During the first half of 2017, gold bullion rose 7.75% while the XAU (Philadelphia Index of Gold and Silver Stocks) rose 2.79% (including dividends). Among the notable developments of the first half were the pronounced weakness of the trade-weighted US Dollar (down 6.44%) and the continuing sluggishness of the US economy, both of which call into question the wisdom, feasibility, and credibility of the Fed’s push to tighten credit.

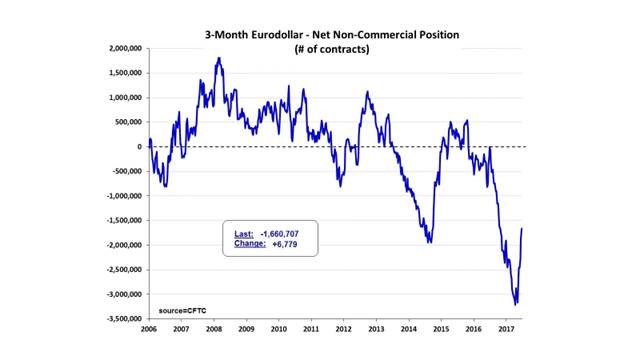

US dollar weakness was completely unexpected by the investment consensus, as reflected in record speculative euro shorts at year end (see chart below). The misreading of the currency outlook by numerous well-known and highly regarded investment thought leaders suggests to us that other important components of the macro and market outlook may have also been misjudged by both the investment consensus and policy makers.

We believe that the Fed’s view of economic activity is not rooted in reality (see Q1 commentary), and that its stubborn pursuit of interest-rate hikes is likely to precipitate a bear market in equities and bonds. Under the headline “Economic Conditions Signal Recession Risk,” Greg Ip wrote in the July 6 WSJ, “If you drew up a list of preconditions for a recession, it would include the following: a labor market at full strength, frothy asset prices, tightening central banks, and a pervasive sense of calm. In other words, it would look a lot like the present.”

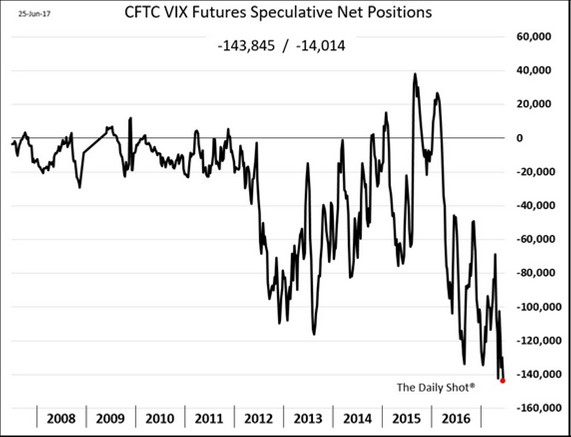

Because of strong financial markets, investor interest in gold remains subdued. In our opinion, revival of interest will be closely related to financial-market damage of sufficient magnitude to shake prevalent investor complacency, best reflected in persistent record-low readings in volatility (VIX index). A mean-reverting VIX would in our opinion cause the Fed to abandon any pretense of monetary tightening. An unexpected U-turn in monetary policy would almost certainly cause precious metals prices to surge.

Financial-market complacency seems (inexplicably, to us) to be based on confidence in a continuing economic expansion and a smooth transition (meaning pain-free in terms of market damage) to normalization of monetary policy and interest rates. We believe that these two expectations are incompatible and unattainable simultaneously. In fact, we believe that the likelihood of either occurring is miniscule.

At the spring 2017 Grant’s conference, Peter Fisher (former manager of the NY Fed System Open Market Account, and now senior lecturer at the Tuck School of Business at Dartmouth) stated, “It appears to me that the Fed and other central banks have avoided being candid about the uncertainty [of the transmission mechanism of monetary policy and the challenge of decision-making in conditions of uncertainty] in order to maintain their credibility.” He went on to say, “normalizing monetary policy will require that the Fed disown the idea that the level of wealth (i.e., financial-asset valuations) is an appropriate objective of monetary policy,” and further, that “forward guidance is the process through which the Fed – through its more explicit influence on the expected rate of interest – becomes the much more explicit owner of the ‘conventional valuation’ of asset prices.”

Stated another way, and in far less erudite terms, the Fed owns the stock market. The institution’s credibility has in our opinion become inseparable and indistinguishable from financial-market stability. This less-than-“candid” institution cannot afford a major downdraft in financial-asset values. It is caught in the lie that the institution’s supposedly superior and privileged knowledge hold the key to future prosperity, economic growth, and policy normalization. The price of an honest reassessment would risk calling into question the extreme policy measures undertaken since 2008.

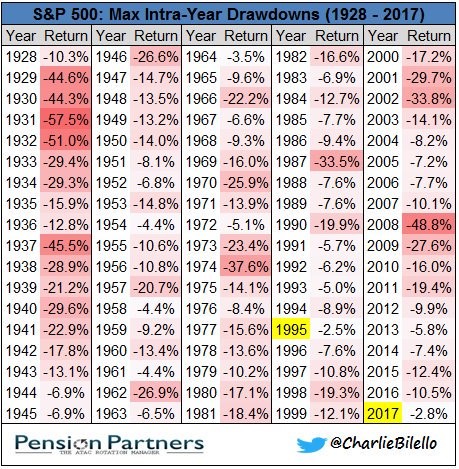

It is not farfetched, in our opinion, to suggest that the Fed and other central bankers, as Mario Draghi has famously stated, will “do whatever it takes” to maintain the illusion of wealth created by radical monetary measures, including market-rigging practices. The evidence in the table below suggests strongly that central-bank trading rooms have begun actively to defend key market support levels. The maximum drawdown for the S&P 500 in 2017 is the second lowest on record since 1928.

Investor confidence in financial-asset valuations appears to rest on the fragile premise of Fed protection. Should the credibility of that premise become untenable, vulnerability of asset values will most likely be accentuated by the following factors:

- Historically high valuations: Bonds trade at historic low yields. Without that tailwind, near-record-high equity valuations would be unsupportable. Michael O’Rourke, chief market strategist at Jones Trading, notes, “unweighted multiples (S&P 500) are higher today (44.5 times) than at their peak in 2000 (33.7 times) and 2007 (30.2 times).” We view the tightening cycle being pursued by the Fed and other central banks as an unambiguous threat to equity valuations.

- ETFs and index funds are reflexive: Inflows have led to indiscriminate buying and outflows will lead to indiscriminate selling. John Bogle, founder of Vanguard, has stated that 50% of trading is controlled by ETFs. The $3 trillion ETF industry has grown nearly tenfold over the past 10 years in terms of assets under management. In our view, the greatest danger of ETFs is the illusion of liquidity. The liquidity of these surrogates in many cases far exceeds the liquidity of the underlying securities and commodities that they represent. Capital inflows into ETFs over the past 10 years have driven equity valuations. Outflows will drive valuations down, fundamentals aside.

- VIX readings are at an extreme. Speculative shorts are at the highest level since 2008. Mean reversion seems inevitable.

- Rapidly expanding sovereign debt in the US and the rest of the world is a time bomb. It is widely dismissed as an investment issue, mainly because of interest-rate suppression by central banks. As famed market analyst Bob Farrell observed in his July 1, 2017, letter, “Debt excesses have proved to be the downfall of many bull markets… From a long-term perspective, our concern today is the record level of sovereign debt and the increasing levels of other government indebtedness… The discipline necessary to reduce it or prevent it from reaching crisis proportions continues to be absent… In a world replete with anomalies arising out of grand monetary experiments…unintended consequences are an increasing risk.”

We suspect that the Fed has already lost substantial credibility, but that investors prefer to look the other way as long as financial-asset values remain intact. It is, in our opinion, an “everybody knows the dice are loaded” situation that could portend an even sharper, impossible-to-escape downdraft once confidence is dislodged.

Rising interest rates and market stability have rarely, if ever, coexisted, even if those increases are generally anticipated. In a free market, the ever-increasing supply of sovereign debt would be met with rising yields. Because bond yields are manipulated, the rate of increase may be dampened somewhat by central-bank actions, but even the baby-step increases contemplated by the Fed would be sufficient to destabilize overvalued financial assets.

Should the Fed and other central banks fail to achieve the all-but-impossible task of returning to a normal yield curve without undermining financial-asset values, exposure to gold and related mining stocks represents a compelling investment proposition, if only as a hedge against increasing macro and market risks. Our investment strategy is to focus on mid- to smaller-cap companies that, through a combination of superior assets and sound management, add incremental per-share value through reserve and output additions independent of fluctuations in precious-metals prices.

Because the gold-mining industry has struggled to maintain reserve life (which stands at a 17-year low), we anticipate a wave of acquisition and consolidation activity over the next three to five years from which many of our holdings will benefit. Should the gold price provide a tailwind, we expect returns from our investments to be quite rewarding.

The macro and market events that we anticipate will almost surely drive large capital flows into the relatively tiny gold sector. Gold, held in proper form is the most liquid asset in the universe devoid of financial-market counterparty risk. No other non-financial asset – including real estate, fine art, or commodities – measures up as a potentially effective or accessible hedge against a market meltdown.

Gold, as we have noted in a previous letter, has been the top-performing asset class since 2000, the dawn of radical monetary experimentation. We believe that a hard look at the facts suggests that a return to the normality of the past is unattainable, and that the captains of economic policy are living in a dream world. In light of these considerations, investor disinterest in gold and the implied expression of trust in the sustainability of current economic arrangements bewilders us, especially when even small exposure to the metal would be the financial-asset analog of fire insurance on one’s home. We therefore recommend taking advantage of periodic pullbacks in the precious-metals sector to initiate or expand positions.

John Hathaway

Senior Portfolio Manager

© Tocqueville Asset Management L.P.

July 10, 2017

This article reflects the views of the author as of the date or dates cited and may change at any time. The information should not be construed as investment advice. No representation is made concerning the accuracy of cited data, nor is there any guarantee that any projection, forecast or opinion will be realized.

References to stocks, securities or investments should not be considered recommendations to buy or sell. Past performance is not a guide to future performance. Securities that are referenced may be held in portfolios managed by Tocqueville or by principals, employees and associates of Tocqueville, and such references should not be deemed as an understanding of any future position, buying or selling, that may be taken by Tocqueville. We will periodically reprint charts or quote extensively from articles published by other sources. When we do, we will provide appropriate source information. The quotes and material that we reproduce are selected because, in our view, they provide an interesting, provocative or enlightening perspective on current events. Their reproduction in no way implies that we endorse any part of the material or investment recommendations published on those sites.

Read more commentaries by Tocqueville Asset Management