A few years back there was a TV commercial for the Toyota Camry featuring the singer, Kelly Clarkson and ESPN’s legendary sportscaster, Chris Berman. It pointed out all the positive attributes of the “new” Camry with Kelly’s hit, “Stronger,” playing in the background. As we look out into the second half of 2017, it is important to understand that we believe the U.S. stock market has tried to “kill” investor enthusiasm. We would argue this enhances the position of the value-oriented and long-duration equity manager in a way that that doesn’t kill us and makes us “stronger.”

What is Killing Investor Enthusiasm?

We see some obvious factors that are killing investor enthusiasm. First, up to 50% of large-cap U.S. equity ownership comes through owning the S&P 500 Index. For the stock market in general, it is like having a favorite sports team and having no individual players you root for or keep track of. Maybe Vanguard will form fantasy stock market leagues, where index investors select a few stocks to follow and measure.

Second, the S&P 500 is heavily committed to the five largest tech stocks, and as a result, it is the most heavily over-weighted tech stocks it has been since 1999. This has multiple negative effects on investor enthusiasm. The success of the tech companies becomes myopic and usually appears to be a detriment to other S&P 500 companies. It narrows the number of successful stocks and it has the appearance of sucking all the stock market oxygen out of the room.

Third, the election of Donald Trump as President of the United States has ushered in an “in your face” era in politics. We had polarized politics in the Obama era, but now the power is held by exactly the opposite group of politicians and regulators. We would remind everyone how similar the lack of investor enthusiasm was in the first 18 months of Ronald Reagan’s Presidency (from January of 1981 to July of 1982).

Fourth, this is the most anemic economic recovery from a deep recession in my lifetime. Slow growth has caused investors to crave sales or profit growth the way women crave a view of Ryan Gosling’s washboard stomach. Without faster economic growth it is hard for main street businesses to gain investor enthusiasm.

Lastly, the stocks which have been successful rarely split their stock price to a level which is attractive to individual investors. It would be like selling ten baseball cards for $25 per pack. Even though you like baseball cards, you can’t afford the entry price. Most of today’s success stories trade for more than $100 per share, a level that would have triggered a stock split in prior eras.

How does this make us stronger?

We believe the lack of enthusiasm for stocks and today’s set of circumstances provides a blueprint to future profits in U.S. large-cap stocks. Bargains are available, especially among companies which are viewed to be damaged by tech stock hegemony. Our portfolio currently trades at one of the biggest discounts to the S&P 500 Index since inception 9.5 years ago. This fact guarantees nothing in the short run, but should bode well long term.

Maniacal activity in tech stocks is easy for us to avoid, even when it causes us to underperform. Warren Buffett says, “Excitement and expense is the enemy of your portfolio.” If anyone can prove that there is no excess excitement attached to tech stocks today, they are not watching the semiconductor stocks. Mania avoidance makes us stronger.

The lack of investor enthusiasm is forcing investors to be more patient and should play into the hands of “stronger” low turnover managers like us. Studies have shown that the turnover among U.S. large-cap equity managers is 62%, costing them about 0.84% of their returns annually. In comparison, we have averaged less than 20% turnover the last eight years.1 Buffett says, “The stock market was formed to move money from those who are impatient to those who are patient.”

The last thing which isn’t “killing” us and makes us “stronger” is the demographic set up for the next fifteen years. As you can see below, the number of 35 to 44-year-old Americans will explode during the next ten years. This bodes well for marriages/household formation, and a ramp up in the birthrate. Economic growth comes from more people and more productivity.

Today’s Circumstances

Numerous factors created by today’s circumstances make us “stronger.” Interest rates are historically low as seen in the chart below:

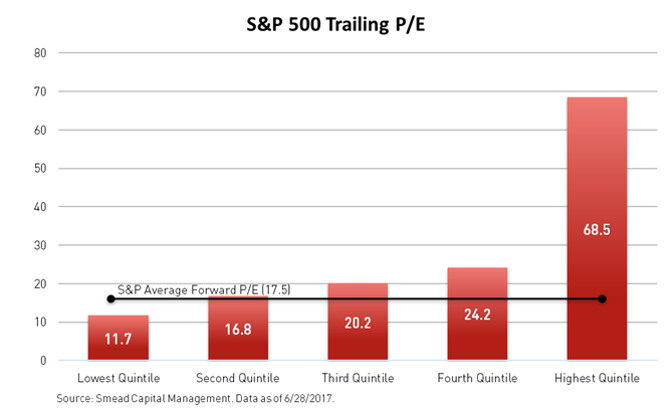

Stock prices in the S&P 500 Index are the most bifurcated since 1999 (see chart below) and set up a very positive 2000-2002 run for value investors.

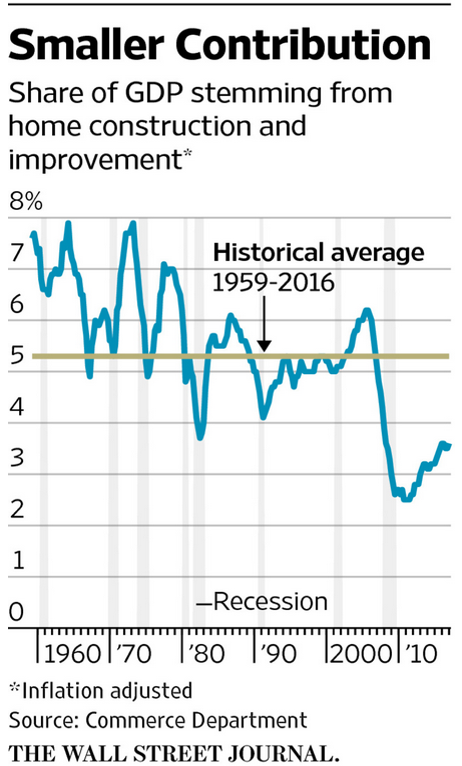

Housing should drive higher GDP growth as this chart shows:

Where are the Bargains?

The same forces that are killing enthusiasm for stocks have been especially detrimental to the prices of media companies, drug/biotech companies, and retail companies. The media companies like Disney (DIS), Tegna (TGNA), and Scripps Network (SNI) look particularly attractive. We also believe healthcare stocks like Amgen (AMGN) and Walgreens (WBA) live under the cloud of polarized politics.

In our view, homebuilders are held back by regulatory restrictions and some labor shortages. For the long-duration investor like us, NVR (NVR) and Lennar (LEN) look very good as the biggest economic need in our society (a lack of stand-alone homes) gets solved. The extrapolation of the death of retail driven by the success of Amazon has bolstered our interest in eBay (EBAY), Nordstrom (JWN), and Target (TGT).

If the pain of sitting through these years of low investor enthusiasm makes us “stronger,” we could be vindicated with multi-year rewards for patient long-duration investors. Thank you for your confidence and trust in our stock-picking discipline.

1Source: Financial Analyst Journal Jan/Feb 2016 “Shedding Light on “Invisible” Costs: Trading Costs and Mutual Fund Performance,” by Edelen, Richard Evans, and Gregory Kadlec.

© 2017 Smead Capital Management, Inc. All rights reserved.

This Missive and others are available at www.smeadcap.com

Follow us on Twitter @SmeadCap