Investors are wary about US stock multiples. But elevated valuations of high-growth stocks may be deceiving. Growth overachievers that can deliver persistent fundamental strength often make a mockery of their short-term valuations in hindsight.

Valuations are important for equity investors. However, simple price/earnings metrics don’t tell you whether a company is cheap or expensive. For that, we believe you need to study a company’s competitive positioning and business returns, and how its growth is funded. It takes a lot of fundamental work—and a long-term horizon.

Exceptionally high growth is rare—and often fleeting. So, the companies that do a great job of converting the promise of growth into the reality of growth should be worth a higher price tag than the average stock in the market.

EARNINGS MISS THE MARK

As we’ve written in prior posts, we think that fundamental returns—or a company’s underlying profitability—are much more illuminating than earnings for identifying long-term growth companies. Our yardsticks are return on invested capital (ROIC) and return on assets (ROA), which tell us whether a company is investing intelligently to grow profits. Stocks of firms that generate an ROIC above a certain threshold, the so-called cost of capital, tend to outperform over the long term. Typically, management of these companies is putting capital to productive use and consistently reinvesting profitably for long-term growth.

DO DREAMS COME TRUE?

These overachieving companies come in different forms. Some are dreams come true or early-stage growth companies that deliver robust growth by transforming markets in unexpected ways. Some examples include Intuitive Surgical, a pioneer in robotic surgical tools, and Facebook and Alphabet Inc., both in digital advertising.

Others are firms like Starbucks and Xilinx, a leader in highly complicated integrated circuits that is enabling applications in fast-growing technology markets such as cloud computing and embedded vision. These are large, mature, well-run companies that have successfully overcome profit slowdowns in the past by re-inventing themselves to create new opportunities for faster growth. In both cases, these companies have powered through uncertainty by being nimble, creative and market defining. Service-oriented businesses, notably those in consumer, science-driven healthcare (biotech) and technology, tend to breed these quality companies.

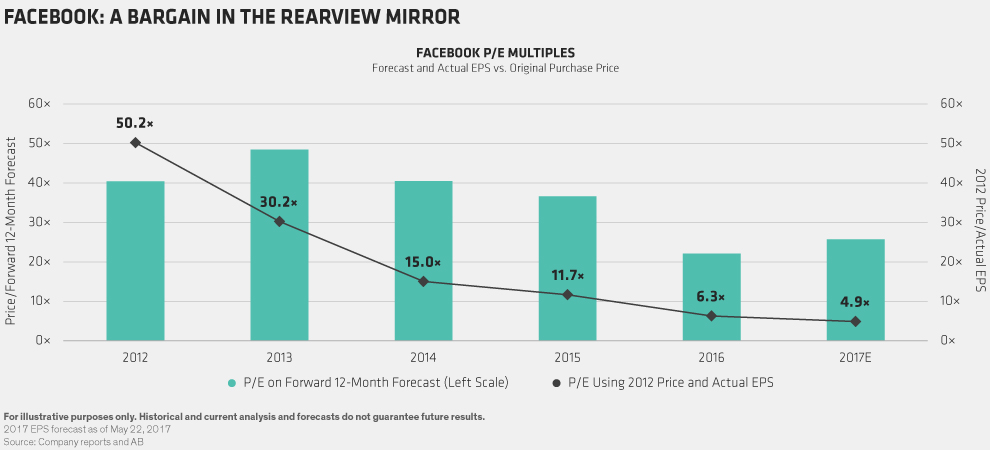

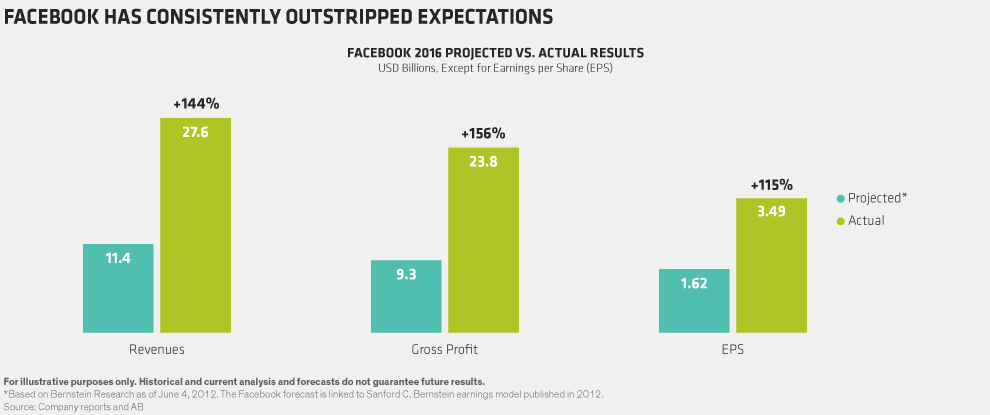

Exceptional high-growth companies aren’t easy to value. Take Facebook, the quintessential disruptive-growth story. Over its entire five-year history as a public company, Facebook has always looked expensive relative to its present-day forecasts. But since then, the social media company has also repeatedly surpassed the market’s original forecasts for revenues, profits and earnings per share (Display).

Entering each calendar year since its IPO in 2012, Facebook traded at what seemed like unjustifiably high multiples relative to the market. Only in retrospect do we see what a bargain the stock was back then (Display). Fundamental analysis can help investors determine whether Facebook can continue its streak in the future.