Key Points

- Volatility has been plumbing historical depths, but it may not be reflecting investor complacency.

- Exchange traded products deserve some of the "credit" for low volatility.

- The Fed's plans for its balance sheet, more than rate hikes, could bring on spikes in volatility.

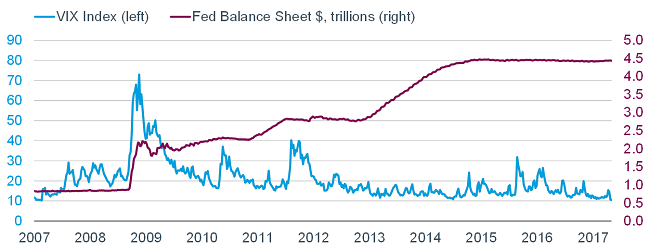

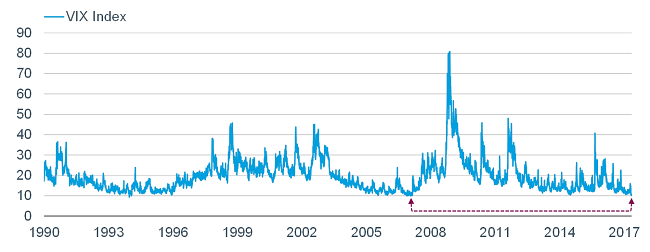

Much ink has been spilled lately by the financial press on the dramatic move down in market volatility as measured by the CBOE Volatility Index (VIX), to the lowest level since February 2007, as seen in the chart below.

Source: FactSet, as of May 5, 2017.

The extremely low level of volatility seems odd when in contrast to geopolitical anxieties, North Korea's saber rattling and U.S. fiscal policy machinations, among other uncertainties. Low volatility is often viewed as a sign of complacency and/or the calm before the storm. Indeed, there have been times when storms followed periods of suppressed volatility; but what may surprise folks is that larger-than-normal price moves can happen both on the upside and downside.

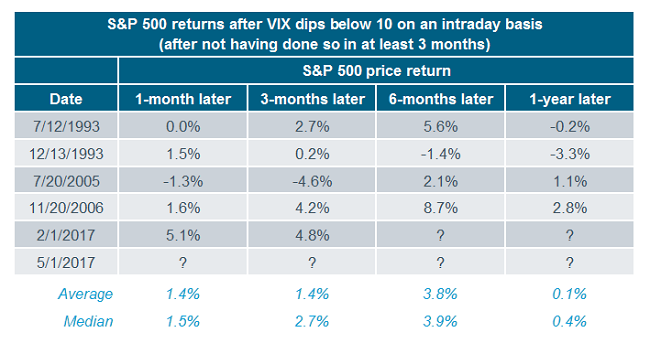

Looking at various time periods subsequent to historic dips into single-digit territory by the VIX, you can see that the stock market's performance was choppy—albeit positive in median terms—in the subsequent months; i.e., not indicative of a market top.

Source: Bespoke Investment Group (B.I.G.), Bloomberg, as of May 5, 2017.

Give credit to ETPs?

But there are some more nuanced reasons than complacency for today's suppressed volatility. Many traders are now suggesting that exchange-traded products (ETPs) linked to the VIX index have had a hand in the perceived distortion, according to Bloomberg (although it's difficult to prove that ETPs apply consistent pressure which pushes the VIX down). VIX ETPs have attracted over $700 million this year; which could exacerbate a selloff if volatility spikes.

In addition, investors may be relying less on S&P 500 index options for protective insurance on their portfolios. According to Bloomberg, investors are instead using alternative ways to manage risk in their holdings, such as options strategies that generate income as well as options on U.S. government bonds.