*The following is adapted from a recent speech given by Steven Romick*

To some of you, all Americans are exactly alike. I may as well be President Trump. Like him, you have no idea what I’m about to say.

Well, check that: it often seems he has no idea what he’s about to say, and that’s a major source of uncertainty in all of our lives, both personally and professionally… that can create an insecurity on which much of the business media preys.

The business media, like President Trump, looks for winners and losers…. They’ll highlight the stocks du jour that are either performing really well, and then, in the next breath, show a graphic of those that tanked. Stocks go up…. Stocks go down…. Sectors do well, sectors do poorly. It’s entertainment. Ultimately, I don’t find it very valuable. It’s no more than tabloid reporting. It’s their version of who is sleeping with whom and who has fallen off the wagon. Short-term market price movement does not tell us anything about long-term value.

At any given moment, the media highlights whichever few stocks are driving the stock market. In the U.S. in 2015, it was the FANG stocks – Facebook, Apple, Netflix, and Google.

In the UK in 2016, it was just three rebounding commodity companies and one financial that accounted for more than three-quarters of the FTSE’s 14.4% return.[1]

For as long as I’ve been investing, it has generally been the case that just a few stocks drive these indices; and that these few stocks pull the lesser performing stocks along with them. The investing community has come to define this law of financial physics as “positive skew.”

“Positive skew” now joins “active share” in that lexicon.

Passive management advocates don’t use this phrase to praise the active manager, but rather to poke at us.

What the passive manager would have you believe is that, thanks to exorbitant fees, to transaction costs, and to not picking winners, it's always better to index. I’ve read that maybe just 10% of the managers can outperform the market over time, and the odds that you will find that manager: even lower still.

Armed with some selective data, some critics of our approach say that that it is unlikely an active manager will consistently own those few stocks that drive stock returns in any given year, let alone year in and year out. Let me read you an excerpt from an essay in the Financial Analysts Journal:

“Disagreeable data are streaming out of the computers of…the... performance measurement firms. Over and over and over again, these facts and figures inform us that investment managers are failing to perform.”

Charles Ellis wrote this more than 40 years ago.

So these arguments have been around a long time. But I am not here to tell you that there isn’t truth to Mr. Ellis’ 1975 essay, which he called: “The Loser’s Game.”

Fundamentally, passive investment is always going to look great during a long-lasting bull market.

If someone wants market rates of return and can withstand some volatility, then it can also serve as an efficient, low-cost tool. The further you get away from a bear market, the greater the number of people who have convinced themselves they can handle the downside – until the next time, of course.

In the interim, if the indices are performing well, then you can bet that many investors – individuals and professionals, alike – are going to feel pressure to do whatever they can to ride the bull.

They fear being different. Tracking error is bad. Owning too many securities in every sector is a sure way to avoid being fired for being different. I’d rather spend my time surfing than to have to invest like that.

Thanks to the accelerated increase of passive investing – now around 40% of the U.S. market – I’m confident that there will be a period when it will look really easy to beat a benchmark – followed by another time when, again, it won’t.

This academic argument against active investment is fundamentally flawed because it’s built on a false premise, which holds that only the best performing stocks will drive returns. The argument doesn’t consider the other side…. A maxim I’ve taken to heart….

If you avoid the worst performing stocks, you can still put up good numbers. (I’ll leave it to you to conclude if I’m just talking my book.)

Further, these critics place too much weight on performance in each year… and ignore performance over a full-market cycle.[2] This leads to short-termism. And short-termism is a breeding ground for all sorts of cognitive dissonance to which smart people fall prey when trying to adapt and join the crowd.

People viewed the internet as a fast-growing disruptive game changer in the late 1990s. And so it was, but as you know, internet stocks of that era were largely priced at wholly illogical levels.

Yet, many smart people couldn’t handle not participating. Maybe they were worried about not making as much as their friends. Or maybe they were worried about being fired. Whatever the reason, if they participated they generally lost badly.

In 2008, we sat on the precipice of a depression and many investors quickly liquidated their stocks and bonds, believing the economy would get worse, and stocks would continue to decline. It appeared correct to do so… for a time.

Some of those who exited the market realized their mistakes and came back to the market… down the road… after the economy found firmer footing… but also after prices had already rebounded.

Short-termism.

Patience, a long-term focus, and avoiding the fads are key for successful investing. Some of the most successful stock investors of the last few decades in the United States aren’t known for finding the latest and greatest.

I give you as just a few examples: Warren Buffett, Seth Klarman, Jean-Marie Eveillard, and my former partner of two decades, Bob Rodriguez. Each compiled a long track record respected by investors of all types.

Each had their share of winners, but none created their enviable performance by owning those few golden stocks of a given year. They won by not striking out, rather than by hitting grand slams. In other words, they won by not losing – emblematic of our approach.

We allow ourselves the opportunity to participate on the upside… while protecting ourselves on the downside…. And we focus, more centrally, on fundamental research on companies that can create value over time.

I’d like to show you from my own experience in managing money over the last few decades, that some of the best investment decisions in my career have been acts of omission – avoiding those securities, industry sectors, and asset classes that we believed offered a poor risk versus reward.

FPA’s Crescent Fund (“the Fund”) operates with a global, go-anywhere mandate and invests across the capital structure, using mostly stocks and corporate bonds to seek equity rates of return, while, at the same time, avoiding a permanent impairment of capital.

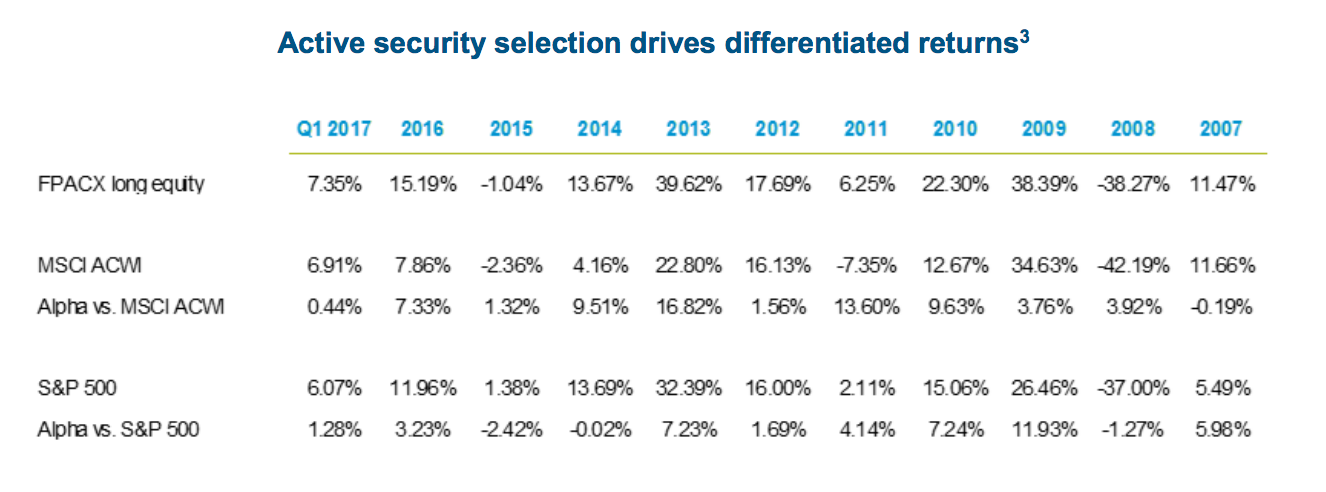

Let’s look at just the stock returns of our FPA Crescent Fund[3] in this past decade (gross of fees). You can see there were times we underperformed. When compared to the global indices, we underperformed in just one year of the past ten. When compared to the U.S. market, we underperformed in three. Our worst relative showing was just -2.4% vs the S&P 500 in 2015. Our average underperformance of these four years was just -1%.

There were five instances where our equity holdings outperformed the global indices by more than 5%; and, there were four instances where we outperformed the U.S. market by the same percent. The average alpha delivered in the years when we bettered our benchmarks was 6-7%.

This has aggregated into some poor periods when the bulls were a runnin’. Our fund has underperformed about 87% of the time when the S&P 500 has booked a trailing five-year return in excess of 10%.

However, we beat the market in 100% of the trailing five-year periods when the market declined; and, almost 98% of the time when the trailing five-year returns fell in the 0-10% range. In addition, unlike the S&P 500, FPA Crescent has had positive performance in every rolling five-year period. We exceeded our goal of doing as well as the market mostly by avoiding permanent impairments of capital. This is in line with how we expect the Fund to perform.

To continue reading, go here.

[1] Royal Dutch Shell A; Royal Dutch Shell B, BP, HSBC Holdings, and Glencore contributed 11.1% to the FTSE Index 2016 return.

[2] Steven Romick and Ryan Leggio, “The Importance of Full Market Cycle Returns.” See: http://fpafunds.com/docs/special-commentaries/2015-04-29-market-cycle-performance-final.pdf?sfvrsn=2

[3] The FPA Crescent Fund discussed in this adapted speech and the performance data reflected herein is based upon the long equity segment of the Fund, and is provided as supplemental information. Performance is presented gross of investment management fees, transactions costs, and operating expenses, which if included, would reduce the returns presented. Performance for 2017 is through March 31, 2017. Past performance is no guarantee of future results. Please refer to the end of the adapted speech for important disclosures.

[4] Source: Morningstar Direct. The chart illustrates the monthly five-year rolling average returns for the Fund from July 1, 1993 (the first full month of performance since inception) through March 31, 2017 compared to the S&P 500 Index. The horizontal axis represents the five-year rolling average returns for the Index, and the vertical axis represents the Fund’s five-year rolling average returns. The diagonal line illustrates the relative performance of the Fund vs. the Index. Points above the diagonal line indicate the Fund outperformed in that period, while points below the line indicate the Fund underperformed in that period. The table categorizes returns for three distinct market environments: a “down market” is defined as any period where the five-year rolling average return for the Index was less than 0%; a “normal market” is defined as any period where the five-year rolling average return for the Index was between 0-10%; and a “robust market” is defined as any period where the five-year rolling average return for the Index was greater than 10%. There were 226 five-year rolling average monthly periods between July 1, 1993 and March 31, 2017. Past performance is no guarantee of future results. Please refer to the end of the presentation for important disclosures.