On Value in the Emerging Markets

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits“Value” is an over-utilized term within the investment management industry. A wide range of fund managers employing disparate strategies claim to utilize “value disciplines” or to follow a “value approach.” In truth, there is no standardized definition for the notion of “value investing.” The progenitors of the value discipline, Benjamin Graham and David Dodd, never themselves used the term to describe their work.1 Instead, they explained an investment process that they believed to be both coherent and capable of producing attractive returns. A critical feature of the discipline was that it sought securities of a deeply discounted nature. Later, other investors sought to claim reference to Graham and Dodd’s work; they developed the term “value investing” as a means to describe their efforts.

In our view, “value investing” is an investment approach that seeks to purchase a security at a discount to its intrinsic worth. We believe there is considerable theoretical and empirical evidence to support the idea that a value discipline generates attractive returns for long-term investors. However, the best support for a value-oriented discipline rests on a simple and elegant first principle: investment returns are inversely proportional to the price paid relative to intrinsic worth. This practice accounts for the “discount” embedded in the definition of value investing.

Defining the second element of our definition, “intrinsic worth,” is significantly more complex. The identification of “value” has evolved over time and varies by practitioner, making a systematic, empirical study of its historical returns problematic. Nevertheless, the most comprehensive empirical study of the subject of which we are aware is a paper called “What Has Worked in Investing” by Tweedy, Browne Company, LLC.2 The paper represents a collection of studies through the decades that have measured the returns corresponding to discrete investment characteristics - such as price-to-book value , price-to-earnings, or dividend yield, among others - associated with a value discipline. The paper’s conclusion is that there is a recurring pattern of positive correlation between these characteristics and excess return when measured over long periods of time. This conclusion confirms what we intuitively knew based on the first principle stated above.

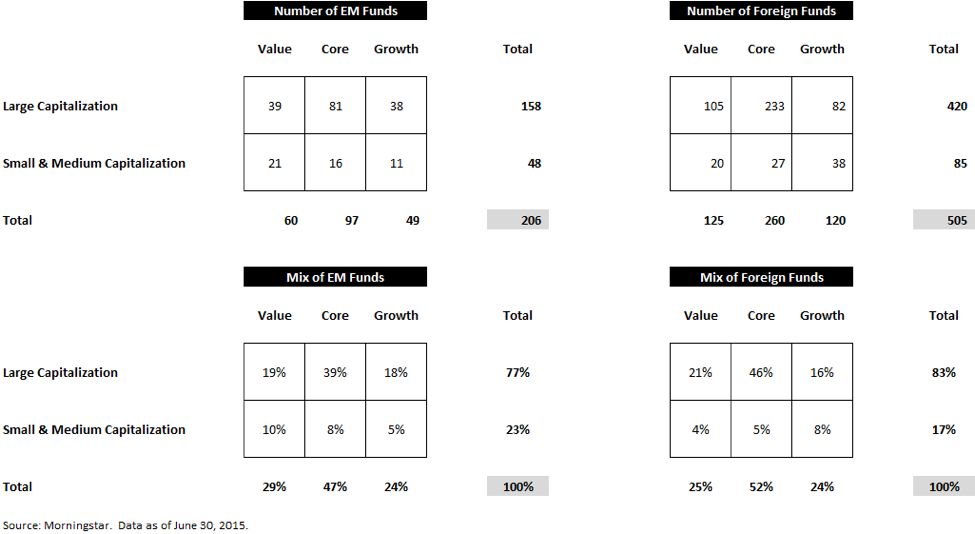

Investors in the United States have long recognized and exploited this association, as evidenced by Morningstar’s mutual fund data. That database indicates that approximately 481 U.S. mutual funds, or 21% of the total, are self-identified as value strategies.3 The number of U.S.-based mutual funds investing in developed market (ex-U.S.) equities, as defined by Morningstar’s “Foreign” fund categories, that self-identify as value strategies is approximately 55, or 11% of the total.4 Clearly, value-oriented strategies comprise an important component of the global investment universe. We presume that this is because investors recognize that over long periods of time, “value” provides attractive returns.

Oddly, though, the merits associated with “value” have not translated to emerging markets. It is quite rare to observe emerging market funds that deploy value-oriented investment disciplines. Using the same Morningstar data, we note that only six U.S. mutual funds in the “Diversified Emerging Markets” category pursue value strategies – only 3% of the total.5,6

What is striking about the paucity of emerging market (EM) value strategies is that one might think the approach would yield superior returns in this universe given the more inefficient nature of developing economies and financial markets. One example of this inefficiency is the higher cost of capital in emerging markets. The higher interest rates associated with EM are indicative of the higher return accorded to capital in these markets. As the cost of capital is relatively high, one might reasonably theorize that the present discount to intrinsic value should be substantial, in corresponding fashion. The compounding of such interest over the long time horizon characteristic of a typical value discipline illustrates the potential remuneration to the approach in this universe – put differently, it illustrates why one is likely to find significant discounts to intrinsic worth.

With such apparent advantages for a value investment discipline, why do so few strategies exist? Is there an impediment to profitable value strategies in EM that is absent from developed markets? Is the opportunity set too small, or insufficiently attractive despite the higher discount rates employed in these markets, or are value traps simply too complex to unravel? It is with this sense of opportunity and curiosity that Seafarer decided to explore the emerging markets and look for answers.

VALUE INVESTING IN EMERGING MARKETS: A WORKING DEFINITION

The Criteria

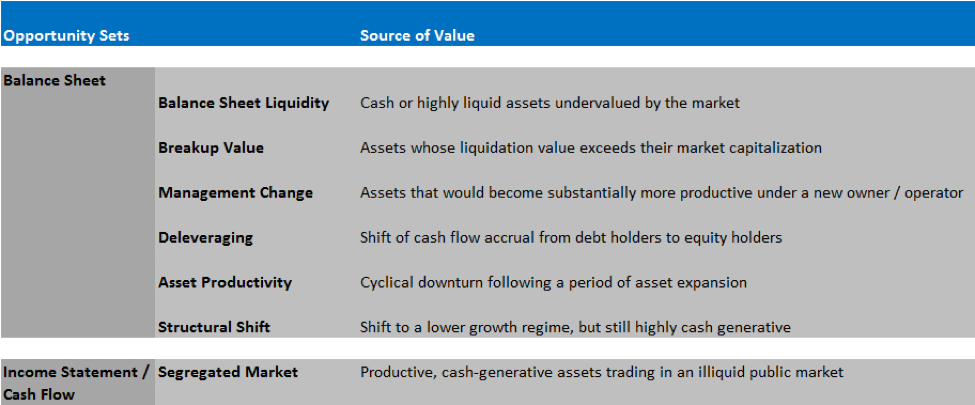

The search for value has traditionally tended to concentrate on three commonplace criteria: a low price to earnings ratio (P/E), a low price to book value multiple (P/BV), or a high dividend yield (Dividends/P). The problem inherent in such definitions is that they define value solely in terms of low multiples. While low multiples can be one signal of potential value among many, they are not determinant of total returns in and of themselves. Recognizing the difficulty of authoritatively defining “a discount to intrinsic value,” Figure 1 takes a different approach, based upon Seafarer’s research, by defining the concept in terms of the individual sources of value that give rise to opportunities. This approach attempts to better illustrate the essence of a value discipline than simply searching for low-multiple stocks.

While we make no claims to provide the definitive or only approach to define value, Figure 1 does attempt to provide a working one, based on our own experience as value-oriented investors primarily concerned with emerging markets. These factors, while relevant globally, have been customized to identify opportunities most likely to arise within an emerging markets setting.

Figure 1

Seafarer has identified seven distinct opportunity sets that describe a specific source of value, and associated potential returns. The first two categories, balance sheet liquidity and breakup value, relate to the value that a company has produced historically, with a residual portion of that past value still evident in the company’s balance sheet, or net assets. The value such assets command in public markets may differ from the value in private markets, or the book value. Validating such divergences is one aspect of price discovery. While these opportunities exist globally, what makes them more pronounced in EM are the cyclical changes in the cost of capital in developing economies.

Companies can also enjoy a critical asset that resides outside of the balance sheet: human capital, such as the personnel and management. Changing or upgrading management can represent an opportunity to realize the value latent in an otherwise dormant enterprise. While this source of value is not unique to the emerging markets, what makes it particularly relevant in developing economies is the generational shift in company ownership that can potentially lead to the employment of professional management. The divestment of government stakes in state-owned enterprises (SOEs) is another form of management change. This opportunity set is large as approximately 60% of private sector EM companies with $1 billion or more in revenue are owned by the founding family.7 Even allowing for cultural differences in management approaches between developed and emerging corporates, it is reasonable to expect a gradual shift toward the division of ownership and management as capital requirements increase with scale.

The deleveraging opportunity set shifts the focus to the providers of capital to an enterprise. The high growth rates associated with developing countries often lead to rapidly expanding asset bases financed with debt, which divert cash flows from the providers of equity capital to the suppliers of debt. The process tends to reverse over time as the asset base matures and debt is reduced, leading to meaningful gains for equity stakeholders.

The corollary of high growth rates is cyclical downturns. The asset productivity opportunity set captures this source of value. While this is a universal source of opportunity for a value approach, the distinguishing factor in EM is the high growth rates and meaningful cost of capital changes that characterize cycles in developing economies.

The structural shift category recognizes the often overlooked idea that despite the stereotype that emerging economies enjoy high rates of growth, companies and industries relay each other in leading that growth. As an economy matures, the underlying companies that compose it go through their own maturation curve at varying rates, yielding publicly-listed companies that shift to a lower growth phase in their lifecycle. This phenomenon often leads to a reshuffling in the company’s investor base as growth investors vacate it, which tends to yield opportunities for a value approach.

The segregated market category captures occasions when rather than a shift in the investor base, it is the size of the potential investor base, i.e. the overall market liquidity, that represents an opportunity to find value. There are myriad, well-managed companies in emerging markets that trade at a discount to their intrinsic worth for no other reason than that their stock has low liquidity. For instance, the low liquidity associated with small capitalization stocks can sometimes cause them to trade at substantial discounts to intrinsic value; likewise, limited liquidity in frontier markets can mean that well-established companies trade at meaningful discounts. The source of value in this instance is that a company’s liquidity has no bearing on the cash flows that accrue to shareholders.

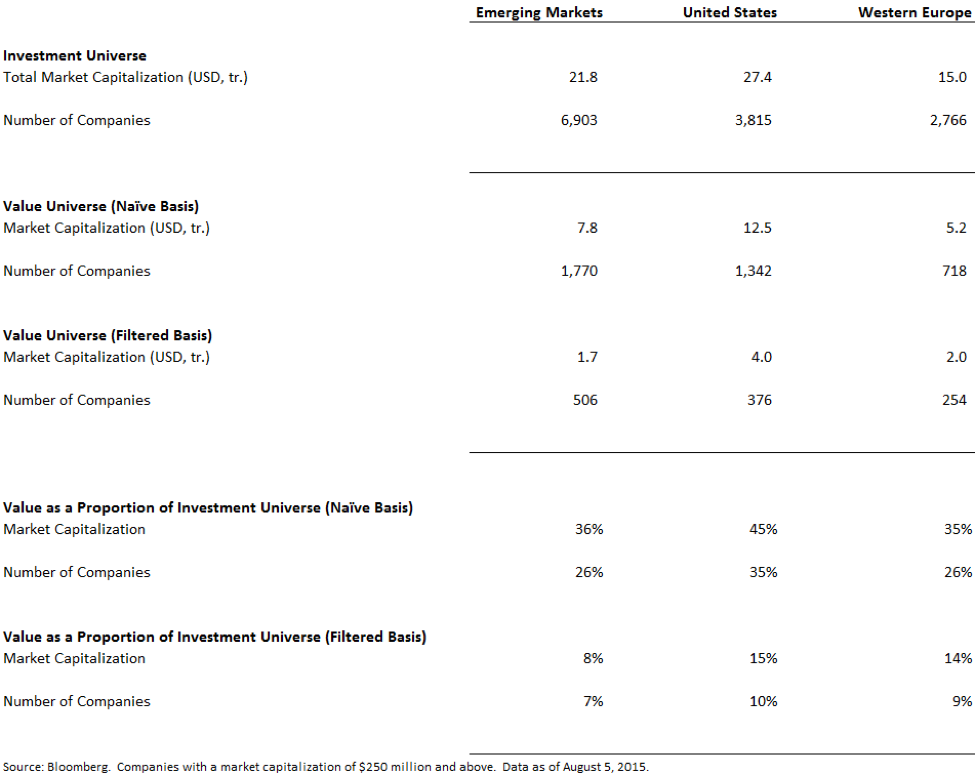

The Value Universe: A Global Comparison

The primary take away from Figure 2 is that EM overall, and the value universe within it, do not appear to be niche markets. Figure 2 shows the size of the value universe in EM – including Chinese A shares– as defined by the development of criteria specifically targeted at each source of value identified above. In the same manner that low multiples are a potential sign of value and not a driver of returns, the criteria employed in the search for value investments can only identify potential opportunities, not actual value. Only fundamental research can confirm whether a security offers value. It is in that spirit that Figure 2 outlines two value universes. The first, a basic universe that quantitatively captures a broad set of stocks that meet the minimum criteria for each value category, and a second, core universe that complements the basic qualifying criteria with more variables designed to screen out potential value traps.

Figure 2 also shows the result of performing the same search in the U.S. and Western European markets. Returning to one of the questions raised at the beginning of this paper, we can answer that total market capitalization, or its implied investment capacity, probably do not account for the paucity of value strategies in EM.

Figure 2

Value in Emerging Markets: Seven Different Sources

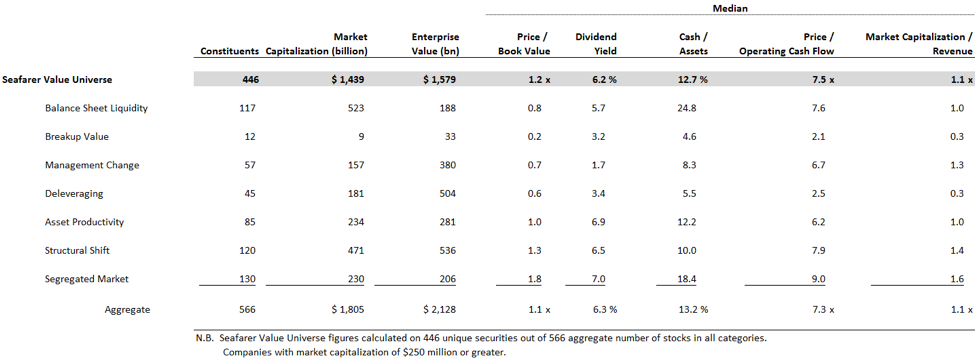

Figure 3 outlines the salient characteristics of value and each of its categories in EM. The parameters presented paint a picture of the landscape in broad strokes, and do not constitute a comprehensive list of the variables used to identify companies in each value category. It is important to note that there is a large variance of results around the median figures shown, illustrating the idea that value extends beyond the traditional definition of low multiples. Indeed, one of the interesting conclusions from this study is that defining value in fundamental terms often leads to companies trading at high multiples.

Figure 3

With such disparities – prevalent throughout the EM value universe – noted, we now take a closer look at the seven main sources of value in EM, noting for each the idiosyncrasies related to industry, geography, or valuation and the different manner in which value manifests itself.

1. Balance Sheet Liquidity

Source of value: Balance sheet liquidity relates to a firm’s net cash or liquid short-term net assets. Companies can often trade near their cash or liquid net asset values if the underlying operations generate losses that will consume said liquidity, or the nature of the business is working capital intensive. There is, however, a third type of balance sheet liquidity that should generate most value opportunities in this category: accumulated operating cash flow, not previously shared with minority shareholders (i.e., large amounts of undeployed and unencumbered cash on the balance sheet).

There is a subset of companies in EM that routinely decline to return excess cash to shareholders, neglecting to pay dividends or engage in share buybacks. Some use it for empire building – usually destroying capital in the process.8 Others simply sit on the excess cash. This is a prevalent source of value within the EM, but unfortunately such value has languished on these companies’ balance sheets, as minority investors often lacked sufficient leverage to force companies to disgorge such cash. However, this situation is beginning to change, given the push for improved governance in many of the major emerging markets.9 For example, in late 2014 the Korean National Assembly passed legislation that aims to increase the return of capital to shareholders and reduce the barriers to competition imposed by large conglomerates. These changes are motivated by the recognition that the conglomerates that once propelled the country’s development are now a source of economic stagnation.

Criteria: The practical pursuit of value here goes beyond simply searching for a high cash balance relative to market capitalization. It also measures cash relative to assets and enterprise value (EV); while guarding against cash coming from debt as opposed to operating cash flow. In order to identify a set of potential value opportunities - as opposed to simply stocks that quantitatively appear cheap – the search focused on companies that show signs of incrementally returning more of their cash balance to investors by reducing retained earnings or cancelling shares.

Manifestations of value: While no single country dominates the category, certain sectors do: real estate, commodity trading houses, engineering and construction companies (E&C), as well as brand-based enterprises, such as sports apparel companies. The common denominator in these industries is a high working capital (WC) intensity, originating from apartment purchase deposits, or down payments related to infrastructure new-order growth. Brand-based businesses tend to generate positive free cash flow and undercapitalize brand equity, resulting in cash-rich balance sheets. An example of such a business is a Chinese sports apparel company that only capitalizes $3.4 million as trademark value, whereas it has $383 million in net cash on the balance sheet, equivalent to 56% of its equity value.

Beyond identifying broad sector categories to potentially hunt for liquidity-related value, these screens prove useful in shedding light on EM company operations. For example, in checking for the cash component of book value (BV), two groups of companies surface as having a very low residual BV: E&C, and consumer products. The search criteria employed lays bare the fact that the former category has a low residual BV because it generates little retained earnings over the course of a full cycle (the high negative WC previously referred to turns positive), whereas consumer companies have a low residual BV because they tend to payout most of the substantial retained earnings they generate. This latter case corrects the misconception that EM companies do not constitute a significant source of dividends.10

Value traps: Not all liquidity that glitters is gold. Chinese real estate companies are a case in point. A subset of these enterprises trades at a seemingly cheap 0.8x P/BV with a 7% dividend yield. As attractive as that combination looks, expectations are tempered by the fact that they have paid out in dividends over 60% of the cash flow from operations they have generated over the past five years (before capital expenditures) – thus, effectively borrowing against new projects to payout dividends. That’s why a slowdown in Chinese credit growth is of such importance to market returns. More generally, in examining high growth markets such as EM, companies operating in industries with negative working capital may look deceptively cheap and liquid, thus the importance of screens based on fundamental drivers, as opposed to simply low multiples.

2. Breakup Value

Source of value: Breakup value relates to the long-term segment of the balance sheet, rather than to short-term liquidity. It is common for the price of assets in the public market to fall below their depreciated book value. In the case of fungible operating assets (vessels or aircraft for example) a company may trade below replacement cost if it operates at an efficiency level below the global norm. In the case of non-tradable assets, based on a concession for example, a company may trade below its liquidation value if its operations underperform for non-concession related reasons.11

Criteria: While a low price to book value multiple would seem ideal to pursue this asset-based category of value; using it on its own fails to guard against value traps. Instead, the search in this category focused on the cash flow yield of operating assets, combined with a low EV in relation to the book value of said assets. Searching for value in this manner, instead of simply looking for a low price to book ratio, ensures that the assets are productive, highlights the potential for cheapness, and guards against debt holder claims on said assets.

Manifestations of value: The results in this category are remarkable in the dominance of Russian companies in general, and Russian utilities in particular. Under normal conditions, the fair value of a productive asset is higher than its price to book value (P/BV > 1x), in proportion to its productivity. While the cash return of Russian utility assets is in the teens, they trade at an abnormally low median P/BV of 0.22x. And even though they are burdened with significant debt, their ability to service such debt is very high due to generous interest cover ratios (>10x). Should one wish to pursue this avenue, this is where research work would begin in pursuit of the currency denomination and maturity of the debt, as well as reinvestment requirements, in order to determine how much of said cash flow will actually accrue to shareholders. Nevertheless, in light of the decline in the U.S. dollar price of Russian equities since the collapse of oil prices and the Ukraine conflict, it makes intuitive sense that Russia should dominate the “breakup value” sleeve of EM.

More generally, low turnover, high margin businesses tend to populate this category. The search for potential value here revealed a port company and a property management stock, as potentially offering value given their low leverage despite the high asset intensity, combined with an attractive cash return on operating assets.

Value traps: A good method for identifying value traps in this category is to search for high dividend yield stocks. The reason a high dividend yield correlates with a value trap in examining breakup value is that the market is already discounting the unsustainability of the dividend. This tends to occur with asset intensive businesses. When their margins cannot support the costs of expansion, they tend to leverage the balance sheet, threatening the dividend. Such is the case of an Indonesian cement company, which paid a dividend while increasing capital expenditures together with debt, and consuming what used to be a meaningful cash balance. The shares trade below book value and offer a 6% dividend yield, neither of which are likely to offer value in this case, due to the firm’s deteriorating demand fundamentals going forward. The real source of risk in this case is not simply that a company is entering a cyclical downturn, as such a risk is transitory. The actual risk is that management weakened the balance sheet during the cyclical expansion to the point that it is unlikely to survive a downturn of any meaningful severity or length. Such a risk is terminal, and it was created during the expansion phase of the cycle.

3. Management Change

Source of value: While some EM assets display signs of being undervalued by the market for macro-related reasons, there are also companies that show signs of potentially being cheap due to poor management decisions. Value in this category arises when cumulative value destruction leads to either a change in management by the control party or industry consolidation. A third solution to an asset’s unsustainable underperformance is, of course, bankruptcy. This is the outcome fundamental research must guard against and the value trap screens evaluating on simple multiples have difficulty detecting.

Criteria: It is important to note that underperforming enterprises tend to trade at very high multiples if earnings are low or book value is depleted. The search in this category centered on the combination of low margin, low turnover, and high leverage. Pursuing value here would ultimately require fundamental research to validate the presumption of inevitable management change in the foreseeable future.

Manifestations of value: What stands out in this category is the preponderance of Chinese A shares (Mainland stocks listed in Shanghai or Shenzhen). These companies have grown revenue and assets meaningfully over the years. Yet, they display dismal asset turnover and margins. Increasing debt has financed the growth that their operations could not support. Given how credit is generally directed and priced in the country (via government rather than free market direction), it makes intuitive sense that Chinese companies dominate this sleeve. Indeed, while China is still undergoing a long process of interest rate liberalization, Chinese banks effectively lend at the benchmark rate (set by the People’s Bank of China) plus or minus a few basis points.12 This practice likely means that they fail to price risk adequately. In addition, the country’s five-year economic plans tend to direct bank lending, crowding out the private sector. Before confirming preconceptions and writing off Chinese companies as investment candidates, it is important to note that the data revealed here is precisely why China has engaged in a corporate productivity drive for a number of years now.13 Some companies are further along that process than others and that is precisely where the opportunity lies.

Value traps: Avoiding traps in this category hinges on understanding the control party and its intentions. Government-owned entities tend to have unlimited capacities to sustain losses, since the government acts as the explicit or implicit guarantor of the debt (also known as “moral hazard”). Thus, the limit to debt extension is not the asset value that nominally acts as collateral to the debt, but rather the government’s capacity to tax its citizens. The case of a very large Chinese shipping company serves to illustrate the point. This enterprise continued to expand capacity in the face of operating losses to serve the government’s foreign policy interests. Given its status as a state-owned enterprise, it has managed to continually raise debt to over twice the level of equity, in spite of economic losses. Unless there is evidence of a privatization drive, these entities tend to represent poor investments. An extension of this line of reasoning is to avoid global industries where state-owned competitors command substantial market share, as these will destroy the economics of the entire industry, including private sector participants.

A corollary of the reasoning above extends to public-private-partnerships, where private capital partially funds public infrastructure projects. The criteria employed in this sleeve identified a privately-owned, Asian infrastructure company that builds, owns, and operates government-sponsored infrastructure projects. The need for infrastructure and financing in Asia allowed this company to raise capital on the promise of substantial asset-based returns. It took some time, but the share price eventually collapsed close to 90% from its peak, after investors recognized the continuous shareholder dilution and long maturation cycle of its assets. Now that primary valuation metrics have collapsed, there is potential for value in this security as its assets mature. However, the outstanding question is whether this company can earn a return on equity above its cost of equity, given the price paid for assets at a time when capital was cheap. The company cannot grow either, as it would entail substantial dilution at a low valuation. Without growth, and given the massive amount of debt on the balance sheet, deleveraging based on asset maturation means that the great majority of cash flow over the projects’ lifetime will accrue to the owners of debt. Accordingly, it is quite likely that this company represents a trap, even as its market price is below book value.

4. Deleveraging

Source of value: By sustainably reducing their debt burden, companies engaged in deleveraging increase the future cash flows that accrue to shareholders, thus creating value. This is a particularly interesting area to look for value in EM for two reasons: first, it is easier for companies to overextend their balance sheets in high growth environments, such as EM. Second, enterprises engaged in paying down debt tend to suffer from a downward shift in growth, leading to an exit of growth investors and lower valuations.14 The point that is usually overlooked in these circumstances is that growth tends to normalize when the deleveraging cycle nears its completion.

Criteria: The criteria used to search for opportunities in this driver focused on the composition of enterprise value versus the capital structure appropriate for an industry, while guarding against an apparent inability to service debt. More generally, each industry has a characteristic turnover and margin combination that supports a natural level of leverage for that industry. Companies with balance sheets that deviate from their natural composition for prolonged periods of time tend to suffer from lower equity valuations. The key to realizing value in this category is to identify a realistic path to balance sheet normalization, which is usually accompanied by a rerating of equity valuations.

Manifestations of value: Unsurprisingly, given sharp price declines in commodities and currencies during 2014 and 2015, materials and energy companies dominate this category. A salient example is a global cement company, whose leverage increased beyond the limits of conventional debt covenants as its profitability deteriorated following the 2008 crisis. Trading below book, the case for potential value in this stock resides on the replacement value of its global assets relative to the debt burden (e.g., the company can normalize its balance sheet through asset sales), together with margin normalization.

Value traps: Potential traps in this sleeve relate to companies with high leverage that don’t have the balance sheet to survive a prolonged downturn, or companies that have unclear asset value. An example is a sub-scale, Latin American iron ore producer. Like many other companies in this industry, it consumed its cash and increased leverage to invest in additional capacity, while concurrently paying dividends that often exceeded free cash flow. The difference with other iron ore producers is that this company is likely on the upper end of the global production cost curve, thus reducing its ability to survive as the lowest cost producers displace other competitors. Thus, the very low price to book value ratio, likely represents a trap.

5. Asset Productivity

Source of value: The asset productivity category of value relates to demand and supply cycles. Specifically, it refers to assets operating at low capacity utilization due to a demand downturn, or following a period of capacity expansion. Investors have a tendency to extrapolate short-term dynamics, often overlooking that cycles are self-correcting if the price mechanism is allowed to work.

Criteria: The search for value here focuses on comparing a company’s current valuation against the long-term cash flow it has generated historically. This is one of the best methods to look through earnings cycles, and gauge the potential to discover value in a security. Only fundamental research can determine the actual presence of value by assessing normalized cash flow, as a distinct concept from historical cash flow generation.

Manifestations of value: An industry that exemplifies a demand downturn coincident with a supply glut is dry bulk shipping. This industry should prove fertile ground for finding value stocks in EM. The extended and sustained demand lift from China, particularly after it joined the World Trade Organization, coupled to central-bank-induced cheap capital across the world, resulted in a miscalculation problem. Asset owners forecast demand would continue to rise consistently for the foreseeable future, and they rushed to place new vessel orders to front-run lengthening shipbuilder order-books and rising vessel prices. The climax of this situation was embodied in second-hand vessels trading at higher prices than new ones during the 2007-2008 time period. While this circumstance was logical given the economics of the industry at the time, it should have also served as the harbinger of the downturn the industry is currently undergoing. One stock in this category that potentially offers value is a dry bulk shipping company trading at a very attractive price to book ratio. Unlike most similarly cheap stocks in the industry, this company has one of the lowest cost fleets globally, together with one of the least levered balance sheets. Thus, the likelihood of not only surviving the downturn, but coming out of it with an enhanced competitive position is high.

Value traps: Following from the above discussion, traps in this category would consist of companies with high leverage that deployed new capital pro-cyclically (i.e., purchased assets expensively at the peak of the cycle). Other potential value traps would be businesses whose normalized cash flows do not correspond to their historical track record. Examples among these companies include a highway operator trading below book that faces traffic diversion to new roads; its cash flows are unlikely to ever recover to the previous peak. Another example: a media company challenged by a new regulatory environment, and a wireless operator whose future cash flow suffers from deteriorating business economics due to competition.

6. Structural Shift

Source of value: Investors pursuing growth have traditionally focused on emerging markets as their hunting ground. Thus, it is not uncommon to find cash flow generative businesses trading at attractive valuations when their growth plateaus. The source of value in this category is not only the price paid for the underlying cash flow, but the fact that investors tend to underestimate the contribution of dividends to total return.10

Criteria: The search for value in this category focuses on finding incrementally higher dividends or buybacks, and potentially an outright reduction in invested capital, combined with business sustainability.

Manifestations of value: The list of stocks in this category contains many telecommunications companies operating in highly penetrated markets, tobacco stocks, and traditional media (print) businesses. A representative example is an Eastern European tobacco stock, which contrary to expectations, actually grew revenue modestly during years when the state taxed away the company’s pricing power. Not only is revenue stable, but the company has no debt, and the dividend yields 8%.

Value traps: An apt contrasting case to the one above is a Brazilian consumer discretionary company that finds itself in a similar position of suffering a sharp deceleration in revenue growth over the past three years. While this stock also enjoys a healthy dividend yield of 7%, the difference with the Eastern European company is that the management of this stock chose to consume cash, and almost triple debt to finance a dividend well in excess of free cash flow. The Brazilian stock has yet to find a natural level for its revenue base and growth rate and needs to cut its dividend; the Eastern European company’s cash flow and dividend seem eminently more stable and secure. Not all 7% to 8% dividend yields are created equal.

7. Segregated Market

Source of value: The final potential source of value opportunities in EM relates to stocks that are in “segregated markets.” These are markets that are naturally small, obscure and typically disconnected from the global flow of liquidity. Seafarer believes that securities that trade in such markets might naturally trade at discounts to their intrinsic value due to their relative illiquidity. We believe a patient value investor can harvest an “illiquidity premium” by investing carefully in such segregated markets. Most “frontier countries” constitute classic examples of segregated markets, as their capital markets are small and thinly traded, potentially causing liquidity-driven discounts.15 As figure 2 shows, the number of listed stocks in emerging markets exceeds that of the United States and Western Europe. Their combined market capitalization is of comparable size. As such, there are myriad, well-managed companies that are typically only apparent to domestic investors. As capital markets in EM gain depth, the value inherent in these companies should surface in the form of higher security prices.

Criteria: The search for value here focused on finding businesses with a sensible mix of reinvestment and capital return designed to sustain them as going concerns, and trading at a valuation inconsistent with this dynamic.

Manifestations of value: Small-capitalization and medium-capitalization companies tend to dominate this space. What is remarkable regarding this group of companies is the combination of attributes seen in Figure 3: the median stock trades at an attractive P / CFO of 9x, with a dividend yield of 7%, and significant cash on the balance sheet. Other categories of value offer more attractive terms on any single variable, but not in this combination. One of the companies in this group trades at the median levels cited, and has been listed in Hong Kong since 1992. Despite its long track record spanning several business cycles with reasonably consistent cash flow generation, the 8% dividend yield indicates the market still discounts its cash flows as if there were low future visibility.

Value traps: For an example of another company in the same group trading at similar levels that likely does not offer value, consider the case of a Hong Kong-listed media company. The reason for the different assessment of similar dividend yields is that this second company is a media enterprise facing new competition in its traditionally protected home market, and its efforts to explore new avenues of growth are falling short of expectations. This is a case that warrants an assessment of normalized cash flow as distinctly different from the company’s historical record.

CONCLUSION

Convinced by the weight of theoretical and empirical evidence in support of a value investment discipline, we were perplexed by the paucity of value-oriented strategies in the emerging market universe – all the more so, as we would assume that a disciplined, fundamental approach could capitalize on markets that are presumably less efficient than their developed world counterparts. We then set out to answer the questions posed by such a seemingly obvious gap. Aware of the limitations of traditional screens to systematically capture the essence of a value discipline, we sought to redefine the approach in terms of the sources of value that we believe can generate consistent returns, while attempting to highlight the value traps associated with sometimes idiosyncratic markets.

This exploration discovered a large value opportunity set with an aggregate market capitalization of $1.4 trillion, characterized by financial metrics that strongly suggest the pervasive presence of discounts to intrinsic worth.

After examining most possible deterrents, this study found no compelling reason that investors would forgo value investing in the emerging markets. On the contrary, this paper documented a potential universe that was both large and compelling. The fact that such an opportunity set remains largely untapped should make it all the more attractive to disciplined value practitioners.

1 The preeminent text that defines Benjamin Graham and David Dodd’s investment process is entitled Security Analysis. The approach recommends investors buy stocks with undervalued assets and that eventually those assets would appreciate to their true value in the marketplace. Seafarer’s analysis of Security Analysis indicates the authors do not utilize the phrase “value investing” within that work. In accompanying commentary of the sixth edition of Security Analysis, Howard Marks, Chairman of Oaktree Capital Management, suggests the phrase is absent because, when the text was first published, “the term ‘growth stock investing’ was relatively new (and in its absence, there was no need for the contrasting term ‘value investing’).” Graham and Dodd, Security Analysis: Sixth Edition, 2008.

2 Tweedy, Browne, Company, LLC. “What Has Worked In Investing: Studies of Investment Approaches and Characteristics Associated with Exceptional Returns,” 1992. http://www.tweedy.com/resources/library_docs/papers/WhatHasWorkedFundOct14Web.pdf.

3 Source: eVestment. Universe is U.S. mutual funds. Data as of June 30, 2015.

4 Source: eVestment. Universe is U.S. mutual funds classified by Morningstar in the following six “foreign” fund categories: Foreign Large Value, Foreign Large Blend, Foreign Large Growth, Foreign Small/Mid Value, Foreign Small/Mid Blend, and Foreign Small/Mid Growth. Data as of June 30, 2015.

5 Source: eVestment. Universe is U.S. mutual funds in the “Diversified Emerging Markets” category. Data as of June 30, 2015.

6 Morningstar’s fund data reveals a normal distribution of strategies across the value-core-growth spectrum, based on the categorization of individual stock holdings into one of the three styles identified. Morningstar’s methodology grades stocks on a relative curve. As a result, funds that tend to own stocks that happen to trade at a cheaper-than-average valuation may be considered value strategies, even if the stated fund objective is a different one. See table below for Morningstar’s categorization of U.S. mutual funds in the “Diversified Emerging Markets” category and “Foreign” categories, based on its assessment of individual stock holdings (i.e. not based on the funds’ self-identified style).

In the case of U.S. mutual funds in the “Diversified Emerging Markets” category, while Morningstar suggests that 60 funds, or 29% of all strategies, may be stylistically considered as value, the number of funds that actually cite the pursuit of value stocks as their objective is 6, or 3% of the total. In contrast, the number of U.S. mutual funds classified in a “Foreign” fund category that self-identify as value strategies is approximately 55, or 11% of the total.

7 Åsa Björnberg, Heinz-Peter Elstrodt, and Vivek Pandit. “Joining the family business: An emerging opportunity for investors.” McKinsey on Investing, Number 2, Summer 2015. http://www.mckinsey.com/insights/winning_in_emerging_markets/the_family_business_factor_in_emerging_markets

8 Richard Dobbs, et al. “Beyond Korean Style: Shaping a New Growth Formula.” Pages 16, 19, 37. McKinsey Global Institute.

9 There are currents of change gathering pace within major emerging markets in support of the interests of minority shareholders:

Korea’s legislative changes aimed at increasing the return of capital to shareholders and reducing the barriers to competition imposed by the {chaebols}[?] is probably the most emblematic of the undercurrents gaining critical mass. At the end of 2014, Korea’s Ministry of Strategy and Finance issued new legislation to tax retained earnings that are not distributed to shareholders, invested, or paid to employees. The aim is to address the infamous capital hoarding of Korean corporates. For more information, see “South Korea: Notable 2015 Tax Law Amendments Affecting Foreign Invested Companies and Foreign Individuals,” International Tax Review, 27 January 2015. http://www.internationaltaxreview.com/Article/3421924/South-Korea-Notable-2015-tax-law-amendments-affecting-foreign-invested-companies-and-foreign.html.

China’s drive to raise the productivity of state-owned enterprises is a form of potential incremental shareholder return. The higher dividend payout demanded by China’s State-Owned Assets Supervision and Administration Commission (SASAC) is another example. Furthermore, one of the unintended (or perhaps intended) consequences of Beijing’s anti-corruption drive is to reduce capital misallocation, which directly enhances returns to minority shareholders. For more information, see “China announces plan for reform of state-owned enterprises, “ Financial Times, 2014 July 15 (http://www.ft.com/intl/cms/s/0/07928638-0c24-11e4-a096-00144feabdc0.html#axzz3uEKFAWYp) and {Chinese SOEs and the Way Forward}[http://www.seafarerfunds.com/commentary/chinese-soes-and-the-way-forward/].

10 The dividend contribution to total return for EM stocks is meaningful in absolute terms, and exceeds that of U.S. equities.

12 Cindy Li. “China’s Interest Rate Liberalization Reform.” Country Analyst Unit. Federal Reserve Bank of San Francisco. http://www.frbsf.org/banking/files/Asia-Focus-China-Interest-Rate-Liberalization.pdf.

13 Xinhua. “News Analysis: Chinese SOEs to ride new reform wave.” 14 September 2015. http://news.xinhuanet.com/english/2015-09/14/c_134623014.htm.

14 Luigi Buttiglione, Philip R. Lane, Lucrezia Reichlin and Vincent Reinhart. “Deleveraging? What Deleveraging?” International Center for Monetary and Banking Studies. September 2014.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All