KEY TAKEAWAYS:

- This week we check in on some so-called Trump trades, including small caps, financials, and industrials.

- Recent underperformance of these areas likely reflects some loss of confidence in the Trump agenda.

- Small caps and financials may have enough going for them that recent weakness may be an opportunity, even with a scaled-back policy path.

- Industrials may need more help from the macroeconomic environment should policy disappoint.

Checking in on some “Trump trades.” The election outcome and resulting expectations for fiscal policy have caused several shifts in market leadership toward areas most sensitive to these policies. Policy is not the only factor to consider when evaluating these investments, but it is a very important one. Here we discuss some of these so-called “Trump trades,” including small cap stocks and the financials and industrials sectors.

SMALL CAPS

Small cap stocks may be the most sensitive to the Trump policy agenda. Smaller companies would generally benefit more from a lower corporate tax rate than their larger cap counterparts because of their greater proportion of domestic revenue and resulting higher tax rates (global multinationals earn more profits overseas in low tax countries). The median corporate tax rate for the companies in the small cap Russell 2000 is 4-5% higher than that of the large cap S&P 500.

Small caps’ more domestic focus means they are not as impacted by potential protectionist trade policies. Many smaller, U.S.-focused companies stand to benefit from the Trump administration’s efforts to bring overseas production back to the U.S. Small caps are also more credit sensitive than their larger counterparts, relying more on bank loans than larger companies that tend to have stronger balance sheets, and therefore generally benefit more from financial deregulation.

One Trump policy that is likely to benefit larger cap companies more is repatriation. Should companies be allowed to repatriate overseas cash at a low tax rate, larger multi-nationals with huge cash hoards overseas will benefit the most. However, some of that extra cash may be used for acquisitions, potentially benefiting smaller cap companies.

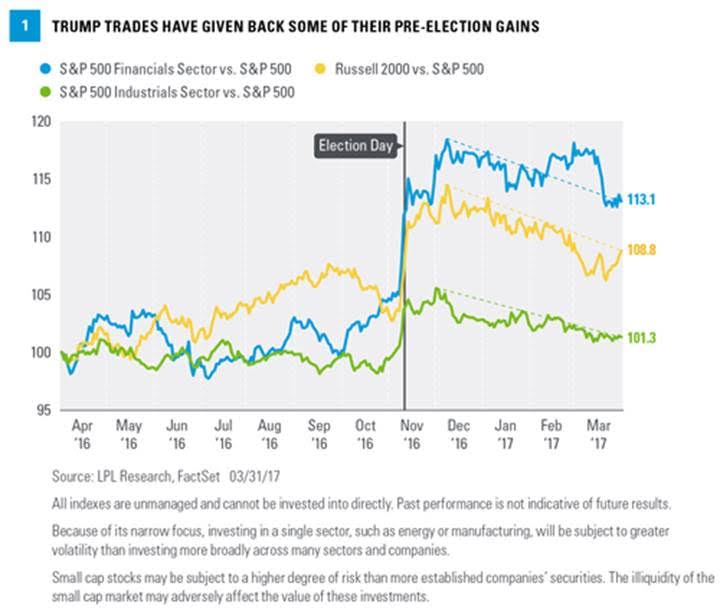

Small caps have underperformed in recent months [Figure 1], begging the question of whether the relative weakness reflects dampened enthusiasm for the Trump agenda (our sense is it does), and whether the weakness presents a buying opportunity. We continue to believe corporate tax reform will pass, though it will likely be scaled down from earlier proposals from Trump and congressional Republicans and it may not get done until early 2018. Still, that potential boost along with the improving underlying health of the economy and credit markets are enough for us to suggest this latest dip in small caps relative to large is more likely to present a potential opportunity than the start of a period of prolonged weakness.

FINANCIALS

The financials sector has fallen into the Trump trade category for two reasons. First, the Trump agenda has been viewed as likely to put upward pressure on interest rates and steepen the yield curve. The yield curve—the difference between short-term and longer-term interest rates—is a key determinant of bank profitability. In addition, higher interest rates lift returns on assets on bank and brokerage company balance sheets (the same way they help savers).

Second, Trump is a big proponent of financial deregulation and has already taken steps to ease the regulatory burden on financial institutions through executive orders. Deregulation offers the potential benefit of freeing up more capital for financial institutions to lend, supporting loan growth, and can also reduce legal and compliance costs. Deregulation may also provide additional revenue opportunities that may not have been available under an Obama or Clinton administration. For example, the Volcker rule, which prohibits banks from engaging in proprietary trading and restricts hedge fund and private equity investments, may be only loosely enforced or watered down to allow banks to do more with their capital.

Like small caps, financials have more going for them than just a potential policy boost. The sector, one of the more domestically focused, is benefiting from underlying recent improvement in the U.S. economy. Inflation has picked up and is starting to—intermittently—put some upward pressure on interest rates. The Federal Reserve (Fed) raised its target interest rate (the federal funds rate) twice in the past four months with little consideration for prospective pro-growth policies (although the strong stock market may be playing a role in Fed psychology). Healthy credit markets reflect oil’s rebound, while financials enjoyed a very strong fourth quarter earnings season with little help from Washington, D.C.

Even if only a scaled-down version of the Trump agenda is implemented, we believe the underlying improvement in the U.S. economy and potential for higher interest rates are enough for at least a moderately positive view of financials. Add to that the potential upside of corporate tax reform (the sector’s domestic focus may result in an above-average benefit from a reduced corporate tax rate), deregulation, and still reasonable valuations, and we would view financials’ recent underperformance, also shown in Figure 1, as a potential opportunity.

INDUSTRIALS

Trump’s plans to increase spending on infrastructure and defense have made the industrials sector a popular Trump trade. Trump has proposed a massive $1 trillion spending plan over 10 years ($100 billion per year) through public-private partnerships; numbers we believe are very unlikely to even be approached. We have expected the deficit hawks in Congress to significantly reduce, or eliminate, the potential for a federally funded infrastructure spending program, while the availability of large and profitable projects the private sector would take up is limited. On top of that, given the Republicans’ inability to get an Affordable Care Act (ACA) replacement to the House floor for a vote on March 24, 2017, getting a significant spending bill through Congress is likely to be very difficult.

Recent headlines have suggested a possible pairing of corporate tax reform and infrastructure spending. Though possible, we view this path as unlikely. Such a deal would likely require adding to the deficit (a problem for the Freedom Caucus in the House) or support from moderate Democrats, which is tough to see even though Democrats are generally pro-infrastructure. In this scenario, corporate tax reform would be particularly difficult to achieve and we see infrastructure getting pushed out to 2018.

Turning to defense, Trump has proposed a $54 billion increase in the defense budget, which would put defense spending at about 10% above fiscal 2015 levels. Although we do not know what budget increase will ultimately be passed (it’s probably smaller), it is clear that defense spending is a priority of this administration and is likely to rise. Global defense spending growth may also pick up from its marginal pace of recent years as a result of Trump’s call for other nations to shoulder more of the financial load for their own protection and global interests.

Of these three so-called Trump trades, the foundation for this one may be weakest. Although we expect a pickup in capital spending, partly due to expected policy support, it has been lackluster in the U.S. in recent years. The sector’s valuations are above average and the risks to the sector from trade protectionism, lower oil prices, and a strong U.S. dollar are concerning.

Industrials’ relatively small post-election rally [Figure 1] leaves less to give back should investors become more skeptical in the Trump agenda. However, we believe the sector may need help from stronger global growth, the long-awaited pickup in capital spending, and higher oil prices to produce strong performance in 2017. It may come, but several things have to fall into place.

CONCLUSION

Small caps, financials, and industrials are each very sensitive to Washington’s policies, so how much the Trump administration can get done will go a long way toward determining if these investments perform well over the balance of the year. Recent underperformance of each of these areas likely reflects some loss of confidence in the Trump agenda, but small caps and financials have enough going for them, in our view, that we see recent weakness as potential opportunities, even with a scaled back policy path. Industrials, on the other hand, may need more help from the macroeconomic environment should the policy path disappoint.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market.

Small cap stocks may be subject to a higher degree of risk than more established companies' securities. The illiquidity of the small cap market may adversely affect the value of these investments.

All investing involves risk including loss of principal.

Because of its narrow focus, investing in a single sector, such as energy or manufacturing, will be subject to greater volatility than investing more broadly across many sectors and companies.

INDEX DEFINITIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Russell 2000 Index measures the performance of the small cap segment of the U.S. equity universe. The Russell 2000 Index is a subset of the Russell 3000 Index representing approximately 10% of the total market capitalization of that index.

The information contained in this email message is being transmitted to and is intended for the use of only the individual(s) to whom it is addressed. If the reader of this message is not the intended recipient, you are hereby advised that any dissemination, distribution, or copying of this message is strictly prohibited. If you have received this message in error, please immediately delete.

© LPL Financial

Read more commentaries by LPL Financial