“Let me warn you, Icarus, to take the middle way…”

The words of Daedalus to his poor son Icarus ring loudly in our ears as we watch the equity markets continually reach new highs and see bond values begin to sink with the offing of increased interest rates. So, how does one find the middle way in a rising rate environment? As long-time market observers and participants, we’ve never seen a more attractive moment for convertible securities.

These hybrid securities have outperformed stocks and bonds when interest rates increase.

If you invest in bonds for safety, you have to be concerned about interest rates going up, because as rates increase the value of your bond portfolio declines. If the economy grows, as experts expect, and the stock market continues to provide positive returns, these returns can be reduced by sticking with bonds.

Still, depending on your risk profile, you may not want to increase your equity exposure because markets are near historic highs and any slight bump in the road could cause a pullback in stock prices.

Fortunately, there’s another kind of investment that combines the stability and income of bonds with the growth potential of stocks.

What’s the outlook for the economy and interest rates?

We’re coming off one of the longest bull markets in bonds in history. Rates have been falling since the early 1980s. It’s like the inverse of gravity. What goes down, must eventual come back up. The CFA-types in our office call it mean reversion. Most economists think that the economy will continue to grow at a steady pace for the next couple of years, and that rates will rise along with this moderate growth. Right now the economy is expanding by between 1 to 2%.

At the same time, the Federal Reserve has already started putting the brakes on this growth in its efforts to fight inflation beyond the Fed’s 2% target. The Fed has already raised its benchmark Federal Funds Rate by 0.25% three times since it shifted monetary policy in 2015 – December 2015, December 2016 & March 2017. Experts expect that it will make two more increases in 2017, thus providing more room for poor Icarus to fall.

The net effect? We expect growth of 2.5% to 3% this year – that’s assuming that the steady but slow growth that we’ve experienced over the last several years gets a boost from the fiscal policy and deregulation initiatives. In this scenario, long-term rates should rise. We expect 10-year Treasury yields to rise from about 2.30% now to close to 3% by year end.

Understand your options

Rising rates aren’t necessarily good or bad, rather it’s about how certain securities react to it. Let’s look at how rising rates would affect the major asset classes right now:

-

Bonds: Bond yields are still at historically low levels following a 30+ year bull market. This run could be over and the value of most bond portfolios would fall if rates continue to rise.

-

Stocks: By some metrics, stocks are also expensive compared to historic prices, so they too may have limited potential for further appreciation with heightened risk. Yet if the President can push through tax reform or regulatory reform or infrastructure spending, the markets could move higher. Investors are in a tough spot – not wanting to miss out on future appreciation, but also worried about risk.

-

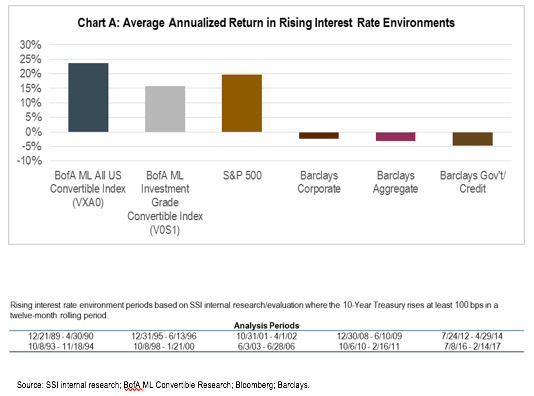

Convertible bonds: Convertible bonds offer the income and stability of bonds, but they tend to be less sensitive to rising rates. Just as important, they allow investors to participate in the growth potential of stocks – but with less exposure to risk. In fact, as Chart A below shows, convertible bonds have outperformed stocks and bonds during most periods when rates rose sharply.

Convertibles have historically outperformed in rising rate environments

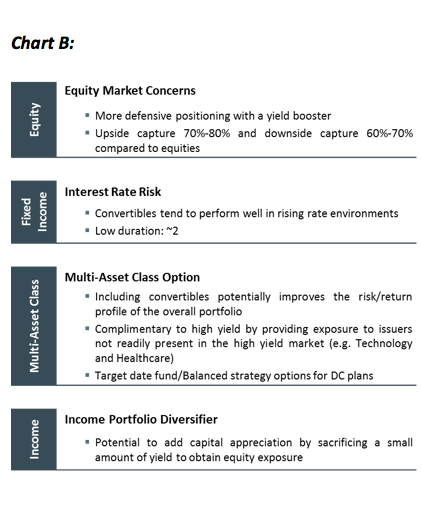

Incorporating convertibles in a diversified portfolio

Convertible bonds share certain characteristics with bonds and others with stocks. Because they share the characteristic of principal protection with bonds, investors do incorporate convertibles into the fixed income portion of their portfolio. Because they participate substantially in the underlying equity’s upside with muted risk, other investors incorporate them in the equity portion of their portfolios. Some rely on their hybrid nature to include them in an “alternative investment allocation,” if they have one. Chart B below outlines how convertibles perform differently enough from stocks and bonds that they can provide meaningful diversification benefits.

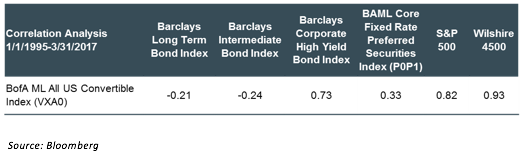

Over time, however, convertible bonds perform more like stocks than any other asset class. As Chart C below shows, they have an 80% correlation to the S&P 500 Index, meaning that 80% of their performance mirrors that of the index. Interestingly, convertible have a negative correlation with most bond indexes – quite often convertibles and bonds can move in opposite directions.

Convertibles perform more like stocks than bonds

Chart C:

By combining assets that perform differently under the same market conditions, investors can increase their chances of having part of their portfolio in the best parts of the market – while reducing exposure to the worst. Over time, diversified portfolios tend to perform better than single-asset portfolios with less volatility.

Diversifying with convertibles

Let’s look at two scenarios for diversifying with convertibles, one for an equity-oriented investor, the other for an investor focused on fixed income.

First consider an investor who holds convertibles as part of his or her stock allocation.

If you own equities but are concerned about a disruptive market event—like last summer’s Brexit Vote or escalating tensions in North Korea— convertibles can help you reduce risk. Remember even if stock prices fall, you can always hold the convertible to maturity and get back your principal plus interest1.

Yet at the same time, you continue to have exposure to stocks, which historically and over long periods of time have produced higher returns than any other asset class.

Now let’s look at how convertibles can add value as part of a bond portfolio.

As we saw in the correlation table, convertibles function differently from most government and corporate bonds. In fact, during most market environments, convertibles do the opposite of bonds. Generally, when rates rise and bond prices fall, convertibles outperform while when rates fall and bond prices go up, convertibles may underperform. As a result, by adding convertibles to a fixed income portfolio, you can obtain diversification benefits that increase returns without adding volatility.

1 Assuming issuer does not default

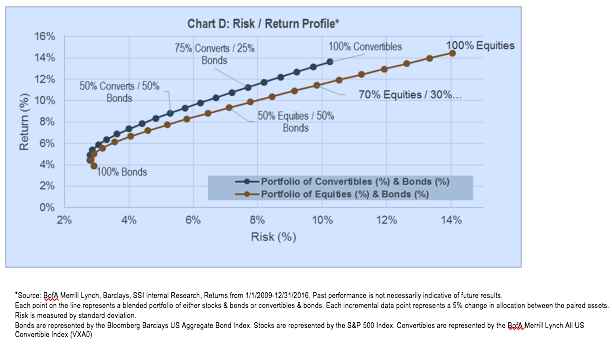

As you can see in Chart D below, adding a modest allocation to convertibles boosts returns while reducing overall fluctuation in portfolio value. The size of that allocation will vary depending on each investor’s goals and risk tolerance, but in most cases, it ranges from 5% to 20%.

Adding convertibles can increase portfolio returns without adding risk

Finding value in the convertible market: One size does not fit all

Not all convertibles are created equal. Some are more like stocks, in that their performance mostly comes from increases in the value of the issuing company. Others act more like bonds, because their companies’ stock prices have stayed the same or declined, so that most of the return comes from interest payments. Still others provide a mix of interest income and appreciation potential.

Over time, this middle category – called total return convertibles – has produced the best risk-adjusted returns for investors, combining the relative stability and income of bonds with the growth potential of equities.

At SSI Investment Management, our portfolios emphasize total return convertibles under most market conditions, because we believe they provide investors with the best mix of return and limited risk.

The importance of research

Investing in convertible securities requires several different types of expertise. Analysts must first understand the structure of each convertible – length of time before the bond matures, how many shares it can be converted into, and how far has the stock price of the issuer risen or fallen since the bond was issued.

Then, because convertible performance is so tightly linked to stock performance, convertible portfolio managers need to have access to research on the underlying companies. How much is the company earning now? What is its competitive landscape like? What are its prospects for future growth?

And finally, because convertibles pay interest and return principal like bonds, investors need to know how credit-worthy the issuers are. How strong is the issuing company’s balance sheet? How much has it borrowed and at what cost? What are the chances that it will default on interest payments or principal?

It takes access to all three types of research to succeed in managing convertibles. If you’re considering investing in a convertible fund or portfolio, make sure your manager has the right kind of analytical capability and support.

Making convertibles a strategic part of the portfolio

In an environment of rising rates and stock prices, like the one we’re currently in, convertibles help minimize downside risk while participating in the upside of the stock market. While convertibles are attractive right now, they also make sense as a permanent strategic part of most investment portfolios. They offer significant diversification benefits for both stock and bond investors, as well as protection from the risks of sharp market downturns.

We know it’s tempting to fly to the sun, but experience and history remind us that a middle way often offers the best way.

© SSI Investment Management Inc.

Read more commentaries by SSI Investment Management