With soft housing data last week and higher interest rates expected, it is a good time to ask:

Is the housing rally over?

Last Week Recap

The big economic news last week was the Fed policy decision and guidance. Friday’s announcement of the Amazon purchase of Whole Foods grabbed the headlines. Attorney General Sessions’ Senate Testimony got the gavel-to-gavel treatment.

Our question from last week – a possible change in market leadership – did attract some discussion. Friday’s grocery news is still being digested, but the sector shifts were pronounced.

The Story in One Chart

I always start my personal review of the week by looking at this great chart from Doug Short via Jill Mislinski. Despite the mid-week Fed announcement, the result for the week was barely changed.

Doug has a special knack for pulling together all the relevant information. His charts save more than a thousand words! Read the entire post for several more charts providing long-term perspective, including the size and frequency of drawdowns.

Note to Readers

Thanks to all of those who offered suggestions for changes in WTWA and feedback on my first attempt. I am still working on many of the other suggestions.

I am off next weekend, but I will again try to post an abbreviated version including an indicator update.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

The economic news last week was mixed.

The Good

-

Jobless claims declined to 237K, maintaining the current record-low levels.

-

Forward earnings estimates are holding up. This may seem like faint praise, but those criticizing the use of analyst estimates point to excessive optimism and repeated cuts in forecasts. Brian Gilmartin tracks these estimates. He notes the comparative strength, but also warns about possible weakness in tech.

-

Chemical activity barometer “suggests continued growth through 2017.” See GEI for the full story.

-

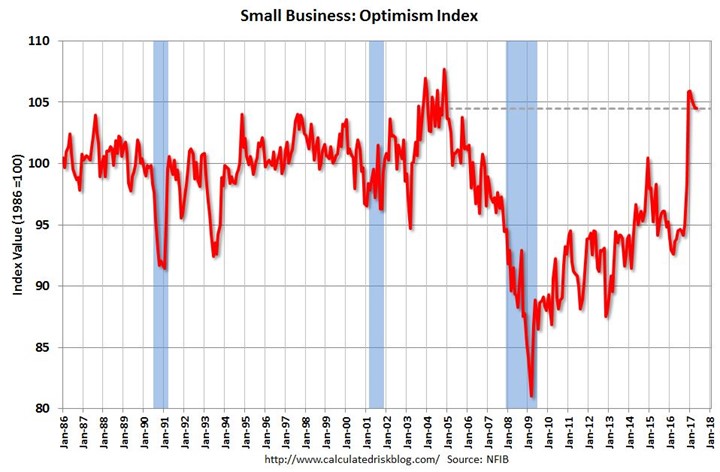

Small business optimism remains high. I have upgraded my attention to this series, since the importance has increased. Sluggish business investment, hiring, and loans to small companies have all been issues. Improved confidence from small business owners is helpful on all fronts. While some have (already?) become pessimistic on the Trump agenda, those relieved of regulations have been more positive. Calculated Risk provides analysis and this chart:

-

CPI remained benign with an increase of only 0.1% in the core rate. Some see this as bad news since it is below the Fed’s target and/or the take inflation as a signal of economic growth. Growth without inflation is good. It gives the Fed a little leeway.

-

FOMC decision got a positive reception. The small increase in the Fed Funds target was expected by markets, demonstrated by the small change in bond yields. Prof. James Hamilton (Econbrowser) explains why the “balance-sheet reduction is not scaring anyone”. He explains, and also provides some interesting data, importantly noting the effects of other news.

The Bad

-

Industrial production was unchanged. The decline from April’s 1.1% gain was expected, but disappointing nonetheless.

-

LA port data is a subject of some controversy. Calculated Risk sees a positive trend, using a 12-month rolling average. Steven Hansen (GEI) prefers rolling unadjusted three-month averages, but notes some anomalies this time. Data nerds should read both pieces in detail to understand how the methods chosen affect what you conclude.

-

Michigan Sentiment declined to 94.5 from a prior of 97.1.

-

Retail sales declined 0.3% compared to the April gain of 0.4% and expectations of unchanged.

-

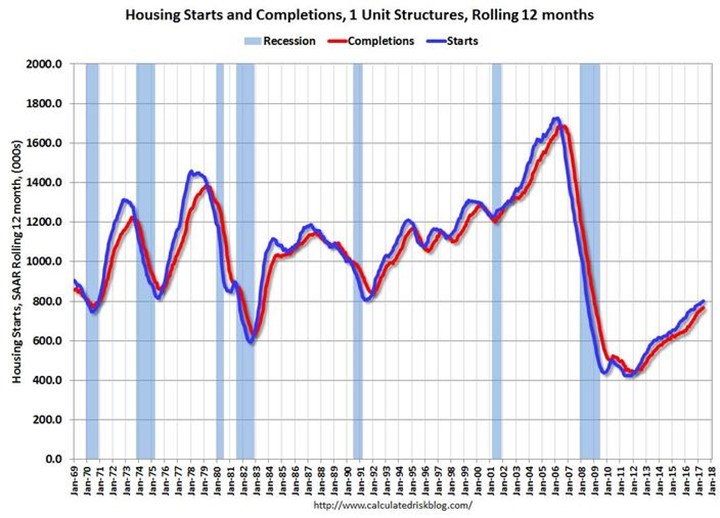

Housing starts declined and missed expectations. Building permits did the same. On the surface this was bad news, but there is some debate over the data. See below for more discussion.

The Ugly

Collateral damage from the Amazon decision to purchase Whole Foods. While it was obviously bad news for competitors in the grocery business, the reach was much greater. Here is a heat map that I tweeted an hour after Friday’s opening.

There may be some logical extensions of the Amazon strategy, but the effect on only four other stocks exceed the entire size of the deal. In some cases, the declines came because of mutual ETF membership, not any specific analysis. This topic deserves more scrutiny.

Noteworthy

Do you think that chocolate milk comes from brown cows? Does anyone? Mrs. OldProf, who grew up in Green Bay and graduated from Wisconsin, notes that most cows are at least partly brown. That would imply a lot of chocolate milk.

Somehow 16.4 million American adults (7%) hold this belief. These people vote and buy stocks. Check out John Harrington for the story and some other surprising examples.

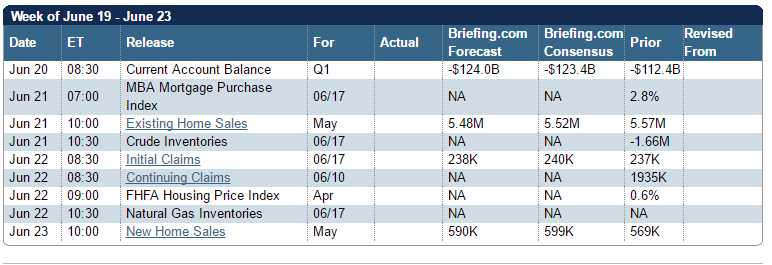

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

The Calendar

It is a very light calendar. Housing data are most important, especially new home sales.

Fed speakers are out in force. Expect more color on the reduction of the Fed balance sheet.

Briefing.com has a good U.S. economic calendar for the week. Here are the main U.S. releases.

Next Week’s Theme

We have the combination of a light week for data, last week’s soft data on housing starts, the Fed rate decision, plenty of scheduled Fedspeak, and a calendar featuring home sales. The ingredients suggest a lot of attention to the housing market. People will be asking:

Is the housing rally over?

Here is a range of opinion.

- The weakening market is a very bad sign. New Deal Democrat analyzes the turn down in permits, starts, and completions. Check out the post for the full story. He promises more to come.

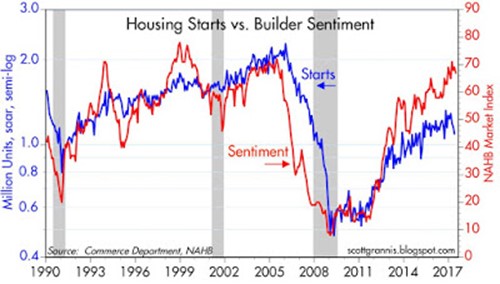

- Gains in homebuilder stocks and builder sentiment provide a better indication. (Scott Grannis).

- Housing starts to remain in the expected range of 3 – 7% growth, year-over-year. Multi-family is solid, but the increasing trend is over. Single family starts are taking over. (Calculated Risk).

- The monthly data present a misleading picture. Steven Hansen (GEI) explains how to interpret the difference between permits and completions.

As usual, I’ll have more in my Final Thought.

Quant Corner

We follow some regular featured sources and the best other quant news from the week.

Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update.

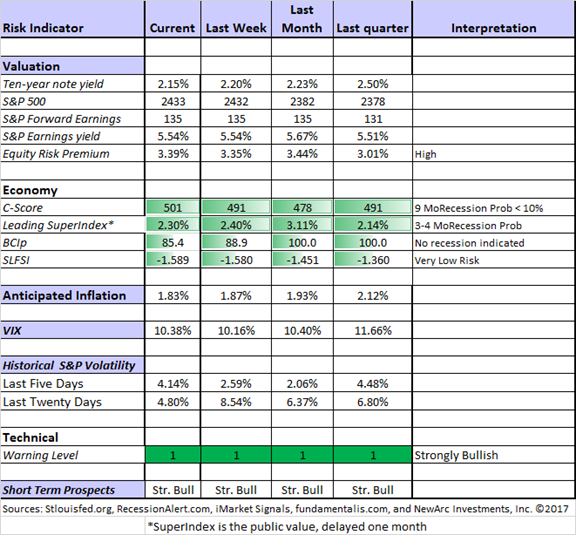

The Indicator Snapshot

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score.

RecessionAlert: Strong quantitative indicators for both economic and market analysis.

Georg Vrba: Business cycle indicator and market timing tools.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

Doug Short: Regular updating of an array of indicators. Great charts and analysis.

We should expect a raft of forecasts from newly-minted recession experts. This example takes the good record of the inverted yield curve and extrapolates from small recent moves. Part of the extrapolation is from some dubious “technical analysis.”

The yield curve is part of our recession forecasts. The influence of other important variables is considered, along with the likely timing. Articles that feature the ‘R’ word are popular, but usually misleading.

Insight for Investors

Investors should have a long time horizon. They can often exploit trading volatility!

Best of the Week

If I had to pick a single most important source for investors to read this week it would be Wade F. Slome’s excellent analysis of the stock market rally – accompanied by “worry, pessimism, and skepticism.” He describes his list as a “small sample.”

He notes as follows:

the endless laundry list of crises and concerns has not broken this significant, multi-year bull market. In fact, stock prices have more than tripled since early 2009. As famed hedge fund manager Leon Cooperman noted:

“Bull markets don’t die from old age, they die from excesses.”

On the contrary to excesses, corporations have been slow to hire and invest due to heightened risk aversion induced by the financial crisis. Consumers have saved more and lowered personal debt levels.

Read the full article to see his warning signs – a combination of several trends.

Stock Ideas

Simply Safe Dividends does his usual careful analysis of restaurant supplier Sysco (SYS). The dividend is safe, but there are some issues on the horizon. Amazon, which he regards as unlikely to compete in this space, and extra debt taken on for a recent acquisition. That said, he assigns a “dividend Safety Score” of 97. DIY investors interested in dividends should read this post carefully. This is the kind of work required.

A brief digression – which I hope you will enjoy. On trading floors people are watching different things. There is no reason to have everyone covering the same news flow. When there is news, we often shout it out so everyone knows what is happening. This is one reason that managers often choose to work from a desk on the trading floor.

When I see a Sysco truck or news about the stock, I am reminded of a Cramer anecdote about how to avoid confusion:

“Wrong Sysco ( SYY) preannouncing!”

In a market that is so Cisco-dominated ( CSCO) — and believe me, this is Cisco-dominated — just the sheer possibility that someone might take Cisco shares on Sysco saying something positive required that our trader shout out the good news for the food broker.

Chuck Carnevale offers a comprehensive analysis of AbbVie, which he notes has growth, value, and high yield. The analysis uses the stock as an example that helps explain his method. You get both an interesting idea and some information strong stock-selection methods.

Energy stocks? John Butters of FactSet reports that this sector accounts for nearly half of the Q2 growth in earnings for the S&P 500.

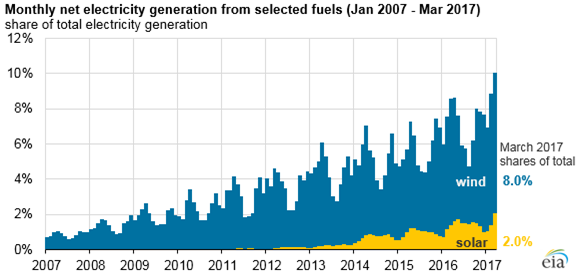

And how about wind and solar energy? The EIA reports that monthly generation from these sources has reached 10% of the total.

A lagging railroad? Barron’s Trader Extra recommends a look at the Genesee and Wyoming railroad (GWR). You cannot guess where they operate! It is an interesting idea, although real value depends upon a resumption of earnings growth.

Personal Finance

Abnormal Returns always has first-rate, daily links for investors. His Wednesday topic is personal finance – of special interest to the individual investor. I especially liked the discussion about the recent reversal for value stocks, the underlying factors, and the long-term success. The Bloomberg piece includes a range of good sources and provides a balanced perspective. Also excellent is the advice from Todd Wenning on how an investor should avoid distractions. Hint: Why do you think your brokerage makes it easy for you to see online quotes?

Seeking Alpha Senior Editor Gil Weinreich has an interesting topic every day. This week I especially enjoyed the renewed discussion about thrift versus economic growth. Your own viewpoint is probably reflected and discussed.

Value versus Growth

GMO notes that value stocks showed strong gains in 2016, which have been erased in 2017. There are always shifts, but this has been much more dramatic than usual. They provide an exhaustive analysis of the trends and possible causes and highlight this conclusion:

Overall, the lion’s share of the performance gap between value and growth across the globe can be accounted for by an expansion in multiples that has outstripped even the habitually bullish analysts’ expectations for future earnings. This should be no small consolation to valuation-oriented investors: Multiples running ahead of fundamentals is a classic sign of over-extrapolation by investors

Watch out for….

What is in your ETF holdings. Here is a little test. If you own an ETF, try to name the top holdings. If you do not like a particular stock, go the other way. Is this a big holding for some of your ETFs?

Final Thoughts

This week’s topic raises interesting questions that have relevance for many other current issues.

Topping markets? The first sign of a rollover in an economic series always gets a reaction. One viewpoint is that it is a clear sign of a top – time to expect the worst. Often it simply puts us on alert, but requires more evidence. If you look at a data series of almost anything, you will see small declines from a top followed by further increases.

Economic relationships do not work like light switches. Changes are not accurately described as two-person transactions – buyer and seller. A change in mortgage interest, for example, affects the point of intersection of supply and demand curves. It shifts the supply at a given price. While we know that this reduces quantity, we do not know by how much.

Even after we improve the analysis by thinking of supply and demand curves, we must consider the micro – the behavior of the individuals making up the curve.

- Some buyers, who have been on the edge of a decision and fearing higher rates, may step up. (See Diana Olick citing this as the reason behind the jump in mortgage applications). This changes the shape of the demand curve.

- Some sellers, sensing a tightening market, may absorb some of the implied price increase. This changes the supply curve.

Anyone who begins with a conclusion that “buyers are priced out” is leading with his chin.

Demographic changes? Millennials are starting families and establishing homes. The worries about the overhang of foreclosure homes has decreased. The big wild card now is the level of future immigration. (See this excellent post from Calculated Risk).

One reason that I continue to love the homebuilders is that the factors moving interest rates higher – stronger economic growth and higher wages – are the same as those that will increase housing demand.

What worries me…

- Continuing contention in Washington. We will need bi-partisan compromise to deal with the big issues like growing government debt and entitlement programs, not to mention infrastructure and tax reform.

- The unknown effects of ETF trading.

…and what doesn’t

- Concern about “escape velocity.” Those who do not understand the current economic cycle rely on mistaken metaphors. They are attempting to persuade through language alone, without analysis.

- The unwinding of the Fed balance sheet. Any reasonable path will barely ripple the market.

© NewArc Investments, Inc.

Read more commentaries by NewArc Investments, Inc.