MSCI to Add China A-Shares to Emerging Markets Index: What Does It Mean for Investors?

The decision brings better representation of the entire Chinese economy

The decision brings better representation of the entire Chinese economy

The decision brings better representation of the entire Chinese economy

The decision brings better representation of the entire Chinese economyAfter four years of discussions, on June 20, 2017, MSCI announced a ”yes” decision on including China A-shares in the MSCI Emerging Markets Index, which tracks $1.6 trillion1 worth of assets around the world, and related indexes.2 The decision is seminal because it provides previously unavailable A-share exposure in emerging markets (EMs) and global indexes. The initial weight of China A-shares in the MSCI Emerging Markets Index upon the August 2018 inclusion will be 0.73% (2.49 % in the MSCI China Index), comprising 222 onshore-listed stocks. The number of stocks is higher than the originally proposed 169 stocks in March’s consultation paper.

This change is not a surprise to us. My team has expected that China A-share inclusion could realistically happen this year, as both China and MSCI have been very supportive of the change. We welcome this decision as it marks another milestone in recognition of China’s gradual market liberalization efforts, further opening its domestic equity market to global investors. What pleasantly surprised us is the higher number of A-shares stocks to be added and the increased initial inclusion weight in the MSCI Emerging Markets Index (from 0.48% to 0.73%) and MSCI China Index (from 1.70% to 2.49%). In our view, the inclusion is a wake-up call for global investors to rethink their investment in China. It brings better representation of the entire Chinese economy and diversified exposure to the existing offshore Chinese equity universe.

What made it a “yes” for MSCI this time?

In our view, MSCI’s decision to include A-shares was the result of:

- MSCI’s assessment framework: The most significant change in the MSCI proposal this year was its consideration of the “Stock Connect” programs, rather than the Qualified Foreign Institutional Investor (QFII)/RMB Qualified Foreign Institutional Investor (RQFII) programs, as the Stock Connect programs offer increased foreign accessibility to Chinese markets, no overall aggregate quota and no capital mobility restrictions.3 This change in assessment framework is practical as the inclusion decision no longer rests on the unresolved issue of the 20% monthly repatriation limit under QFII/RQFII programs, which are becoming obsolete. International institutional investors generally welcomed the expansion of the Stock Connect program to include Shenzhen-listed stocks and viewed the program as a more flexible access framework.

- Reduced voluntary trading suspensions: Since the market turmoil in July 2015, Chinese regulators have tightened information disclosure requirements and reduced the length of suspensions. This resulted in a significant decrease in the number of suspended China A-shares – an encouraging development which international investors favor.

- Resolution on the pre-approval requirement issue: MSCI was able to reach a resolution with Chinese stock exchanges on loosening the pre-approval requirement for financial products linked to China A-shares. This addressed the last hurdle for inclusion.

Wake-up call for global investors

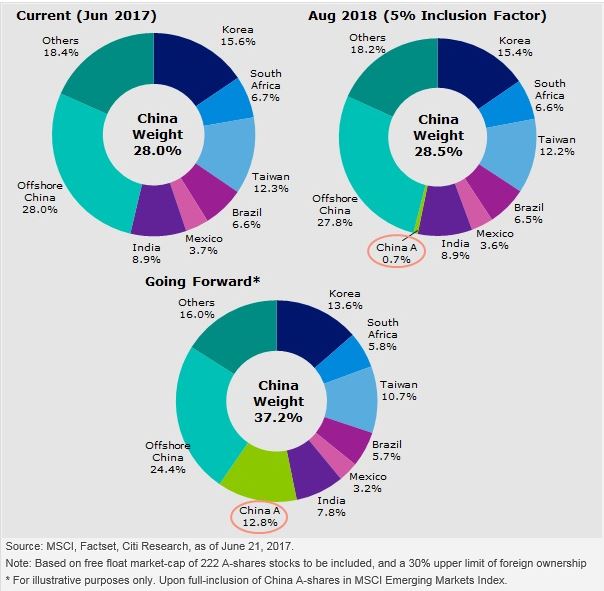

MSCI’s decision on A-share inclusion recognizes China’s increasing importance and validates China A-shares as “recognized” markets, offering adequate market access and investability. This is a structural change to the MSCI Emerging Markets Index and will be significant for years to come. Upon full inclusion, it is estimated that China (combined onshore and offshore) could comprise up to 37.2% of this index.4

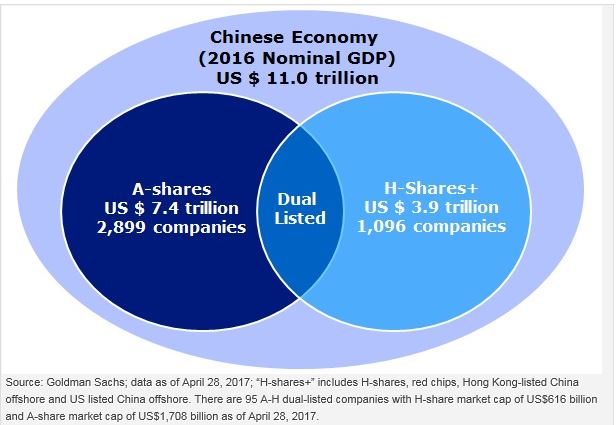

In our view, the inclusion is a wake-up call for global investors. We believe it is important for them to rethink their strategic allocation to China and realize that offshore Chinese equities alone do not represent the entire Chinese economy. In fact, as shown in the chart below, there is greater breadth and depth to the domestic onshore market, given that 2,899 companies are listed onshore, compared to 1,096 companies listed offshore (with 95 that are dual listed).

Offshore Chinese equities alone do not represent the entire Chinese economy

Closer to China’s real economy

We believe that upon full inclusion of A-shares, the MSCI China Index will offer investors a better representation of the underlying economy. A-shares also offer complementary exposure to existing offshore Chinese equities. Currently, the MSCI China Index provides good exposure in large overseas listings of Chinese banks and internet companies. The 222 A-share stocks are, on the other hand, closer to China’s real economy. The inclusion will bring the weights for industrials, health care, consumer staples, materials, information technology and telecommunications as well as energy closer to their respective GDP representation. At the same time, A-shares also contain many unique companies that are not abundant in the offshore space such as household furnishings, chemicals, renewable power producers, biotechnology and pharmaceutical companies.

MSCI China Index potential sector weight changes (before and after full inclusion)

Timing for full inclusion — a gradual process

MSCI’s recent announcement stated that A-share inclusion will use a two-step process, during May and August 2018 index rebalancing respectively, to account for the existing daily trading limits on Stock Connect. Although MSCI confirms A-share inclusion, they have left the full inclusion timeline open-ended. While it is difficult to predict the exact timeline of the full inclusion, we can use MSCI’s experience with South Korea and Taiwan in its Emerging Markets Index as a reference.

Both South Korea and Taiwan equity markets were included in the MSCI Emerging Markets Index gradually via multiple phases. It took six years (1992 to 1998) in the case of South Korea and five years (1996 to 2001) for Taiwan to be fully included. The pace of inclusions takes into account the limitations that could arise in the opening of equity markets to foreign investors, such as capital controls. Over the years, we have noticed the inclusion process corresponded with the regulatory effort to relax capital controls in both markets. For instance, MSCI decided to increase Taiwan’s weight in the index in 2000 (from 65% to 80% of its total market cap) when the investment ceiling for Taiwan’s Qualified Foreign Institutional Investors was increased.

So based on South Korea and Taiwan, we believe it would be unlikely for the full inclusion of China A-shares in the index to take place abruptly; instead, it would probably occur in gradual steps. But investors should be prepared for full inclusion that may not be far. Full inclusion is estimated to have a 12.8% weight in China A-shares, and a 37.2% weight in the MSCI Emerging Markets Index together with offshore China.

Country weights in MSCI Emerging Markets Index

Conclusion

With the ”yes” decision from MSCI on the inclusion of A-shares, global investors should realize that going forward, the index will provide a better representation of the Chinese economy and diversified exposure to the current offshore Chinese equity universe. Although the full inclusion will not be immediate, we believe it will not be far, based on previous MSCI experience with Taiwan and South Korea.

We believe market liberalization in China is a structural trend, as China is further opening its equity markets to global investors. The representation of Chinese equities will only get bigger in regional and global indexes. In our view, global investors should embrace this structural shift sooner than later to participate in both onshore and offshore Chinese equities.

Learn more about Invesco Greater China Fund.

1 Sources: MSCI, eVestment, Morningstar and Bloomberg as of Dec. 31, 2016 (latest available data), released by MSCI on April 21, 2017.

2 Because the MSCI Emerging Markets Index is part of the MSCI All Country World Index (ACWI), once A-shares are included in the EM index, they will also simultaneously be included in other regional and global MSCI indices, such as the MSCI All Country Asia Pacific ex-Japan Index.

3 Launched in November 2014, the Shanghai-Hong Kong Stock Connect is a securities trading and clearing links program that allows both global and domestic investors to make cross-border stock purchases between the Shanghai and Hong Kong stock markets.

Launched in December 2016, the Shenzhen-Hong Kong Stock Connect is a securities trading and clearing links program that allows both global and domestic investors to make cross-border stock purchases between the Shenzhen and Hong Kong stock markets.

The QFII (Qualified Foreign Institutional Investor) and RQFII (RMB Qualified Foreign Institutional Investor) schemes allow global investors to access China A-shares. However, these schemes are available only to institutional investors who can fulfill capital and asset size requirements. Detailed submissions and preapprovals are needed for the mentioned schemes.

4 Source: MSCI, Citi Strategy Research estimates, made on June 21, 2017

Mike Shiao

Chief Investment Officer, Asia ex Japan

Mike Shiao joined Invesco in 2002 and was promoted to Chief Investment Officer, Asia ex Japan, in 2015. With over 23 years of industry experience, he leads the Greater China equities team and focuses on the Greater China equity strategy, covering the Hong Kong, China, and Taiwan markets.

Previously, Mr. Shiao was head of equities for Invesco Taiwan Ltd. He started his investment career in 1992 at Grand Regent Investment Ltd., where he worked for six years as a project manager supervising venture capital investments in Taiwan and China. In 1997, he joined Overseas Credit and Securities Inc. as a senior analyst covering Taiwan technology sector. Mr. Shiao also worked at Taiwan International Investment Management Co., as a fund manager and was responsible for technology sector research.

Mr. Shiao holds a bachelor’s degree from National Chung Hsing University, Taiwan and a Master of Science degree in finance from Drexel University, Philadelphia.

Important information

Blog header image: TK Kurikawa/Shutterstock.com

The MSCI Emerging Markets Index is an unmanaged index considered representative of stocks of developing countries.

The MSCI China Index is an unmanaged index considered representative of Chinese stocks.

The MSCI All Country World Index is an unmanaged index considered representative of large- and mid-cap stocks across developed and emerging markets, excluding the US.

The MSCI All Country Asia Pacific ex-Japan Index is an unmanaged index considered representative of Pacific region stocks, excluding Japan.

An investment cannot be made in an index.

Domestic China A-shares are listed on the mainland in the Shanghai or Shenzhen Stock Exchanges which are not fully accessible to international investors. At present, global investors can invest in China A-shares via the QFII (Qualified Foreign Institutional Investor), the RQFII (Renminbi QFII) and the recently launched Shanghai-Hong Kong Connect programs.

H-shares represent companies incorporated in mainland China that are listed on the Hong Kong Stock Exchange or other foreign exchanges. H-shares are regulated by Chinese law, denominated in Hong Kong dollars and trade the same as other equities on the Hong Kong exchange. H-shares include companies from most major economic sectors, such as financials, industrials and utilities.

The risks of investing in securities of foreign issuers, including emerging markets, can include fluctuations in foreign currencies, political and economic instability, and foreign taxation issues.

Investments in companies located or operating in Greater China are subject to the following risks: nationalization, expropriation, or confiscation of property, difficulty in obtaining and/or enforcing judgments, alteration or discontinuation of economic reforms, military conflicts, and China’s dependency on the economies of other Asian countries, many of which are developing countries.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. Each entity is an indirect, wholly owned subsidiary of Invesco Ltd. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC, investment adviser. Invesco PowerShares Capital Management LLC (PowerShares) and Invesco Distributors, Inc., ETF distributor, are indirect, wholly owned subsidiaries of Invesco Ltd.

©2017 Invesco Ltd. All rights reserved.

MSCI to add China A-Shares to emerging markets index: What does it mean for investors? by Invesco