Emerging Value and Margin of Superiority

Why would a value manager buy more of an asset that has just gone up?

Ben Inker

Long-time GMO clients have become accustomed to a certain kind of behavior from our asset allocation portfolios. If they are reading stories about how well an asset class has been doing, chances are pretty good that their next account statement will show that we are a seller of that asset (assuming we owned some in the first place). If, on the other hand, headlines are about how horribly things are going for an asset class, our clients have come to expect to see us buying in the coming quarters. But recently we made a move across a number of our asset allocation portfolios that goes counter to that general pattern. After a strong first half of 2017 for emerging equities that saw them rise over 18%, we actually bought more emerging in early July. It seems like a non-intuitive move for us to make, but we believe it is the correct one despite the fact that the prospective returns to emerging equities have dropped a bit since the beginning of the year. Even though the absolute expected return for emerging market value stocks has decreased, we believe the margin of superiority of emerging value over other assets has actually increased. As its superiority is higher and emerging-specific risk is relatively benign, our willingness to bear its risk has increased at the margin, which created the opportunity for us to increase our allocation.

Emerging value is extraordinary today

There are a couple of important points to make about our decision to buy more emerging recently. The first is that despite the strong returns of emerging equities so far this year, the group we are most interested in, emerging value, hasn’t been particularly extraordinary. MSCI Emerging is indeed up over 18% through the first half of the year, but value has underperformed by 4.8% in the period and 3.5% of the returns to emerging were due to currency moves. That leaves emerging value up about 10% in local terms, about on par with stocks around the world. Given that fair value for the group compounds at around 6% real annually or 3% in a half year, this means emerging value should have gotten about 6% more expensive over the period, which would cause its forecast to drop by around 0.8%, all else equal.1 In this particular period, all else has been more or less equal and the forecast has indeed gone down by 0.8%, from 7% to 6.2%. Our next favorite equity assets, EAFE value and US quality, have seen their forecasts fall by 0.3% and 1.1%, respectively.

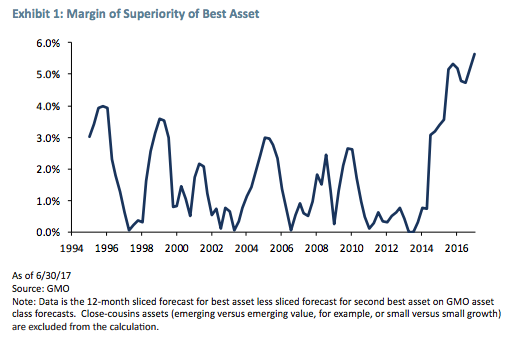

But the second point to make is that we have tried to learn the lessons of history with regard to how to use value to actually outperform. As I wrote a few years ago in “Divesting when Discomfited” and touched again on last year in “Keeping the Faith,” one of the key aspects of value as a selection technique is that lagged value works every bit as well as – and sometimes better than – today’s value. As a result, when putting together our portfolios we react not just to today’s forecast but to the average of the forecasts over the last year. And on this basis, emerging value has done something fairly remarkable. Emerging value today is not the cheapest we have ever seen it; not only was it cheaper at the beginning of the year and at some points in 2016, but it was significantly cheaper than today in both the financial crisis and the 2002-03 period. Actually, in February 2009, almost every single risky asset class we had a forecast for had a higher forecast than emerging value does today!2 But, on a measure that really matters to us for portfolio construction, emerging value today is the best asset we have ever seen. That measure is its “margin of superiority” – the amount by which it is better than the next best asset on our forecasts.3

As you can see, much of the time our favorite asset is only a little better than the next best. On those occasions, the cost of diversifying from our favorite asset is fairly low and the benefits of diversification tend to dominate. Of course, we should own plenty of our favorite asset, but not necessarily a lot more than we own of the next best. Today, emerging value is a lot better than anything else, so the drop-off in expected return going from it to the next best asset is severe. How much of it should we hold? That answer, in the end, must come down to risk.

The risk of emerging

There is little question that emerging market value is not only a risky asset, but probably the riskiest of the risky assets we routinely buy in our portfolios. We should expect worse performance from them in the event of a global economic crisis than even other types of equities. Furthermore, emerging economies are subject to home-grown crises, and in periods like 1997-98 or 2014-16 have shown themselves capable of substantial losses even when other risky assets are doing well or at least a lot less badly.

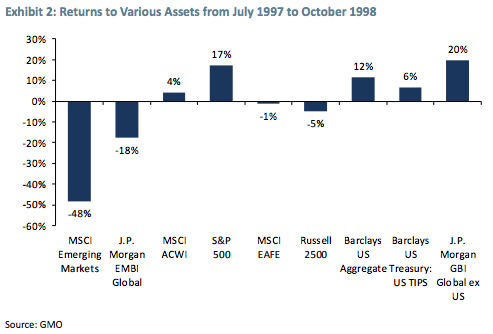

But depending on your definition of risk, 1997-98 was either a big problem or a small one. Let’s first think in terms of running an equity portfolio against an MSCI ACWI benchmark.4 If your view of risk as a portfolio manager is underperforming ACWI, the worst thing that ever happened to emerging was the period from the summer of 1997 to the fall of 1998. In that period, ACWI rose by 4% and MSCI Emerging fell by 48%. It’s a stunningly bad event in relative terms.5 If that didn’t cause equity managers to recognize the risk of betting on emerging, I don’t know what it would take! You could say that it was just as bad in absolute terms, and in a sense that is true. A 48% absolute loss is a big deal in anybody’s book. But given that it was basically an emerging-specific problem, the loss was unlikely to lead to a big drawdown in your overall portfolio. Exhibit 2 shows the returns to various assets during the time period of emerging’s disaster.

Other than emerging equity and debt, this was a pretty decent time to be an investor. When one thinks about the real risks for a long-term investor, the risks that really matter are events that cause sufficiently acute losses across the portfolio to require a behavior change in spending, or events that cause losses that are not reversed even in the long term. The 1997-98 loss, as bad as it was for emerging, has not meant any permanent loss for emerging market investors. Since the start of 1997, MSCI emerging has mildly outperformed ACWI, even including that large drawdown. As for emerging debt, the other material loser in the period, since 1997 it has been the best performing of all of the asset classes we track, despite its losses in 1997-98. Emerging equities and debt are volatile assets and move somewhat to an “emerging” rhythm. This means that the potential for them to underperform other assets is quite material, but so is their ability to beat them. In other words, for an investor more concerned with absolute risk and return than relative, they can offer valuable diversification.

But let’s not kid ourselves. Emerging is also a risky asset that can be relied upon to perform poorly in events that really do matter. From the 2007 high for ACWI to the 2009 low, ACWI lost 55%. MSCI Emerging lost 62%. This may not sound like a big difference, but in order to recover the losses, ACWI had to rally 122%, whereas MSCI Emerging needed to rally 160%, a difference of 38 percentage points.

So for an investor focused on absolute return and risk, emerging is a risky asset class – let’s say a factor of 1.2 on platonic “equity depression risk,” although that is only an educated guess. But the fact that it is also capable of large losses at times when other assets do just fine is not necessarily such an issue. Even on the “Hell” version of our forecasts, where returns to all equities are higher, emerging market value stocks have an expected real return about 2.4 times higher than the next best equity group. On the “Purgatory” version, the ratio is 5.4 times.6 A return multiple of over 2.0 and a risk multiple of 1.2 argues for owning emerging equities to the exclusion of all other equities.

Why not go all the way to that, with perhaps 50% of our portfolio in emerging equities and no other risky assets? This portfolio would have similar “depression risk” to a standard 60% stock/40% bond portfolio and a hugely higher return on our forecasts – about 5% better than the traditional portfolio for the next 7 years. One reason not to do this is that this takes the “emerging-specific problem” event and turns it into a really meaningfully nasty event for the portfolio. If there were another -48% return from emerging such as we saw in 1997-98, we wouldn’t be bailed out by the performance of other assets in the way a diversified portfolio would be. Even if emerging came back as it did after that crisis, a 25% overall portfolio loss is a big loss. And just as important, given the fact that the large loss would come from a single volatile asset class, I’m also willing to bet that it would be a large enough loss to cause pretty much any investor (including GMO) to think twice about rebalancing into the pain, which is generally the right thing to do in such events. So let’s agree that 50% is too large a position. What is the right size? Given the size of the expected return premium for emerging value over everything else, it’s not really driven by the expected return gap but by risk.

The risk of emerging today

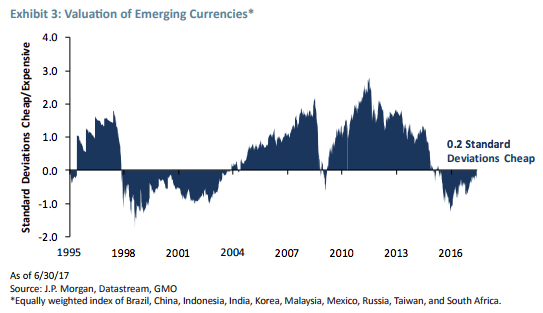

What can we think about the risk of emerging today versus points in the past? Certain things are clear. If the causes of previous crises in emerging have generally been currency or credit blow-ups, we are in better shape than we have been in the run-up to previous crises. Exhibit 3 shows the valuation of a basket of EM currencies over time.

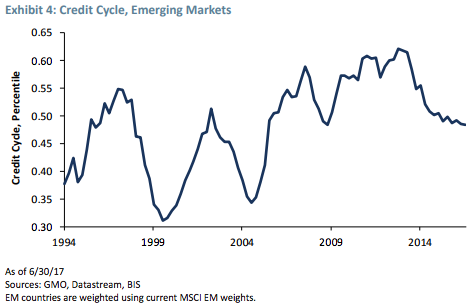

You can see that in the run-up to 1997-98, 2008-09, and 2011-15, emerging currencies were quite overvalued. In all of those cases, currencies got to at least 1.5 standard deviations overvalued. Today, even given a recovery from the 2015 lows, they are mildly cheap on our forecasts. A currency crisis therefore seems an unlikely driver of emerging problems. On the credit side of things we are likewise not in an obvious danger zone, as can be seen in Exhibit 4.

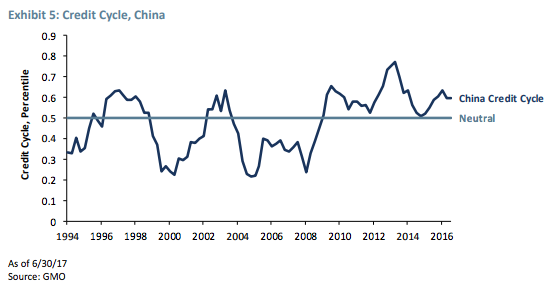

The current score on the credit cycle is 0.48, where 0.5 is neutral, and it has been coming down gradually over the last few quarters. Previous emerging crises saw this model top out between 0.55 and 0.65 before the crisis hit. Emerging is not a monolithic group when it comes to credit, and the most notable “hot” country is China, which is well above neutral. Exhibit 5 shows the cycle for China in particular.

On this model, the credit cycle has come down from the recent peak but is still at an elevated level. This argues to us that the risk of broad contagion in emerging from a credit event in China is not horribly high, but we need to be aware of the risk of credit problems coming from China. An elevated credit cycle is by no means a guarantee of a credit crisis, but it certainly creates the conditions for a crisis to take hold.

Given this data, it does not seem as if a 1997-98 currency crisis repeat is a high likelihood, but a creditdriven problem in the most important emerging economy is a meaningful possibility. And given the absolute valuations in emerging, losses in a bad event for emerging could be quite painful. We believe a worst case scenario is lower probability than normal, but by no means off the table.

Cromwell risk and the 30% solution

Given that the margin of superiority for emerging value is extremely high and the risk seems slightly less than normal, it is clear we should own a lot of emerging, but not necessarily what “a lot” should be. I’d love to tell you we have a scientific method of determining the ideal weight and we are completely confident we are at that weight, but that simply isn’t true. Given the state of the credit cycle and the absolute valuation of emerging, we want to be at a weight that is less than our true maximum. But how much lower an expected return every other asset has than emerging value, the maximum emerging weight for emerging value should be higher than it is when emerging market equities are only mildly cheaper than other assets. This is where another, harder to quantify risk comes into play. I don’t have a perfect term for it, but let’s call it “Cromwell risk.” Oliver Cromwell, in a letter to the Church of Scotland in 1650 wrote, “I beseech you, in the bowels of Christ, think it possible that you may be mistaken.”7 We are believers in value. We believe that cheap asset classes will outperform expensive ones in the long run. Historically, the evidence is in our favor, but that does not mean that every cheap asset does well. Value can be wrong. On the individual stock side, “value traps” – optically cheap companies whose fundamentals wind up deteriorating so fast that the cheapness turns out to have been an illusion – abound. On the asset class side, the odds are better, but still not 100%. On our data, emerging valueis the cheapest asset around today. Despite the fact that we know it can take large losses, our belief is that its volatility will not impact its longer-term performance. But there exists some risk that even though cheap assets normally do well, emerging value is, this time, a value trap. A compelling reason to diversify our multi-asset portfolios is that we are more confident that a portfolio of several different cheap-looking assets will outperform than that the single cheapest-looking one will. We need to trade off Cromwell risk – which always argues for diversification – against the expected opportunity cost of the diversification. In this case, we increased the maximum weight we’d contemplate having in emerging from 25% to 30% for our Benchmark-Free Allocation Strategy and made similar shifts in other asset allocation strategies with benchmarks. The high cost of diversification argues for a higher maximum emerging weight than we would otherwise be willing to live with. Given the state of the credit cycle and the absolute valuation of emerging, we want to be about 80% of the way through the range today, which gives us room to buy more if we do get an emerging, or global, crisis.

This shift in the maximum weight for emerging led us to buy a few percent more emerging value in July, despite emerging’s strong performance this year. Because an equity portfolio with more emerging has a meaningfully higher expected return, the money for this came from a combination of lower expected return equities (US high quality stocks) and non-equities, increasing our total equity weight at the margin.8 Is this a profound change to the stance of our portfolios? No. We still have materially less “depression risk” than a standard portfolio, given our low weight in equities overall. Emerging value was, by a large margin, the most important risk exposure in our portfolio. Now it is a little more so. Looked at this way, it seems mostly business as usual. But today isn’t a usual time. Normally when we buy more of an asset it is because we are moving farther through the range toward its maximum weight. This time it wasn’t so much the percent of the way through the range that changed, but the range itself.

1 The apparent 1% gap in returns (10% return less 3% value increase = 6% more expensive) is because of inflation over the period.

2 The only exceptions were low quality stocks, with an expected return of 4.7%, and emerging debt at 5.7% real. 3 In calculating

3 In calculating margin of superiority, we are excluding close-cousin assets that do not provide much diversification in the portfolio. For example, currently the second best asset forecast after emerging value is the overall emerging equity asset class, which is “only” 2.9% worse than emerging value on this basis. But diversifying from emerging value by buying broad emerging as well doesn’t make sense. The major risk (EM risk) is the same, so the risk benefit of diversification is far smaller than the cost of giving up the extra return of the value stocks.

4 ACWI is short for MSCI All Country World index and is a market capitalization weighted index of stocks around the world. 5 Specifically, this is the return from the end of July 1997 to the end of October 1998.

5 Specifically, this is the return from the end of July 1997 to the end of October 1998.

6 As a reminder, the “Purgatory” version of our asset class forecasts assumes that equity valuations revert to around 16 times normalized earnings over 7 years. The “Hell” version assumes we will revert to a normal P/E of around 20 times earnings. Given that higher equilibrium level, expected returns over the next 7 years would be higher for all equity groups in “Hell” than in “Purgatory.” The flip side, however, is that the very long-term returns to all assets are lower in “Hell” given the higher average valuations.

7 Oliver Cromwell is an interesting figure to be associated with a statement that can be so easily read as referring to essential limits of knowledge, as he does not seem to have suffered from much personal doubt in his correctness, either as a political and military leader or from a religious perspective. But let’s not let a little potential hypocrisy stand in the way of one of the great quotes of history.

8 This is, of course, only true for our multi-asset portfolios. Equity-only asset allocation portfolios funded all emerging buys out of other equities.

Ben Inker. Mr. Inker is head of GMO’s Asset Allocation team and a member of the GMO Board of Directors. He joined GMO in 1992 following the completion of his B.A. in Economics from Yale University. In his years at GMO, Mr. Inker has served as an analyst for the Quantitative Equity and Asset Allocation teams, as a portfolio manager of several equity and asset allocation portfolios, as co-head of International Quantitative Equities, and as CIO of Quantitative Developed Equities. He is a CFA charterholder.

Disclaimer: The views expressed are the views of Ben Inker through the period ending August 2017, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2017 by GMO LLC. All rights reserved.

Why Are Stock Market Prices So High?

(The market has always loved variables that make it feel comfortable and it has them now.*)

Jeremy Grantham

With an unexpected contribution from Ben Graham

Summary

■ Contrary to theory, the market P/E level does not primarily reflect future prospects. It reflects current conditions.

■ The variables it weights heavily are not academically or economically correct, but those that make investors feel comfortable.

■ High profit margins and stable, low inflation dominate this feel-good list, with stability of GDP growth (as opposed to actual growth) a distant third.

■ Investors’ extreme preference for comfort, like human nature, has never changed. (Tested back to 1925.) This is unlike financial and economic conditions, which have very substantially changed in the last 20 years.

■ The ebb and flow of these variables explain previous market peaks and troughs. These comfort factors, for example, have been at an extremely high average level for 20 years (as have P/Es) and remain so today. Thus today’s high priced market is the completely usual response from investors.

■ Any shift back to a lower P/E regime must therefore be accompanied by a major sustained fall in margins or a sustained rise in inflation (or both).

■ And, yes, I do believe these comfort variables will move to be less favorable. But probably not quickly

* My PhD thesis title would have been, “The Persistent Dominance of Superficially Appealing But Economically Inappropriate Market Influences.”

Introduction

In an investing and economic world in which almost everything seems to have changed in the last 20 years, one thing has remained constant: human nature. And, we can more or less prove it. At least in the case of the stock market.

The behavioral drivers of P/E ratios

Ben Inker and I designed a simple model 15 years ago to explain the shifts in P/E levels of the S&P 500. Recently we updated it. Our model does not attempt to justify the P/E levels as logical or deserved, nor does it attempt to predict future prices. It just shows what has tended to be the market’s typical response over the years to major market factors. By far, the two most important of these are profit margins, the higher the better, and inflation, where stable and lower is better, except not too low.

The market’s responses are typically quite different from what one might expect from an efficient market. Let us start with profit margins. In a rational world, stocks should sell at replacement cost. And therefore, above-average margins require a below-average P/E. An alternative way of viewing this is that above-average margins can be expected to mean revert – to move back to average – and vice versa. In real life, though, even in the past when margins were provably very mean-reverting, the market has always preferred high margins. Investors would dependably pay up for high margins, which would then decline, whacking them on the way down. Subsequently, investors would avoid markets with low average margins, which would then recover, causing them to underperform. Over and over again. This, in short, was primitive double counting. In 1974 or 1982, for example, at cosmic market lows, very, very depressed margins would sell at equally depressed P/Es of 6x or 8x, producing a price to book (or Tobin’s Q) of one-quarter or one-third. Conversely, at market peaks like 2000, record margins were multiplied by record P/Es, producing 3x price to book. This double counting is a major market inefficiency, perhaps the major inefficiency, and the main reason why market volatility is many multiples of the stately moves in the theoretical future value of dividends. To sell at fair value – true replacement cost – profit margins must be negatively correlated with P/Es, yet in the real world they are strongly positively correlated. And always have been.

Then there’s inflation, which the market hates despite a history of stocks proving that their fundamentals are robust in the longer term in passing inflation through to consumers. Stocks, unlike bonds, are clearly real assets, so inflation should not matter. But in real life, when inflation first appears or accelerates, there is an immediate, coincident negative effect on P/E multiples. (Modigliani, one of the very few economists who seemed to understand how inefficient the market was capable of being, visited a Boston brokerage house in the depths of 1974, when the market was 7x, and made this point eloquently over lunch. He explained that because inflation was irrelevant to long-term value, the market should always be at replacement cost, or twice the then price. Which it obediently moved to in the following two years. Not a bad call. Unfortunately, he seemed to be uninterested in doing serious academic work on the stock market. Had he done so, the belief in market efficiency might have been less of an expensive and dangerous proposition for society. Counting on rational behavior – or even reasonable behavior – from an investment world that overresponds to inflation and can’t even get the sign right for the effect of profit margins can be expensively misleading. As Kindleberger said, this kind of faith in market efficiency “ignores a condition for the sake of a theory.”)

A third behavioral factor, which we first modeled 16 years ago and still has explanatory power, although much less than the first two, is the volatility of GDP growth. Notice that this is absolutely not the growth rate of GDP. I have spent a few decades with traditional portfolio managers and I can guarantee that they are made nervous by rapid GDP changes, even on the upside. Changes make them fear more bumps in the road than normal. Rather, they love stable GDP growth, with few surprises, where they can feel more in control of their own predictions. And in such a world P/Es tend to be higher when GDP growth is stable, not when it is high. (By a strange coincidence, on June 28 the Wall Street Journal presented a chart showing global GDP volatility that has this very last month as the lowest in their 44 years of data!)

During the updating last year of our behavioral P/E model, we added two new factors, which we believe provide a little further value. The first addition was an on-off switch, which causes P/Es to be a bit lower after a down quarter. Again, not a very scientific reflex in a mean-reverting world, but understandable. The second was to add the US 10-year bond rate, where higher rates are negative, modestly improving the model even after the inflation component had done the heavy lifting for nominal interest rates.

Exhibit 2 shows our original model from 1925 through 2006 compared to actual Shiller P/E (current price over trailing 10-year average earnings). The overall fit is pretty good, but it is much better than that at extremes. In the past, the model explained a record high P/E in 1929, extreme lows in the 1930s, another high in 1965, extreme lows in 1974 and 1982, and a world record high, by a wide margin, in 2000. The outlier nature of the market peak in 2000 – confirmed in our updated version – suggests something interesting: Market peaks (1929, 1972, 1987, and 2008) and market troughs (1932, 1974, 1982, 2002, and 2009) were more or less – and more rather than less – what you should have expected from investors pressured with the comfortable (and uncomfortable) news at the time, as reflected in our model. For those events, you don’t need any further bubble or bust explanations. They were normal behavioral responses to extreme data. This behavioral model seems, in that sense, like a parallel universe to all our other investment thinking on bubbles. Only 2000 stands out, fully one-third higher than “explained,” as a genuine bubble, beyond these normal factors. The reader can surely pity investors who were hung out to dry in that extra and extraordinary one-third! Even the memory still stings.

We might reasonably conclude from this finding that any large and more or less permanent decline in the market (i.e., to a new, lower trend, much more like the 1945 to 1995 period than today) would require an equally large deterioration in profit margins or increase in inflation or some combination. Without either, any large market decline would be very unusual historically and likely, I believe, to be temporary. I can conclude this point by offering my personal opinion for 2017 on the two most important factors: favorable for margins and unfavorable for inflation. If only life were easy! But, even if these guesses prove to be correct, this mixed signal does not suggest a major decline or perhaps any decline.

For the record, if you need yet another rebuttal of the Lucas/Fama and French model of economic efficiency on the part of investors, this model is it: a long-term testimonial, and a very stable one, to investor behavior that they would have to describe as inefficient by their definition. And though this investor behavior may be loosely described as rational, it is certainly economically and financially innumerate. I am happy to say that I never believed a word of their theory on the efficiency of the market, which I have always thought is better described as a behavioral jungle. But having said that, I must admit to having detracted from my usefulness as an investor by assuming that investors overall would at least respond sensibly most of the time to the data they are given. And they do not. The effectiveness and persistency of our behavioral model, almost all the components of which should not work in a resolutely sensible world, let alone an efficient one, should have persuaded me to change my thinking years ago. But, here I am, trying to explain during these last nine months or so why the general discount rate of assets has dropped by roughly two percentage points from the 1900 to 1997 average. My proposed reasons for the reduced discount rate come down to a complicated stew of factors, most of which interact with the others: higher profit margins; higher leverage; lower rates; aggressive Fed and central bank policies to push rates lower; moral hazard from the Fed that may be more important than rates – the asymmetry of helping in bad times and letting good times run; changes in the age profile of the developed world; slower population growth; lower productivity; lower GDP growth; less low-hanging technological fruit; loss of the old $16 a barrel oil; extreme income inequality; remarkable lack of progress in median and lower hourly wages; and very much enhanced corporate political and monopoly power. Phew! I truly believe we will never know for sure which factors dominate the equation, although my favorite is Fed policy and the runners-up are an aging population profile and the rising political and monopoly power of corporations. But whichever they were, they got the job done: For the last 20 years profits in the US as a share of GDP and corporate revenues rose by about 30% and P/E ratios by 70% above the old normal.

Now, cutting across that previous attempt to understand these major changes in our new 20-year era, comes an entirely behavioral approach. Whether sensibly or not, investors love high margins and like stable growth even if it’s modest, and hate inflation. They felt this way from 1925 to 1997 and they felt exactly the same way in our new era of 1997 to 2017. So, behaviorally it is absolutely not a new era. It is precisely – to a 0.90 correlation – the same ole same ole. The peaks of 1929 and 1965 delivered favorable margins and inflation inputs but for a very short while in both cases. In contrast, the period of 1997 to 2017 has delivered to investors their preferred conditions almost the entire time, with only two very quick time-outs for market breaks. Can the market really be this easy to explain? Well, it has been for 92 years! And what can we investors do with this information? It tells us that if we re-enter a period of old normal profits and old normal inflation, the market’s P/E will indeed mean revert to its old average. And if we don’t re-enter such a period, the P/Es are likely to stay high. It tells us separately that if we expect a market crash, we should also expect to have a crash in margins (as we did in 2008-09) or a truly dramatic rise in sustained inflation (as we did in 1979-81) or some powerful combination. All of which is possible of course, but I think improbable, at least in the near term. This behavioral approach to explaining shifts in P/Es is certainly a much simpler equation than my previous stew-of-factors approach. But it does have some powerful similarities to my earlier arguments found in Parts 1 and 2 of “Not With A Bang But A Whimper.1 In both approaches, the role of profit margins is dominant. Improved margins not only move the earnings up directly, but also the P/E multiplier applied to those earnings. Inflation is also a strong secondary factor in both approaches, for low inflation, of course, drives down the interest rates, which appear to be an important ingredient in the stew.

So, where does this leave us? It suggests to me that I have in general been over-intellectualizing the working of the market for a few decades. I have had too strong a belief that investors would at least be influenced by past data in a sensible way. The market, however, appears not to care at all about the past or to learn much from it. This model for sure seems to say that for 92 years, at least, the market has with remarkable consistency been a coincident indicator of superficially appealing variables that in a strict economic sense have been inappropriate, and that have caused spectacular and unnecessary market volatility. The model is apparently a reflection of human nature and, of all factors influencing the market, human nature, as economically inefficient and unsophisticated it may be, seems the least likely to change.

Postscript #1: momentum and value

If the short-term behavioral variables described above dominate the short-term market level to the degree shown – a 0.90 correlation – what is the role for both momentum and value? My guess is that there is enough noise in the data for there to be room for many individual stocks to be driven in the short and intermediate term away from fair value by momentum, also a behavioral factor. More importantly for us value managers, I believe there is also enough noise in the data for individual stocks and the market to be pulled back toward replacement cost or fair value. Value (like gravity in physics) is a weak force in the short term, but very, very persistent so it can eventually work its way around the stronger coincident behavioral forces. Value was the beneficiary, after all, of a real world arbitrage: If the market priced a stock too high, management would sell stock and buy more – say, fiber optic cable – until market forces brought the price of the product, the profit margins, and the stock price down. If priced too low, management would buy stock back and reduce the underpricing and, more directly, it would withhold expansion until shortages occurred, sometimes quickly and sometimes drawn out. But more recently, increased monopoly power and other factors appear to have decreased the corporate reflex to expand in favor of stock buybacks, perhaps weakening the previously reliable game. But that of course is the question under consideration.

Postscript #2: a paean to changing your mind when the facts change

Descending out of the blue just before the July 4 weekend came this no doubt heaven-sent recently discovered talk by Ben Graham titled “Securities In An Insecure World,” which was given on November 15, 1963. It is one of the last he gave. After a 40-year career in which he had developed a fairly highconfidence view on how to define the value of the US stock market, he was having second thoughts. Like some of us now. Here are my favorite snippets.

“In early 1955 when I testified before the Fulbright Committee the stock market was then about 400, my central value was also around 400 and the valuation of other ‘experts’ using other methods all seemed to come to about that level. The action of the stock market since then would appear to demonstrate that these methods of valuations are ultra-conservative and much too low, although they did work out extremely well through the stock market fluctuations from 1871 to about 1954, which is an exceptionally long period of time for a test. Unfortunately in this kind of work, where you are trying to determine relationships based upon past behavior, the almost invariable experience is that by the time you have had a long enough period to give you sufficient confidence in your form of measurement just then new conditions supersede and the measurement is no longer dependable for the future.” [Emphasis added. By the way, the deliberate total return from the S&P 500 from the end of 1963 until today has been 5.75% real, exactly what we at GMO assume to be the long-term, normal return.]

“My reason for thinking that we shall have these wide fluctuations – of which we had a taste in 1962, in May particularly – is that I don’t see any change in human nature vis-à-vis the stock market which is sufficient to establish more restraints in the public behavior than it showed over so many decades in the past.”

“But let me point out ‘for the record’ that it is not impossible in theory that the market’s high level alone could sooner or later precipitate a collapse without the necessity for these technical weaknesses [described above, Ed.] to show themselves. The collapse might be triggered by some untoward economic or political development. But if things do happen that way it will be the first time in market history, I believe, that we would have the end of a bull market without the excesses and abuses of the sort I have mentioned.” [Emphasis added.]

“The main need here is for the investor to select some rule which seems to be suitable for his point of view, one which will keep him out of mischief, and one, I insist, which will always maintain some interest in common stocks regardless of how high the market level goes. For if you had followed one of these older formulas which took you out of common stocks entirely at some level of the market, your disappointment would have been so great because of the ensuing advance as probably to ruin you from the standpoint of intelligent investing for the rest of your life.”

1 Jeremy Grantham, “Not With A Bang But A Whimper,” GMO 3Q 2016 Quarterly Letter and “This Time Seems Very Different,” (Part 2, Not With A Bang But A Whimper,” GMO 1Q 2017 Quarterly Letter. Both of these pieces are available at www.gmo.com.

Jeremy Grantham. Mr. Grantham co-founded GMO in 1977 and is a member of GMO’s Asset Allocation team, serving as the firm’s chief investment strategist. Prior to GMO’s founding, Mr. Grantham was co-founder of Batterymarch Financial Management in 1969 where he recommended commercial indexing in 1971, one of several claims to being first. He began his investment career as an economist with Royal Dutch Shell. He is a member of the GMO Board of Directors and has also served on the investment boards of several non-profit organizations. He earned his undergraduate degree from the University of Sheffield (U.K.) and an MBA from Harvard Business School.

Disclaimer: The views expressed are the views of Jeremy Grantham through the period ending August 2017, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2017 by GMO LLC. All rights reserved.

© GMO

Read more commentaries by GMO