In the era after the Financial Crisis, pundits, investment commentators, and the media falsely maintained a constant proclamation that interest rates were just about to rise and that the collapse of the bond market was imminent. When the Federal Reserve Bank (Fed) first lowered interest rates to 0%, the pundits proclaimed irresponsibility and that inflation would skyrocket. Then came Quantitative Easing I & II, and the claim that this equates to the printing of money, which surely had to lead to inflation, irresponsible debt, and rising interest rates. And there is the ever-present adage that interest rates are just too low and that they simply have to “normalize”. The Fed has even stepped in and raised the fed funds rate three times, only to see the yield curve flatten and to witness longer-dated interest rates remain relatively unchanged. Now, with the election of President Trump, the debate has switched from monetary policy to fiscal stimulus. This time the thought pattern is that fiscal spending and tax cuts, which simply amount to massive government borrowing, will lead to rising growth, inflation and interest rates. All the while, interest rates have remained peculiarly low, inflation has tended towards deflation, and we have experienced the worst economic recovery in modern history according to real Gross Domestic Product (GDP). What is it about this post-2008 economic environment that is so different from the prior 50 years of the U.S. economy and traditional economic theory?

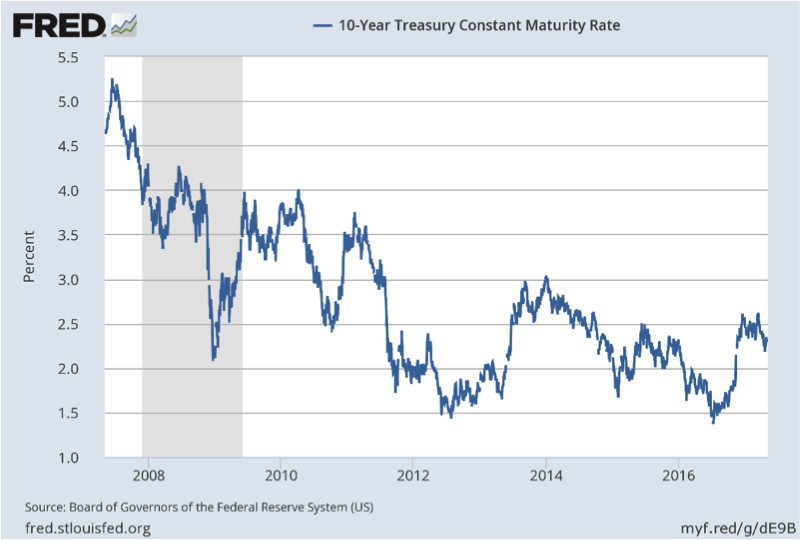

Given that we now have 6 months under our belt to digest the expected policies of the Trump administration, a simple check of interest rates shows little material change relative to the post-2008 environment.

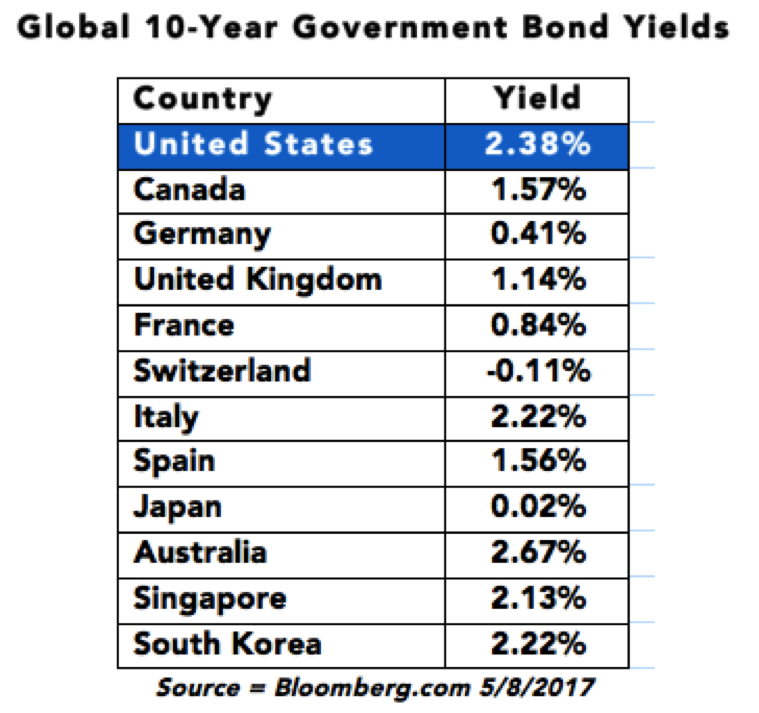

While some might think that these yields paid on high-quality bonds are too low, a simple comparison relative to other first world nations’ bond yields reveals that U.S. interest rates are actually relatively high. Could it be interpreted that some of the expected growth in inflation and debt are already considered in current yields? U.S. interest rates are even higher than those in Italy and Spain, which are, it can certainly be argued, lower credit quality countries.

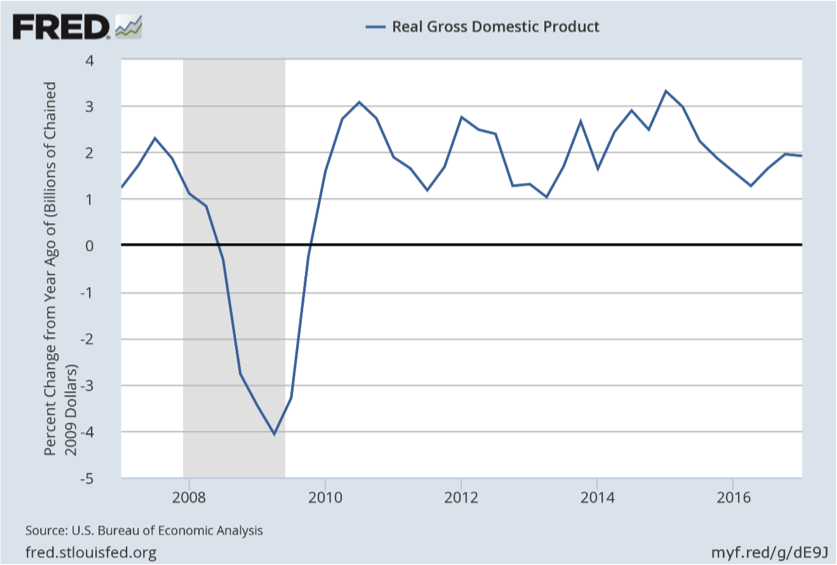

Real GDP growth, too, has remained relatively constant in the post-2008 environment, and after 8 years, it still represents the worst economic recovery in modern U.S. history.

It seems that even though the Fed has maintained near zero percent interest rate levels and the debt levels have been greatly elevated, this leverage has not lead to elevated levels of growth or inflation. All that the leverage has managed to achieve is maintaining the current low level of economic growth against a backdrop of constant deflationary pressure.

While the economy is showing signs of recent reflation – a little more growth, a tick up in inflation, and improved earnings – it is those pesky dark clouds on the horizon that are keeping many investors from being too optimistic about the long-term. The looming problems with population, debt, and globalization continue to warn of deflationary pressure.

Population:

Expanding the population is the most direct way to drive economic growth. As the population grows, more people will have jobs, more products will be consumed and more will need to be produced . It’s not only the size, but also the shape of the population, which has a great impact on potential growth. The younger a population, the more family formations and births are likely to occur. Family formations provide the biggest bump to growth, as this is when the maximum growth in spending occurs. The opposite is true, too; the older a population, the slower the potential growth. Another often overlooked economic growth factor is in immigration. Importing young talents can cause a significant economic boost.

Across the entire first world, Baby Boomers make a up large percentage of the population. In the U.S. alone, there are 76 million Baby Boomers, and the oldest of the demographic turned 70 last year. It is evident that the retirement wave is upon us, and last decade has seen a steady decline of the labor force participation rate as Baby Boomers step into retirement. Retirement brings with it slower economic activity as workers relinquish their higher incomes to live off their retirement savings and on a fixed income. To counterbalance a baby boom, there is an echo boom – in this case, the Millennials. What is different this time is that unlike previous generations, this second wave of population is not having children or forming families at near the same rate as previous generations. Across the entire first world, birth rates are below replacement rates for populations. There is also evidence that the Millennials are already struggling with debt and high asset prices. What’s becoming painstakingly clear is that the first world demographics will continue to be a deflationary force for years to come.

Debt:

The Fed has managed to close the post-2008 spending gap by keeping interest rates low and borrowing high. But leverage tends to lose its power over time as borrowers reach their maximum capacity. The need or desire to take on debt decreases as the population ages, too. Thus, the rate of return on every dollar borrowed diminishes over time.

The transmission mechanism of debt is that when consumers borrow from the bank, the bank borrows from the Fed. The money seemingly comes out of nowhere. Money is created, which is why it is referred to as leverage. But when the debt is paid back, the opposite effect occurs. Deleveraging is when real money, out of real people’s pockets, has to be removed from the economy and sent back to the bank. While the first world is awash in liquidity, it is also levered to the gills. Debt levels have never been higher, for consumers or federal governments. One day all this debt will need to be reduced, or worse, written off. Either way, deleveraging as an action is massively deflationary.

Globalization:

The globalization of everything that has unfolded over the past 30 years has also driven prices lower. It would seem self-evident that more competition drives prices lower, but when combined with technology, the deflationary pressures seemed to accelerate over the past decade. We only need to look to amazon.com for clear evidence of the creative destruction and deflationary pressure that result from this combination.

So, what is the risk of crying wolf about interest rates and inflation rising? Despite the lingering evidence of deflationary pressures, pontificators still proclaim that interest rates are about to shoot up and that bonds are a risky asset. However, while seeking to avoid potential loss situations is a conservative posture, there are always unintended consequences. A constant barrage of fear surrounding rising interest rates may have driven conservative investors to run to the “safety” of stocks. With banks paying little to no yield, and with bonds seemingly just about to succumb to the fate of rising interest rates, investors are turning to stocks like it is 1999. Parallel to the late ‘90s, investors may be jumping out of the pot and into the fire to chase stocks higher now. By almost every measure, stocks around the world are near all-time high valuations. History books tell us that the worst declines in stock markets have occurred when valuations have been near current levels, and following the Fed’s tightening campaigns. During periods of economic panic, high-quality bonds often increase in value, but stocks have commonly experienced losses in the 30% range.

So, are we setting ourselves up for a perfect storm? It is fairly safe to assume that the savings of the large portion of the first world population, that just happens to be about to retire, is currently at its lifetime maximum. Debt levels, too, are at peak levels. The economic balloon is stretched thin. Awash in liquidity, capital markets have to absorb all of this money, which explains why stocks, bonds and real estate are simultaneously near all-time highs. But, with hundreds of millions of people across the world gearing up for retirement, any hiccup in the “growth plan” would be disastrous.

Of course, interest rates may rise, they may fall, or they may stay the same. The current administration’s intention to reduce taxes and increase the federal debt may drive inflation and interest rates higher, or the policies may not work as hoped. However, the deflationary forces are more known factors that don’t seem to be going away anytime soon.

We don’t like to make bets here at Frontier, especially when all the pontificators are lined up on the same side of the canoe. We prefer to perform well through a multitude of market environments, not just the outcome we “think” is going to happen. There are many known unknowns in investment management, and outcomes have a tendency to be unexpected. But, we do know that stocks like a good economy, bonds like a bad economy, and commodities like inflation. Despite the human desire to chase stock prices, as well as the equally universal fear of rising interest rates, even a betting man should hold some combination of all three of these asset classes.

Past performance is no guarantee of future returns. Performance discussed represents total returns that include income, realized and unrealized gains and losses. Nothing presented herein is or is intended to constitute investment advice or recommendations to buy or sell any types of securities and no investment decision should be made based solely on information provided herein. There is a risk of loss from an investment in securities, including the risk of loss of principal. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable or suitable for a particular investor's financial situation or risk tolerance. Diversification does not ensure a profit or protect against a loss. All performance results should be considered in light of the market and economic conditions that prevailed at the time those results were generated. Before investing, consider investment objectives, risks, fees and expenses.

Exclusive reliance on the above is not advised. This information is not intended as a recommendation to invest in any particular asset class or strategy or as a promise of future performance. Information provided herein reflects Frontier’s views as of the date of this newsletter and can change at any time without notice. Frontier obtained some of the information provided herein from third party sources believed to be reliable but it is not guaranteed and Frontier does not warrant or guarantee the accuracy or completeness of such information. The use of such sources does not constitute an endorsement. Sources include, fred.stlousi.org, Bloomberg.com and the US Census Bureau. All calculations by Frontier Asset Management, LLC.

© Frontier Asset Management

Read more commentaries by Frontier Asset Management