Though the “Trump bump” helped, the year-old winning streak in smaller stocks owes far more to the spirited US economy. This rally has firepower, but we’d be choosy in riding the next leg higher.

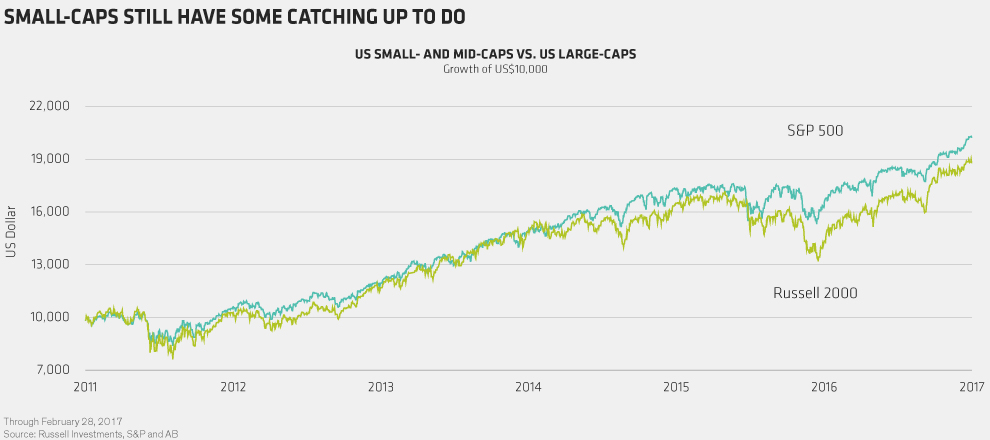

US small-caps have been on a tear for the past year. The small- and mid-cap Russell 2500 Index rocketed 17.6% in 2016, soundly beating the S&P 500 Index’s 12% gain. Yet, despite erasing several years of sluggish performance, small stocks still haven’t fully caught up with the large-cap index (Display). In the first quarter of 2017, the rally stalled, with the Russell 2500 up 3.8%, roughly two-thirds the gains of the broader market.

As we see it, the US small-cap comeback is really a US recovery story. The expansion that began in 2009 continues to gain traction, with unemployment at historic lows and wage growth perking up. And, though policy details have yet to come, the Trump administration’s proposals to cut taxes and relax regulations have raised expectations for faster US growth. This backdrop should benefit smaller companies, which are more domestically oriented, pay higher taxes and face disproportionately stiffer regulatory burdens than do the larger firms.

NOT A BLANKET CALL

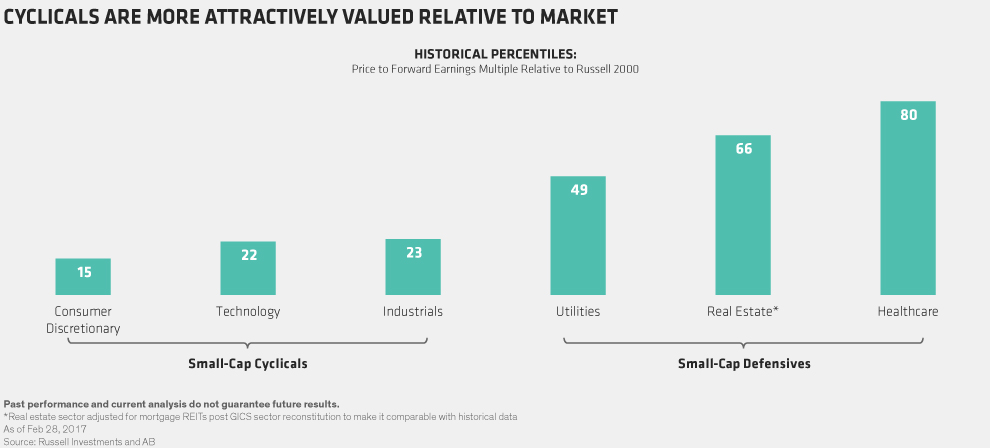

Even so, while we remain positive on small stocks, we believe investors should be selective in how they get exposure. The macro environment and Trump’s policy proposals will affect different companies and industries in different ways. For example, rising rates are good for bank shares, but bad for interest-rate-sensitive REITs and utilities. New trade barriers may help US-centric firms that compete with foreign imports, but they could hurt small businesses that supply large multinationals facing higher import costs. And after the run-up of the past year, valuations matter. Today’s heightened geopolitical, monetary and policy uncertainties call for a hands-on, nimble strategy, in our view.