Proposed US tax cuts—if they happen—would be a nice boon for corporate bottom lines. But for most companies, the boost to underlying earnings power would likely be fleeting. To find tax-reform winners, look for the exceptions.

The stocks of potential tax-reform beneficiaries have surged since the election of Donald Trump last November. The reasoning is that lower tax rates will drive higher net income and cash flows, and support higher stock prices, especially those of companies generating a lot of US income.

It remains to be seen what, if anything, gets done. And, indeed, the tax-relief rally has faded along with the prospects for new legislation any time soon. But, let’s assume that promises eventually become reality. Under that scenario, we think the most critical follow-up question for investors is: Will lower taxes improve the fundamental value of American businesses?

For most companies, we’d say no—certainly not over the long term, and probably not even over the nearer term. Why? Because a structural, step-change in returns on capital would require a dramatic—and unlikely—change in competitive behavior. We expect the longer-term benefits of lower taxes to be highly company-specific and to largely depend on the robustness of a company’s market positioning.

THE LAWS OF THE JUNGLE STILL RULE

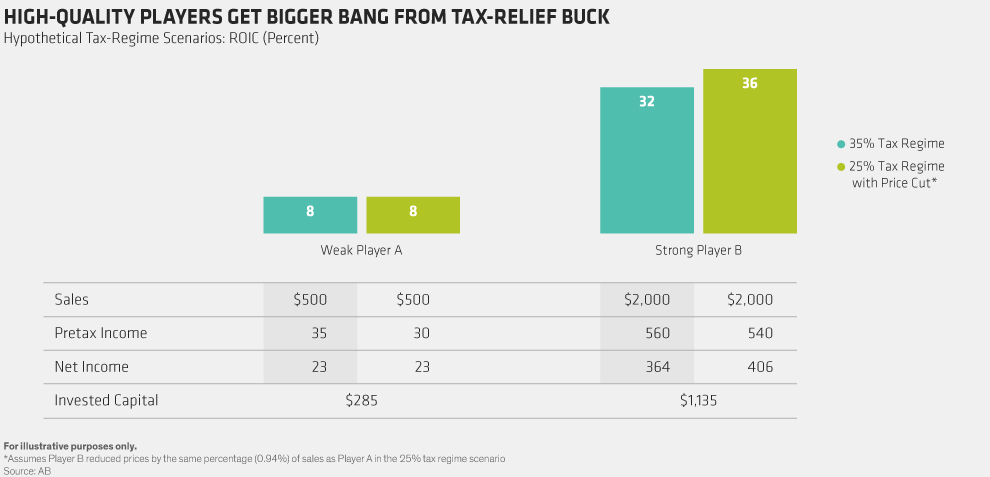

On balance, the return on invested capital (ROIC) for most industries tends to be at or slightly above the cost of funding. That means these businesses are already quite competitive. Because a tax cut is an external factor, not specific to any one firm, we’d argue that, over time, many companies would choose to pass along the margin pickup from a lower tax rate to consumers, mostly by reducing selling prices.

That calculus differs for the higher-quality, higher-return companies in an industry, however. These businesses generally have strong competitive moats or advantages—such as a well-defended network effect, a difficult-to-replicate service, or a beloved brand—that enable them to maintain high and predictable profitability. Those advantages would likely endure, especially if the only change in the overall business environment was a tax cut. Because these companies typically enjoy strong pricing power, the stronger operators would likely retain most of the tax windfall rather than pass it onto customers.

THE STRONG GET STRONGER

In the end, despite modest potential pricing pressure, we’d expect the after-tax returns of the high-quality, cost-efficient companies to significantly surpass those of the low-quality, inefficient companies. What’s more, we think the bigger the ROIC gap between the strongest and weakest competitors in an industry, the greater the relative benefit of a tax cut to the strongest players.