The stock market started off this year in a similar fashion to how it ended last year, in rally mode. The difference this year is that international stocks have been participating as well. If this international outperformance were to continue, it would be in stark contrast to the last 5 years when US stocks more than tripled the return of International stocks. The last three years of the US stock market rally has been even more fascinating because one key ingredient has been completely absent…earnings.

It’s Me, Earnings! Don’t Forget About Me!

Over the last three years, investors have seen the unemployment rate fall from 6.7% to 4.7%² and have seen the average duration of unemployment fall from 36 weeks to 25 weeks³. They have also seen the S&P 500 go from 1,831 at the start of 2014 to over 2,350 today. However, what they have not seen is an increase in S&P 500 company earnings. In fact, full year earnings for 2016 were 5% below 2013.4

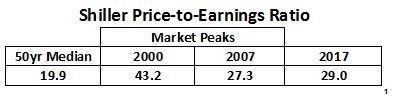

It appears what has driven US stocks for the past three years has not been company fundamentals, but investor optimism itself. This has resulted in valuations of US stocks surpassing levels prior to the 2008 Financial Crisis.

There is no way to know how much investors will be willing to pay or how far they are willing to drive up US valuations. Fortunately, there are other places to look for opportunities.

What investors need to remember is that risk is not a constant factor. The price investors pay for an asset, in relation to its fundamentals, affects the risk level of that investment.

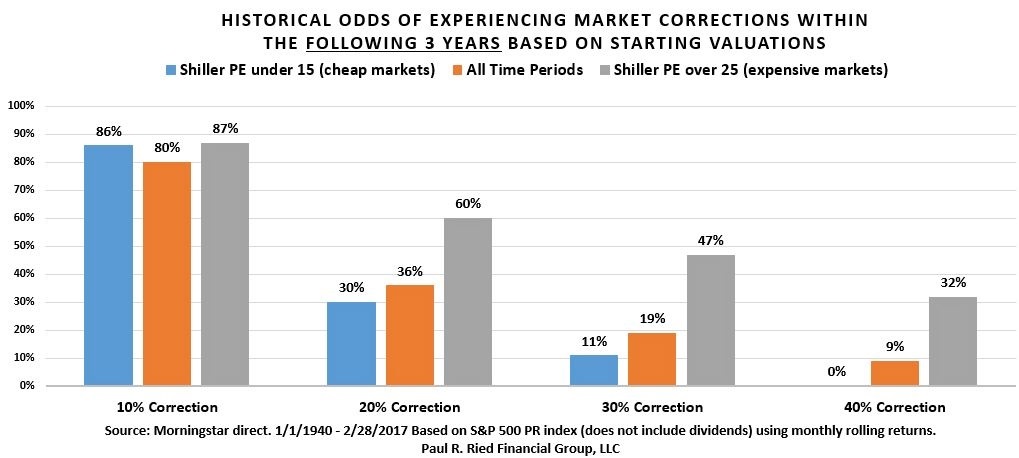

The chart below shows the historical odds of experiencing market corrections of varying degrees within a three-year period. In addition, it shows how those odds are affected based on the starting valuation.

While the chances of experiencing rather mild corrections of 10% are similar regardless of starting valuation, the odds of experiencing much bigger losses increase significantly during periods when markets are expensive. As the chart illustrates, the odds of a 30% correction go from about 1-in-9 during cheap markets to nearly a 1-in-2 chance during expensive markets.

Patiently Waiting

So far, market participants have been willing to push aside the fact that the new administration hasn’t provided many more details or time tables regarding corporate tax reform, individual tax reform or infrastructure spending…. despite these being three “market friendly” policies investors were most optimistic about.

Instead, it appears they have chosen to confront some of the more “market unfriendly” measures up front. These include immigration and trade policies. In addition, they have attempted to address healthcare. However, considering the rocky road encountered on these measures, it may not be a bad thing for markets that they addressed these first.

Little Room for Error

With US Stocks priced for perfection, it leaves little room for underwhelming results when it comes to earnings or policy implementation (currently investor expectations for earnings are directly tied to policy implementation).

Furthermore, it is possible that investors are factoring in the positive side of the tax policies (including lower tax rates and tax reductions for the repatriation of cash held overseas) but may be downplaying the negative effects of the border tax or elimination of interest deductions which may be required to make the policies feasible.

Trip Planning & Your Portfolio

There are some common-sense concepts involved in planning a trip that also speak to investments. Unfortunately, investors don’t tend to apply them in the same common-sense fashion.

For instance, when deciding between hotels it’s unlikely you would only compare things like location and amenities without ever taking price into consideration. However, oftentimes investors not only ignore pricing but they are also willing to pay peak season prices despite the fact they are going during hurricane season….As long as it’s sunny out today! That is in effect what investors are doing when they want to increase their allocation to US stocks at peak valuations.

Similarly, when planning a trip, you pack your bag based on your plans and final destination…with an outfit or two for backup. Unfortunately, too many investors just load up with swimsuits and hope for the best… sometimes forgetting it’s not even a beach vacation!

It is our goal that your investment experience go as smoothly as possible with the least number of surprises (because this is not the kind of trip where you want surprises). That is why we have incorporated numerous local tour-guides (active fund managers) to help navigate every aspect of your journey.

¹- http://www.econ.yale.edu/~shiller/data.htm 2000 peak (3/2000) 2007 peak (10/2007) 2017 (3/26/2017)

² - https://fred.stlouisfed.org/series/UNRATE Feb 2014 – Feb 2017

³ - https://fred.stlouisfed.org/series/UEMPMEAN March 2014 – March 2017

4 - http://us.spindices.com/documents/additional-material/sp-500-eps-est.xlsx As Reported Earnings

Opinions expressed are not intended as investment advice or to predict future performance. All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. All economic and performance information is historical and not indicative of future results. The S&P 500 is an unmanaged group of securities considered to be representative of the stock market in general. You cannot invest directly in an index. Past performance does not guarantee future results.

© Paul R. Ried Financial Group

Read more commentaries by Paul R. Ried Financial Group