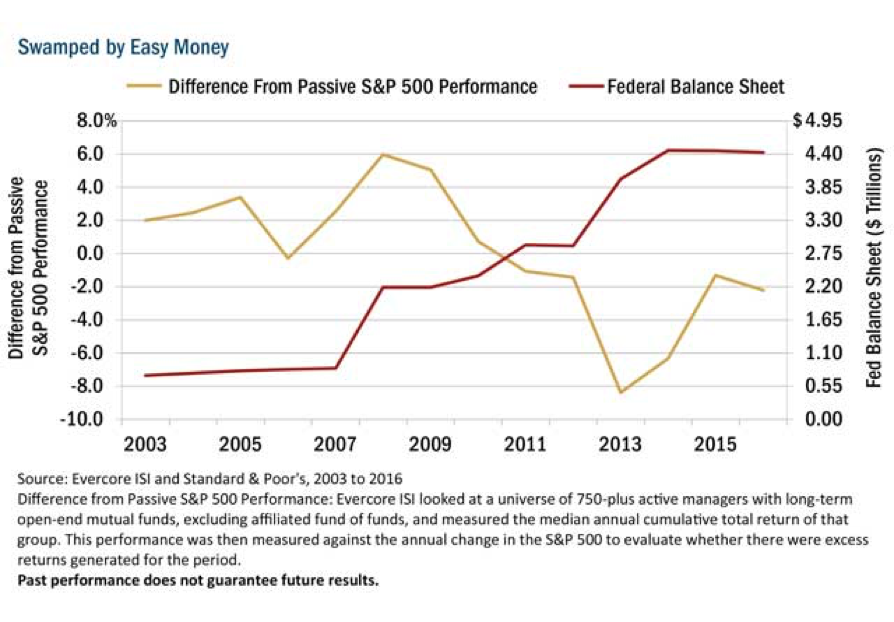

When talking with clients these days, passive versus active management is the red-hot topic. Many point to underperformance by active managers in the past few years as proof that the days of the stock picker are numbered. What strikes me during these conversations is that so many investors take it as a foregone conclusion that index funds will continue to outperform regardless of the backdrop. But is that true? Based on this chart, the case could be made that the fate of passive investing’s performance is tied to how the Federal Reserve Board acts going forward.

As shown, the average active manager was handily beating the S&P 500 Index prior to the Fed unleashing the power of Quantitative Easing. As the central bank’s balance sheet ballooned, so too did returns of the broad Index against fundamental portfolio managers.

Intuitively, it makes sense. Excessive liquidity and low interest rates can paper over a lot of flaws at the company level. With businesses receiving little or no penalty for poor capital management or unhealthy debt, investors have been free to outsource investment decisions to index providers and turn their attention elsewhere.

Now that rates are rising and the Fed has signaled a commitment to shrinking its balance sheet—and, consequently, reducing the liquidity sloshing around the financial system—we think it is prudent for investors to reconsider their assumptions. As the old adage goes, past performance does not guarantee future results.

Disclosure:

Past performance does not guarantee future results.

Investing involves risk, including the potential loss of principal. There is no guarantee that a particular investment strategy will be successful. Value investments are subject to the risk that their intrinsic values may not be recognized by the broad market.

The statements and opinions expressed in this article are those of the presenter(s). Any discussion of investments and investment strategies represents the presenter’s views as of the date created and are subject to change without notice. The opinions expressed are for general information only and are not intended to provide specific advice or recommendations for any individual. Any forecasts may not prove to be true.

Economic predictions are based on estimates and are subject to change.

Definitions: Active Management: the use of a human element, such as a single manager, co-managers or a team of managers, to actively manage a fund's portfolio. Active managers rely on analytical research, forecasts, and their own judgment and experience in making investment decisions on what securities to buy, hold and sell. Passive Management: a style of management associated with mutual and exchange-traded funds (ETF) where a fund's portfolio mirrors a market index. Quantitative Easing: is a government monetary policy occasionally used to increase the money supply by buying government securities or other securities from the market. S&P 500 Index: is an index of 500 U.S. stocks chosen for market size, liquidity and industry group representation and is a widely used U.S. equity benchmark. All indices are unmanaged. It is not possible to invest directly in an index.

©2017 Heartland Advisors heartlandadvisors.com

2017232