Since the election, markets have responded positively to a growing emphasis on fiscal policy over monetary policy. We share the view that an increased focus on fiscal policies is likely to be a long-term positive for the economy and markets. The stagnant economic conditions of recent years demonstrate the limits of monetary policy, while history has shown that pro-growth fiscal policies can provide tailwinds to move the economy into a stronger growth phase.

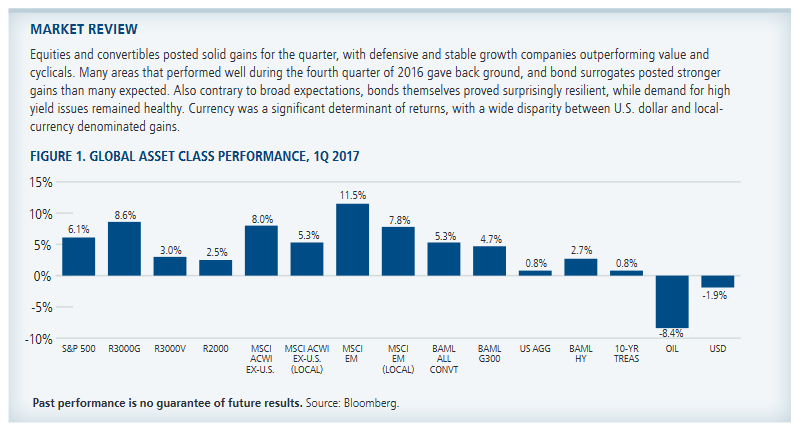

During the first quarter, investor sentiment was upbeat (see Market Review below). Markets cheered the prospect of more business-friendly fiscal policies in the U.S., while a weakening dollar provided a welcome tailwind around the world and particularly for emerging markets. We see a growing likelihood for sustained and balanced global GDP growth through 2018. The U.S. economy appears positioned for measured expansion, with growth picking up a bit of steam as the year progresses. Recovery is taking hold in Europe and a number of emerging market economies have moved from negative to positive growth.

While markets have risen briskly since the election, we do not believe the potent mix of tax reform and less regulation has been fully priced into equities. Even so, stocks may well move sideways until there is greater clarity around U.S. fiscal policy implementation and as economic data ebbs and flows. Markets will remain sensitive to political developments as the U.S. administration tries to propel its agenda and major elections approach in Europe. In this highly charged environment, we expect periods of market rotation and attention to valuations remains essential. Earnings expectations may be up overall, but in many cases this is a reflection of easy comparisons. We will be closely watching for the quality of earnings releases in the coming weeks.

U.S. Equities

Leading indicators point to a fundamentally improving economy, modest inflationary pressures have replaced deflationary concerns, and unemployment continues to fall. We expect the Federal Reserve to raise short-term rates at least two more times this year. This return to a more normal interest rate environment is a positive, given that increased rates would be a response to a healthier economy.

Still, it is important to acknowledge that many “hard” economic measures (such as government-reported retail sales and durable goods manufacturing) have been less robust than readings for “soft” economic measures (such as surveys of business and consumer confidence). We believe fiscal policy implementation can greatly influence how the soft data carries over to hard measures. If the administration can coalesce enough support to advance some of its pro-business policies, even conditional wins could help bridge the disconnect between soft and hard data, thereby catalyzing stronger growth and the animal spirits in the economy.

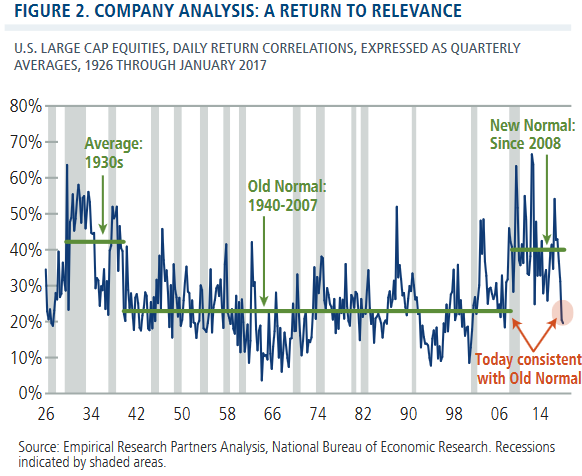

As deflation fears transition to reflation confidence, we see positive and pervasive implications for active stock picking. Since 2008, the “wall of worry” has been that low interest rates signal deflation risk, which is negative for earnings. Stocks have been dominated by these macro (or top-down) concerns rather than company fundamentals, which is shown in Figure 2. This chart highlights the high and unusual correlation across stocks post-2008, which is in contrast with much of the post-World War II period when these fears of systemic risk did not exist. It is striking that correlations have recently fallen into the pre-2008 range. This confirms our view that deflation fears are subsiding, with positive implications for active management. We think corporate fundamentals will trump macro fears as investors gain confidence in sustained and stable global GDP growth.

In this environment, there are growth opportunities beyond defensive growth sectors, including in consumer discretionary, industrials and financials. The consumer discretionary sector is highly diverse but has generally performed well on the strength of U.S. consumption. Here, we are emphasizing higher quality areas, while maintaining a highly selective approach to struggling areas, such as retail. In industrials, we are favoring companies that can benefit from recovering U.S. GDP growth and potential tax reforms (including railroads and machinery), as well as beneficiaries of increased defensive spending. In the financials sector, we see opportunities multiplying as regulatory pressures ease, the economy improves, and interest rates rise over time. We are overweight banks and have exposure to capital markets.

Our positioning also reflects our long-standing constructive view on technology, including high-quality names in the internet and software industries. Meanwhile, within health care, a difficult political setting is offset by specific opportunities. Contrary to common perception, many health care companies are no longer growth businesses in the absence of meaningful pricing power. This is a broad risk that is unlikely to resolve quickly as the central problem in the U.S. health care system remains excessive cost. However, a large part of this risk is reflected in stock valuations and the sector is highly diverse. Managed care and medical technology are two industries where we see attractive upside.

Global and International Strategies

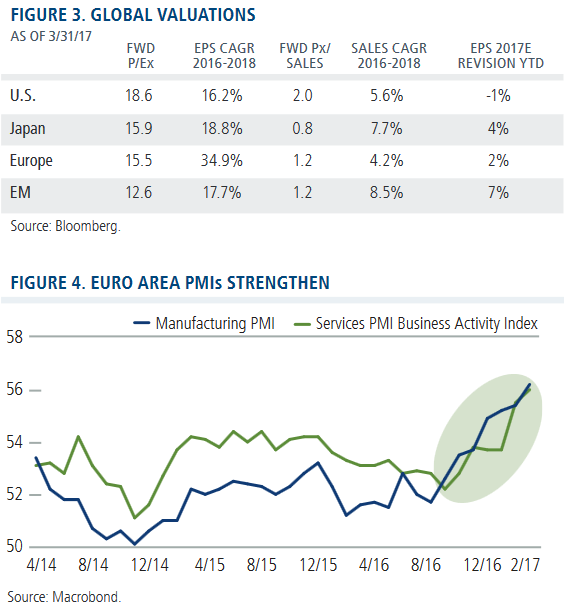

Fundamental economic improvements continue across Europe and the emerging markets. Although economic expansion in these markets may not be as robust as in the U.S. in absolute terms, the improvements mark more meaningful turning points. A weak dollar has been a boon to global economies, reducing deflationary forces and giving countries increased latitude to implement more accommodative monetary policy. We continue to identify many opportunities outside the U.S., supported by improving growth profiles, relative valuations, and positive earnings revisions (Figure 3).

In Europe, the ECB affirmed its intention to maintain highly accommodative monetary policy, and inflation has edged upward. PMIs have maintained a positive trajectory (Figure 4), and credit growth has improved on the back of increased credit demand, while corporate profitability and exports have strengthened. Although political risk continues—most notably, upcoming French and German election risk—populist sentiment has cooled somewhat. Absent a shock, we expect recovery will continue. Elsewhere in the developed markets, while Japan’s economy remains lackluster, we see continued bottom-up opportunities for exporters to capitalize on global expansion.

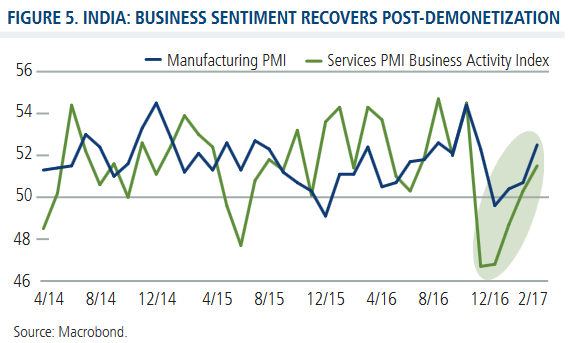

We are especially constructive on emerging markets. India remains one of our favorite growth stories. Indian equities struggled in 2016 due to a variety of factors, including the government’s surprise move to demonetize its currency last November. While this move roiled the markets, we viewed it as a surmountable near-term hurdle, and more importantly, as evidence of a longer-term reform agenda. As we discussed in a blog post, recent elections suggest that this agenda remains popular, and the country has lately delivered a stream of encouraging economic data, including improving consumer confidence, easing food inflation, and manufacturing survey data (Figure 5). We continue to identify opportunities in China, where recent economic data (including fixed-asset investment, housing activity, and PMIs) suggests growth resilience.

Convertible Securities

During the first quarter, global issuance was a very healthy $24.3 billion, the strongest quarter in nearly two years. U.S. issuers led, bringing $13.0 billion to market, followed by Europe at $7.6 billion. Encouragingly, nearly all U.S. issuance was in the form of convertible bonds. This stands in contrast to recent years when the U.S. market saw increasing mandatory convertible issuance.*

*Mandatory convertibles have enhanced equity characteristics and automatically convert to stock at a specified time. In contrast, the holder of a convertible bond has the right but not the obligation to convert at any time.

Given our expectations for sideways-moving equity markets and rising interest rates, we believe the case remains strong for actively managed convertible securities. With their blend of equity and fixed-income characteristics, convertibles offer upside equity participation, potential downside protection, and historically less sensitivity to rising rates than bonds.

Convertibles vary in their levels of equity and fixed-income sensitivity, and we continue to favor securities with balanced equity and fixed-income attributes. We maintain an emphasis on technology, where many companies are benefiting from long- term growth trends and cyclical tailwinds. We have also identified a number of consumer discretionary companies with attractive fundamentals and valuations, including bottom-up opportunities in media and autos. We are more selective in the defensive utilities and consumer staples sectors. We are also underweight financials, where convertible issues generally reflect a higher level of credit sensitivity than we would like in a rising interest rate environment.

Fixed Income

We expect that short-term rates are likely to settle in between 1.75% and 2.00% over the next four to five quarters, assuming inflation in the 2.0% to 2.5% range. (For more on this, read our recent blog post .) Meanwhile, as we have noted in previous commentary, parallel rate rises have been extremely rare, which is holding true today. In line with the expectations we shared in our January Outlook , long-term rates have been well behaved in the wake of the Fed’s most recent move, and we have seen a flattening curve. Presently, the market expects 10-year rates to be in the 3% range over the next couple of years, which seems reasonable based on the overall health of the U.S. economy and the highly accommodative policy coming from other global central banks.

In our view, a new dynamic has emerged between the Federal Reserve and the markets—one that creates opportunities for active managers. Whereas the Fed used to be far more sensitive to the market’s response to rate rises, the central bank has become more singularly focused on meeting its intended targets. Additionally, while we expect the Fed to continue providing clear guidance on its intentions, predicting the timing and magnitude of rate rises will become more difficult. This is because the data has become less cut-and-dry (for example, the discrepancy between hard and soft data we noted earlier). An environment of less precise Fed guidance and less consensus opens the door wider for active managers.

Conclusion

We are in a world of conflicting agendas, within the U.S., as well as among global economies and central banks. These crosscurrents will continue to challenge investors, but slow and stable global GDP growth and increased fiscal policy support global opportunities. Sensational headlines are likely to continue, but investors are generally not rewarded for chasing headlines. Rather, we believe this is an environment in which active investing and a focus on downside risk management will be rewarded, and therefore, one in which we believe we can thrive.

--

Indexes are unmanaged, not available for direct investment and do not include fees and expenses. The U.S. Dollar Index measures the value of the U.S. dollar relative to a basket of foreign currencies, including Euro Area, Canada, Japan, United Kingdom, Switzerland, Australia, and Sweden. The Russell 3000 Growth Index and Russell 3000 Value Index measure U.S. growth and value equities, respectively. The Russell 2000 Index measures U.S. small cap stock performance. The S&P 500 Index is considered generally representative of the U.S. equity market. The MSCI All Country ex U.S. Index represents the performance of global equities, excluding the U.S. The MSCI Emerging Markets Index is a measure of the performance of emerging market equities. The BofA Merrill Lynch U.S. High Yield Index is an unmanaged index of U.S. high yield debt securities. The BofA Merrill Lynch All U.S. Convertible Index (VXA0) is a measure of the U.S. convertible market. The BofA Merrill Lynch G300 Index measures the performance of 300 global convertibles. Oil is represented by current pipeline export quality Brent blend. The Bloomberg Barclays U.S. Aggregate Bond Index is a measure of the broad U.S. bond market.

Purchasing Managers Indexes measure manufacturing sector strength. Quantitative easing refers to central bank bond buying activities. Earnings per share (EPS) is a company’s profit divided by its number of common outstanding shares. Price- to-earnings ratio (P/E) is a valuation ratio of a company’s current share price compared to its per-share earnings; forward P/Es are based on forecasted earnings. CAGR , or compounded annual growth rate measures year-over-year growth. Price-to-sales ratio measures a company’s stock price versus its revenues.

Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. The views and strategies described may not be suitable for all investors. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations.

Calamos Investments LLC

2020 Calamos Court | Naperville, IL 60563-2787 800.582.6959 | www.calamos.com | [email protected]

Calamos Investments LLP 62 Threadneedle Street | London EC2R 8HP Tel: +44 (0)20 3744 7010 | www.calamos.com/global

©2017 Calamos Investments LLC. All Rights Reserved. Calamos ® and Calamos Investments ® are registered trademarks of Calamos Investments LLC.

OUTLKCOM 18562 0417O

© Calamos Investments

Read more commentaries by Calamos Investments