These days some wonder about a potential recession, as we’re eight years into a long U.S. economic expansion and the S&P 500Ò index keeps making record highs (and getting more expensive), up 14.25% on a year-to-date basis as of March 30, 20171. Such growth is just one reason that a good read on the U.S. economy is crucial for portfolio management.

Economic indicators to watch

As such, our team of investment strategists regularly evaluates recession risk with both confirming indicators and contrarian indicators. With such research, as our latest Global Market Outlook Q2 Update notes, we’ve concluded that a near-term U.S. recession is unlikely, but we should monitor this aging cycle of market growth.

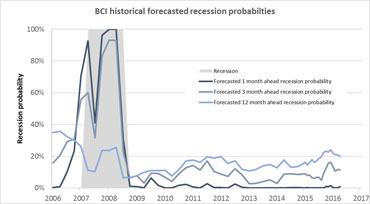

The Business Cycle Index (BCI) tracks the health of the U.S. economy by looking at confirming indicators like job growth, consumer spending, and measures of financial risk. The index estimates the probability of recession in the next 12 months is only 20%.2

Recession risks have been gradually building over the last few years but declined a bit more recently. I believe that the recent decrease in recession probability is driven by a steepening yield curve3 and lower credit spreads4—indicators that reflect potential stronger future growth expectations and likely lower financial risk for both the economy and investors.

Why optimism can matter

In my view, this optimism around the economy is echoed through a range of business, consumer, and CEO surveys. These data points show increased confidence in the U.S. economy. However, it may be difficult to reduce U.S. recession probabilities to the levels we saw two years ago, when the BCI pegged the average 12-month recession probability under 15%, given we’ve already had such a long economic expansion. The pace of job growth is still steady, but we believe it is likely to moderate as we push towards full employment.

Source: The Business Cycle Index. April 7, 2017.

Russell Investments strategists also check for signs of an overheating economy with our internal research. This research combines data from the labor market, business investment, household debt and business borrowing, among others. This is how we came to believe that the unemployment rate has dropped below its sustainable level, suggesting that the labor market may be overheating.

History tells us that when unemployment is very low, employers are often forced to bid up wages to attract a scarce pool of qualified workers, which can gradually cut into corporate profits. Firms often respond to weak profits by cutting investment and hiring, hurting consumer spending, which can feed into a negative spiral, and start the onset of a recession. In the last nine economic cycles, looking at the BCI, it historically took an average of 2.5 years from the time the unemployment gap closed until the next recession.

Our view on near-term U.S. recession probability

Overall, our team of investment strategists thinks that the U.S. economy is still on a path of moderate growth with low probability of recession—see the latest Global Market Outlook to learn more on our U.S. economic outlook.

In our view, short-term (one to 12 month) recession probabilities fell in the last quarter, driven by strong economic data. We believe that medium-term (two - three year) recession risks are building as the U.S. cycle ages. We believe investors need to consider a multi-asset approach to help maintain a balanced risk portfolio and look for opportunities to buy the dips and sell the rallies.

Disclosures

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page.

These macroeconomic forecasts do not constitute a projection of the stock market or of any specific investment.

Forecasting is inherently uncertain and may be incorrect. It is not representative of a projection of the stock market, or of any specific investment. Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

Investing involves risk and principal loss is possible.

Past performance does not guarantee future performance.

This material is not an offer, solicitation or recommendation to purchase any security. Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type.

The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional. The information, analysis and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual entity.

Please remember that all investments carry some level of risk. Although steps can be taken to help reduce risk it cannot be completely removed. They do no not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns. They do no not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

The S&P 500®, or the Standard & Poor’s 500, is a stock market index based on the market capitalizations of 500 large companies having common stock listed on the NYSE or NASDAQ.

Russell Investments’ ownership is composed of a majority stake held by funds managed by TA Associates with minority stakes held by funds managed by Reverence Capital Partners and Russell Investments’ management.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the “FTSE RUSSELL” brand.

Copyright © Russell Investments 2017. All rights reserved.

This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an “as is” basis without warranty.

UNI - 11033

1 Yahoo Finance: S&P® 500 Index Historical Chart, 1YR view as of March 30, 2017.

2 Source: The Business Cycle Index (BCI), as of March 30, 2017. The Business Cycle Index (BCI) forecasts the strength of economic expansion or recession in the coming months, along with forecasts for other prominent economic measures.

3 The steepening of the yield curve is a result of changing yields among comparable bonds with different maturities.

4 Credit spreads is an indicator of default risk and a proxy for general financial risk/stress. Credit spread is the difference in yield between a risky asset (ex: corporate bonds rated at BAA) and a safe asset (ex: US government bonds). When the yield for the risky asset is very high compared to the yield for a safe asset, it means that investors think the risky asset is extra risky, and want to be compensated with a higher yield to hold this extra risky asset. An investor might think this asset is extra risky because he/she thinks the corporation may default on the loan.