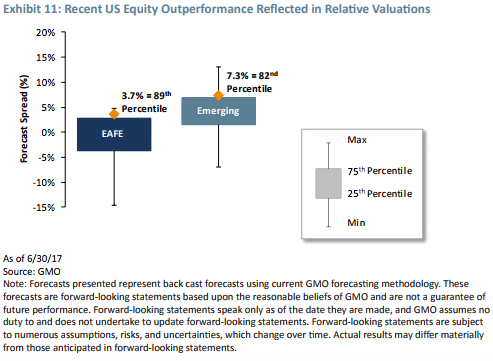

However, in relative terms EAFE stocks look much cheaper than US equities. In fact, if we go back to the early 1980s and look at the spread of EAFE versus the US (see Exhibit 11), the approximately 4% gap between these two major asset classes in the 89th percentile of observations means that 89% of the time the spread between these two assets is less than 4%. Basically, on only a couple of occasions in the late 1990s and during the European crisis of several years ago have EAFE stocks been as cheap as they are relative to US equities.

While US equity bulls can point to stronger economic fundamentals in the US than those we see in Europe and Japan, the issue for investors is not the relative health of the respective economies because we know that economic growth has little to do with subsequent equity returns. Plus, anybody that can pick up a newspaper can see the headlines and make that facile determination. The question for investors is “What’s in the price?” And as we look at the US equity market, relative expectations seem quite high and an awful lot appears to be in the price. However, international equities, while not cheap in absolute terms, certainly suffer from poor expectations and much better pricing. Their currencies also seem a bit cheaper relative to the dollar. Combine all this with significantly cheaper relative valuations and we believe international equities look a damn sight better than their US counterparts.

The story is similar within emerging market equities, but the news is actually better. Emerging equities have a forecast of 2.9% real (local terms) and cheap currencies to boot. Though emerging equities are expensive in absolute terms (slightly expensive on P/E), they provide a very strong return relative to US equities. The spread between emerging and the US is in the 90th percentile of observations going back to the late 1980s. We would think the currencies should add another tailwind (approximately 1%) to the asset class as well. That represents a significant premium to US equities. We all know the trouble emerging equities have had over the last several years – concerns for an economic slowdown in China, a depression and never-ending political turmoil in Brazil, Russia’s recent significant recession after the price of oil collapsed to name a few. There are numerous reasons to be worried about emerging. But again, the key question is “What’s in the price?” And to us, emerging market equities look poised to significantly outperform developed market equities. And if you look at the emerging value universe, the forecast looks even better, rising to 6.2% real. Now, Trustee Smith is going to be even less enamored of emerging stocks than international stocks because they have underperformed even more significantly over the last seven years. But he is completely missing one of the most crucial points in investing – starting valuations are going to cover the vast bulk of portfolio outcomes over any reasonable length of time.

For a relative investor (following the edicts of value investing), we believe the choice is clear: Own as much international and emerging market equity as you can, and as little US equity as you can. If you must own US equities, we believe Quality is very attractive relative to the market. While Quality has done well versus the US market, long international and emerging versus the US has been a painful position for the last few years, but it couldn’t be any other way. Valuation attractiveness is generally created by underperformance (in absolute and/or relative terms). As Keynes long ago noted, a valuation-driven investor is likely seen as “eccentric, unconventional, and rash in the eyes of average opinion.”

In absolute terms, the opportunity set is extremely challenging. However, when assets are priced for perfection as they currently are, it takes very little disappointment to lead to significant shifts in the pricing of assets. Hence our advice (and positioning) is to hold significant amounts of dry powder, recalling the immortal advice of Winnie-the-Pooh, “Never underestimate the value of doing nothing” or, if you prefer, remember – when there is nothing to do, do nothing.

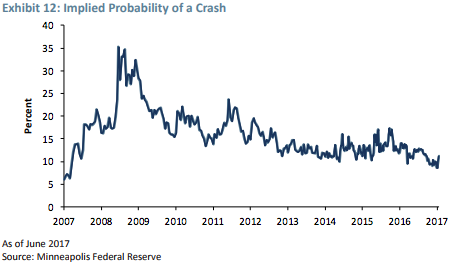

Markets appear to be governed by complacency at the current juncture. Indeed, looking at the options market, it is possible to imply the expected probability of a significant decline in asset prices. According to the Minneapolis Federal Reserve, the probability of a 25% or greater decline in US equity prices occurring over the next 12 months implied in the options market is only around 10% (see Exhibit 12). Now we have no idea what the true likelihood of such an event is, but when faced with the third most expensive US market in history, we would suggest that 10% seems very low.

But, one thing we have a high degree of confidence in is that Trustee Smith’s recommendation to concentrate his portfolio into indexed US equites, shun diversification, and sell international equities will ultimately increase the real risk in his portfolio, i.e., losing money, and make it even more difficult to meet the required rate of return. Good luck to you, Trustee Smith. It seems you are going to need it.

1 There will be more on this measure a little later in this paper.

2 As Graham and Dodd (1934) wrote, “Using a 5-, 7-, or preferably 10-year”average of earnings is a way of smoothing out the business cycle. Right now, 10-year average earnings are above their trend so this is actually a generous measure. As we have shown elsewhere (see “A CAPE Crusader: A Defense Against the Dark Arts,” a white paper by Montier, February 2014) a measure based on the trend 10-year earnings does even better at forecasting returns.

3 One of the authors (Montier) has regularly run this screen over time to assess the potential opportunity set from a bottom-up perspective.

4 Recall that the S&P was up more than 50% from the end of February 2009 to December 31, 2009. If a market is up 50%, holding fundamentals (earnings and dividends) constant, one would expect the forecast for the market to fall by approximately 7%. This is essentially what happened to our forecasts.

5 See Ben Inker, “Hellish Choices: What’s An Asset Owner To Do?” The April 2016 GMO Quarterly Letter is available at www.gmo.com.

6 An all-time favorite quote from Jeremy Grantham’s April 2001 Quarterly Letter: “The market gets increasingly inefficient as investors become more reluctant to bet against the benchmark…As the opportunities to add value increase, so does the personal risk, the career risk, and the business risk, until finally there will be incredible opportunities to make money and reduce risk that no one will dare take advantage of. We would like at least to be the last ones trying...”

7 See James Montier, “Six Impossible Things Before Breakfast” (March 2017). For instance, to believe that the US market offers fair value, you need to believe that it is capable of growing nearly three times faster in real terms than it has historically managed to do.

8 To get a total US dollar return for US investors, you need to add a forecast for the EAFE currencies to the forecast for EAFE. We have currency forecasts based on valuation and real interest rates, and developed currencies provide a very mild (less than 0.5% expected return) tailwind for EAFE equities.

Matt Kadnar. Mr. Kadnar is a member of GMO’s Asset Allocation team. Prior to joining GMO in 2004, he was an investment specialist and consultant relations manager at Putnam Investments. Previously, he served as in-house counsel for LPL Financial Services and as a senior associate at Melick & Porter, LLP. Mr. Kadnar has a B.S. from Boston College majoring in Finance and Philosophy and a J.D. from St. Louis University School of Law. He is a CFA charterholder.

James Montier. Mr. Montier is a member of GMO’s Asset Allocation team. Prior to joining GMO in 2009, he was co-head of Global Strategy at Société Générale. Mr. Montier is the author of several books including “Behavioural Investing: A Practitioner’s Guide to Applying Behavioural Finance”; “Value Investing: Tools and Techniques for Intelligent Investment”; and “The Little Book of Behavioural Investing.” Mr. Montier is a visiting fellow at the University of Durham and a fellow of the Royal Society of Arts. He holds a B.A. in Economics from Portsmouth University and an M.Sc. in Economics from Warwick University.

Disclaimer: The views expressed are the views of Matt Kadnar and James Montier through the period ending August 2017, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2017 by GMO LLC. All rights reserved.

© GMO

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All