Despite uncertainty about global politics and policy, stock markets are soaring and volatility is low. Does this mean it’s time for investors to double down on growth-oriented assets? Not necessarily.

For many risk-managed strategies, a multi-month rally like the recent one in US equities, coupled with low volatility, is an unambiguous signal to lean in. But here’s the problem: it’s just one signal. To be effective, risk management should take its cues from multiple market signals.

Don’t get us wrong: With the US economy strengthening and global growth gaining traction, equities definitely belong in investors’ portfolios. But high stock valuations and policy uncertainty in the US and elevated political risk in Europe suggest that now isn’t the time to ramp up your existing equity exposure.

TOO MUCH OF A GOOD THING?

The current market environment is a case in point. Yes, risk signals based on the volatility implied by the pricing of stock options, credit spreads and other indicators are declining. And most of the time falling risk leads to market rallies and higher returns. But not always.

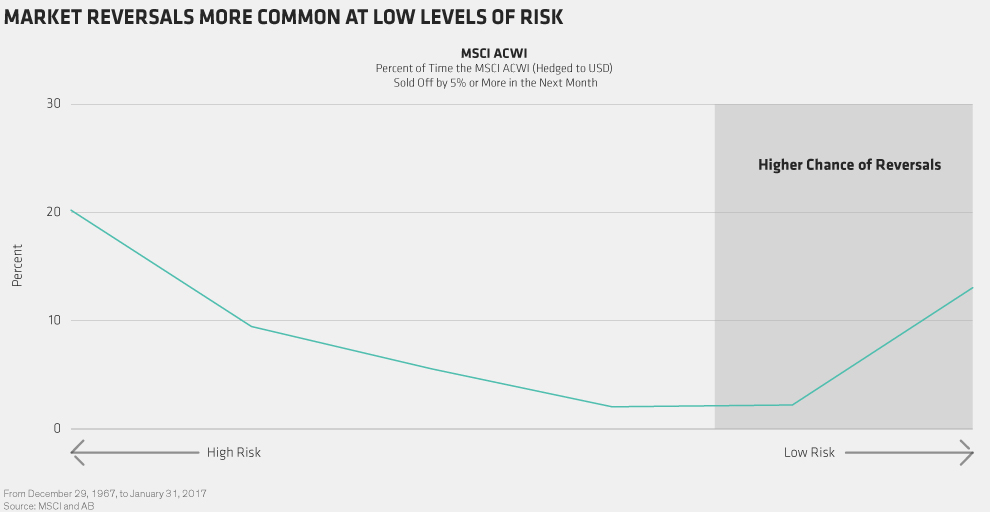

Looking back over the past five decades, we found that when risk metrics fell below a certain point, the probability of a monthly decline of 5% or more in the MSCI ACWI increased dramatically (Display).

In early 2006, for example, global stock markets were rising steadily. But in May, the rally turned into an extended sell-off. The reason: fear that central banks’ attempt to quell inflation with higher interest rates would choke off growth. The move caught many off guard because risk indicators and volatility were low at the time.