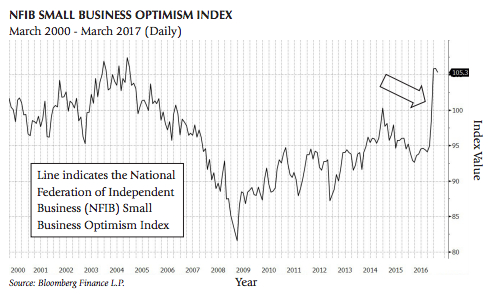

Below is the single most interesting chart we’ve seen in the last quarter.

It is a plot of the National Federation of Independent Business (NFIB) Small Business Optimism Index since March 2000. The NFIB conducts monthly surveys of its members in order to better understand the environment in which small businesses are operating. The way we interpret the chart is that small businesses are MUCH more optimistic about their future post-election than they were pre-election (the arrow is there to highlight that move for you). If that increased optimism results in greater hiring and spending on capital goods, we believe the economy can grow significantly faster than it has managed to do the last few years. In part we think the chart validates our assertion that increased regulations and costs have been limiting business growth— and the promise to reduce them has small businesses more optimistic than they’ve been in years. The questions now are “Will our politicians deliver on their promises?” and “Which companies will benefit and which will be hurt by the changes?” That’s what we are paying a lot of attention to right now.

While potential U.S. policy changes are the most important things going on, they aren’t the only things to keep an eye on. A quick update on some pertinent developments: the U.S. Federal Reserve raised the Federal Funds Rate by .25% in March. This is the third rate hike by the Fed since the ’09 recession and was largely expected. The Fed has stated that they may continue to raise short-term rates this year as the country is near their employment and inflation goals. At this point we don’t expect a rapid run up in inflation nor do we see rising interest rates triggering a recession. Either or both of those things may happen in the future, but we don’t see signs that they are imminent.

U.S. companies in the aggregate in the 4th quarter of 2016 reported an increase in both earnings and revenues—the first time we’ve seen that in five quarters, led by improvements in the energy sector where higher crude oil prices (now in the vicinity of $50 per barrel) have led to increased drilling activity. The strong dollar we saw late last year has weakened a little, easing pressure on the earnings of our exporters. Long-term interest rates have also declined a bit since last year, keeping the cost of rolling over debt low for those companies that need to do so. From a consumer perspective, rising short-term rates will provide savers a marginally better return on savings accounts, money markets, and short-term certificates of deposit but inflation adjusted returns on fixed income products are still pretty poor, as we’ve been pointing out for a long time now. On the consumer borrowing side, rates are pretty cheap with 30 year mortgage rates at about 4% — they’ve been as high as 4.2% and as low as 3.8% over the last year.

Outside of the U.S., elections in France and Germany later this year have the potential to disrupt the Eurozone. Belgian elections in March resulted in a re-election of the status quo, we’ll have to see what develops in France and Germany. The European Central Bank (ECB) continues to buy bonds, keeping interest rates low in Europe and, we believe, helping to keep interest rates low in the U.S. That program is scheduled to end in December, it isn’t clear if the ECB will let it expire or extend it once again. On a positive note, real Gross Domestic Product (GDP) growth in Europe the last quarter was 1.9%, much improved over a year ago and on par with U.S. GDP growth.

The U.S. stock markets remain on the expensive side, as they’ve been for some time now. In the absence of signs of an approaching recession or financial crisis we have stuck to our knitting, selling holdings that have reached full value and reinvesting the proceeds in companies we believe are selling for less than we think they are worth—though good companies selling cheaply are few and far between these days.

Until next quarter…

Ron Muhlenkamp and Jeff Muhlenkamp

The comments made by Ron and Jeff Muhlenkamp in this commentary are opinions and are not intended to be investment advice or a forecast of future events.

Glossary

Federal Funds Rate is the interest rate at which depository institutions lend balances at the Federal Reserve to other depository institutions overnight. It is the interest rate banks charge each other for loans.

Federal Reserve Board (informally referred to as “the Fed”), is the central banking system of the United States, created in 1913 by the Federal Reserve Act. The main tasks of the Fed are to supervise and regulate banks, implement monetary policy by buying and selling U.S. Treasury bonds, and steer interest rates.

Gross Domestic Product (GDP) is the total market value of all goods and services produced within a country in a given period of time (usually a calendar year).

Copyright ©2017 Muhlenkamp & Company, Inc. All Rights Reserved

© Muhlenkamp & Company

Read more commentaries by Muhlenkamp & Company