SUMMARY

- Europe and China appear to be joining the U.S. in expansionary mode. Flows to their currencies are likely to restrain the strength of the dollar.

- Populist mandates around the world are likely to further drive pro-growth policies and inflationary pressure is seen increasing.

- Investors are trapped in trillions of dollars of low-yielding, long-duration assets. When they exit this "crowded trade," volatility is likely to result.

- We favor a flexible, opportunistic approach to capitalize on volatility in a challenging fixed-income environment.

In this Q&A, Kathleen Gaffney and Henry Peabody share their outlooks for the bond market and the impact of stronger global growth, and how they seek to position the Multisector Income strategy.

Kathleen, could you explain why you’re a bit more bearish on the dollar than the market?

The market currently seems to have a view that the dollar is going to continue to strengthen, mainly because of the Fed's recent 25 basis point increase and the hawkish language that accompanied it.

We recognize that in the short term, hiking rates may provide a boost to the dollar, but there are a number of reasons why we think it is unlikely to continue appreciating at the current pace. First, consider that Europe and China, along with the U.S., appear to be in an expansionary mode. This is evidenced by recent Purchasing Managers' Index (PMI) data as well as sharp acceleration of new orders in manufacturing.

Assuming other major economies are in growth mode along with the U.S., it's unlikely that flows into the dollar can continue at the same pace with that kind of competition from other currencies. We are likely to see convergence in terms of rate hikes and growth all around the globe.

Moreover, there is a political aspect to this forecast. The current global political environment contains a strong populist mandate for stronger growth. We are likely to witness a transition from monetary policy to fiscal policy driving the market, and in the U.S. the focus is on bringing back jobs and manufacturing. That's going to be tough to do if the dollar continues to climb, especially given its significant rise over the past couple of years (Exhibit A).

So for reasons driven by our more optimistic view of world growth and the current political climate, we think that the dollar is less likely to appreciate as much as the market is predicting. That means nondollar currencies look more attractive to us.

How does inflation figure in the stronger growth picture?

Since the global financial crisis, inflation expectations have been nonexistent, but we're seeing inflation start to build in the system. The market has been much more concerned about deflation and the inability of global economies to get any kind of traction.

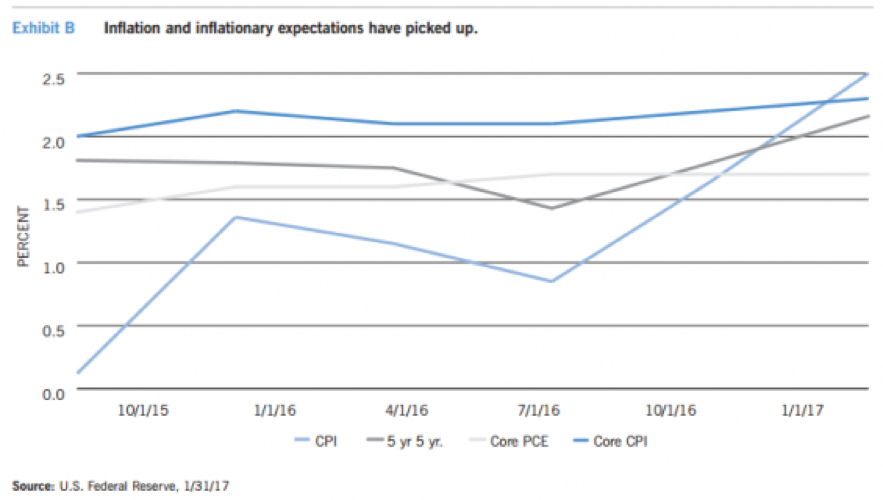

However, Exhibit B shows how dramatically both inflation and inflationary expectations have shifted, especially since the election. Expectations, as measured by TIPS break-even rates (illustrated by the 5-year TIPS, 5 years forward rate in the chart), picked up significantly in the latter half of last year – at 2.2%, as of February 2017, they are at the highest level since June 2015. "Headline" inflation, measured by CPI, has bounced from under 1% in July 2016 to 2.5%; core CPI, which excludes the volatile food and energy sectors, is just slightly less at 2.3%. Core Personal Consumption Expenditures (PCE), the Fed's favorite inflation gauge, at 1.7%, is still below its 2% target.

We are also starting to see tightness in the labor markets, with unemployment coming down quite sharply along with evidence of wages picking up, and average hourly earnings rising. Combine the changing inflation story with the pro-growth political environment and you have a scenario in which nominal growth can beat expectations – that's an important factor in our long-term view.

What does the potential for stronger growth mean for the bond market?

With the changing macroeconomic picture, we have to point to the impact it may have on the "crowded trade" that has built up over the past decade. Quantitative easing incentivized investors to go out the yield curve and/or down in quality to meet their return objectives, as the demand for safe haven assets caused absolute yields to reach very low levels.

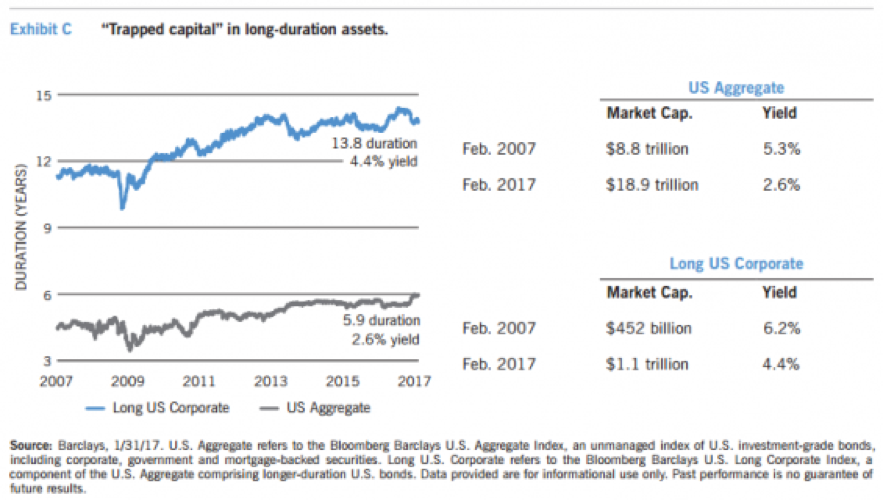

Exhibit C shows the extent to which fixed-income investors have accepted both low yields and long duration. Since the financial crisis in 2008, yields on the Bloomberg Barclays U.S. Aggregate Index (U.S. Agg) have fallen from 5.3% to just 2.6% at the end of 2016, while duration has crept up from about four years to six years. To get the dimension of the "crowded" aspect, the market cap of the U.S. Agg over the past 10 years has swelled from $8.8 trillion to $18.9 trillion.

If we just focus on the long corporate component of the U.S. Agg, we see duration over the past 10 years has increased from around 10 years to 14. Even that component, with twice the duration risk of the U.S. Agg, has had yields fall from 6.2% to 4.4%, and market cap has more than doubled to $1.1 trillion.

Investors trapped in such low-yielding, long-duration assets are finding it very hard to reach their return objectives. How will investors react in a scenario of rate hikes, increasing growth and inflation? If we return to the crowded trade analogy, a lot of people may be looking to get through a small doorway at the same time, as the yield advantage relative to the broad market becomes very slim, with some investors looking at negative real rates of return.

We don't know exactly how investors are going to react, but our guess is that they're going to lead the broad markets in a large way. The potential for this scenario forces a new conversation about how to be positioned. Being flexible and opportunistic may be the best way to generate returns amid the volatility and uncertainty we could face over the next couple of years.

Henry, what is your approach to finding value in this market?

We are staying away from the most interest-rate-sensitive part of the market – U.S. Treasurys and agencies. Typically when valuations and credit are not attractive we will take positions in Treasurys for the purposes of liquidity and income. But with low rates and the risk of rates moving higher we’re very comfortable holding cash right now.

Can you give examples of how the bottom-up, issue-specific approach has worked?

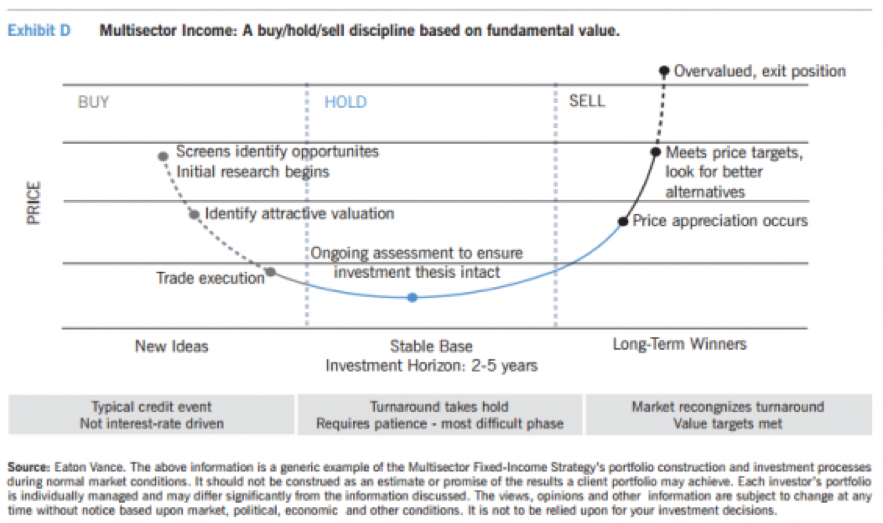

Sure. By way of background, the J-curve in Exhibit D is an excellent guide to our investment process. The line represents the price trend of issues that catch our interest – on the left side, it is typically a credit under pressure that may represent an attractive valuation. Recall that late 2015/early 2016 was a risk-off period in which there were concerns about a global depression and a hard landing in China.

We thought those fears were overblown, but the market nervousness gave us good opportunities to put our rigorous fundamental analysis to work. Around the same time, we were analyzing a technology firm in the data storage sector, and the market was pricing it as if that particular technology was going to disappear.

We disagreed with that assessment – we saw a need for this technology to exist in the long term, as it is frequently used in "big data" configurations. We had to ride the issue down another 10 points from initial purchase along the curve, as illustrated in Exhibit D, but, as we projected, the market's fears receded and pricing has recovered.

By the same token, a good credit opportunity can't necessarily overcome broader market risk – that is a fundamental judgment that is very important in this space. We recently looked at a pharma company whose downside in terms of credit quality appeared slight. But with high-yield valuations stretched and the duration of the bond being on the long side, we decided to pass.

With the potential for higher rates and growth ahead, accompanied by volatility, we are confident that a disciplined approach based on fundamental value is likely to uncover many opportunities. We are ready to take advantage of the upcoming market changes with the strategy's flexibility.

About Risk

An imbalance in supply and demand in the income market may result in valuation uncertainties and greater volatility, less liquidity, widening credit spreads and a lack of price transparency in the market. Investments in income securities may be affected by changes in the creditworthiness of the issuer and are subject to the risk of nonpayment of principal and interest. The value of income securities also may decline because of real or perceived concerns about the issuer’s ability to make principal and interest payments. Investments rated below investment grade (typically referred to as "junk") are generally subject to greater price volatility and illiquidity than higher-rated investments. As interest rates rise, the value of certain income investments is likely to decline. Derivative instruments can be used to take both long and short positions, be highly volatile, result in economic leverage (which can magnify losses), and involve risks in addition to the risks of the underlying instrument on which the derivative is based, such as counterparty, correlation and liquidity risk. If a counterparty is unable to honor its commitments, it’s value may decline and/or could experience delays in the return of collateral or other assets held by the counterparty.

Before investing, investors should consider carefully the investment objectives, risks, charges and expenses of a mutual fund. This and other important information is contained in the prospectus and summary prospectus, which can be obtained from a financial advisor. Prospective investors should read the prospectus carefully before investing.

©2017 Eaton Vance Distributors, Inc. • Member FINRA/SIPC Two International Place, Boston, MA 02110 • 800.836.2414 • eatonvance.com

© Eaton Vance

Read more commentaries by Eaton Vance