Children eventually reach an age when they outgrow the need or desire for an elaborately staged birthday party. In the case of a certain bull born back in March 2009, that age appears to be eight. Although we write this a few days in advance of the “special day” (March 9th), the hoopla has certainly fallen short of that which surrounded birthdays #3 through #7 (or at least our recollection of it). Could it be that complacency has set in—that bull market birthdays have become… well… a birthright? Based on the flood of assets into passively managed stock mutual funds, our answer would be yes.

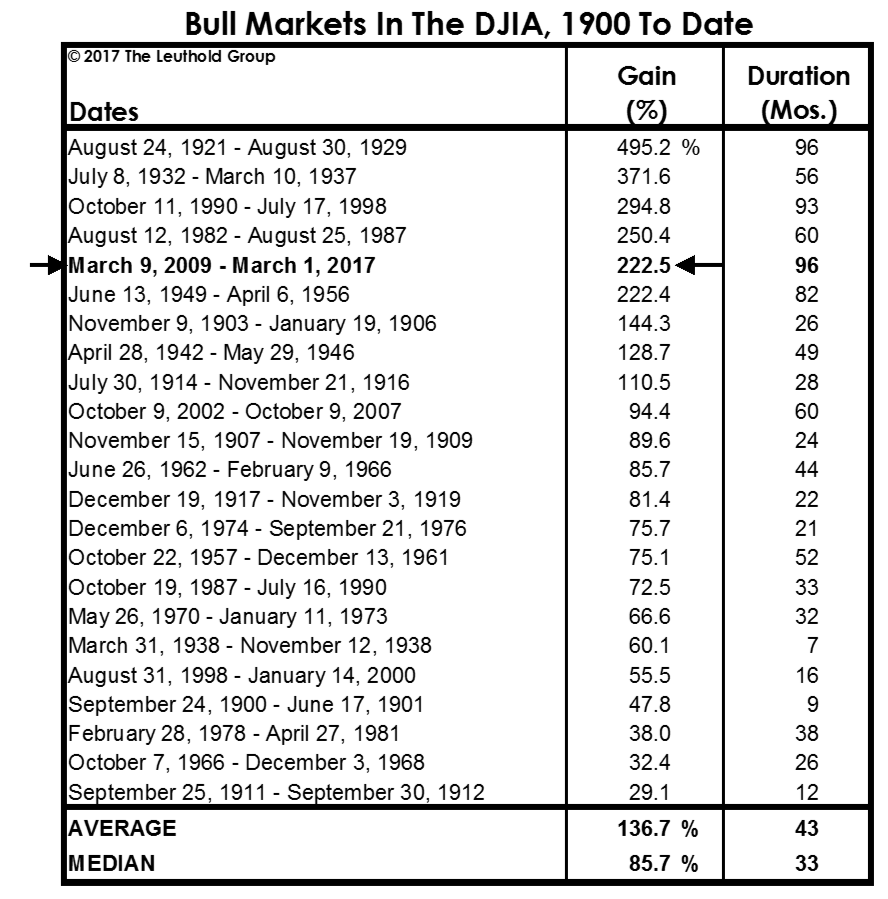

Our underestimation of the current bull market started even before it commenced, when we foolishly built Chart 1 to accommodate cyclical bull markets lasting up to a maximum of 8 1/2 years. (There we go again, relying on history to gauge the present.) While the horizontal boundary of the chart might be violated later in 2017, the vertical boundary—representing a DJIA bull market price gain of 500%—looks safe for now.

Thanks to the market surge on March 1st, the Dow’s cumulative bull market price gain of 222.5% now ranks fifth among the 23 cyclical bull markets since 1900 (Table). And, any new DJIA high after March 15th will put the current bull in the top spot as far as longevity, dethroning the 1921-1929 bull (which lasted 96 months and six days).

This bull market has overcome seemingly any challenge proposed in these pages, so we’ll put forward a couple more. To eclipse the powerful 1982-87 cyclical bull, the DJIA would need to close above 22,941.64; a close north of 25,849.29 would eclipse its 1990-1998 gain. These numbers might seem a stretch after an 18-year period in which the DJIA traded mostly between 10,000 and 20,000, but both are achievable in a true melt-up scenario.

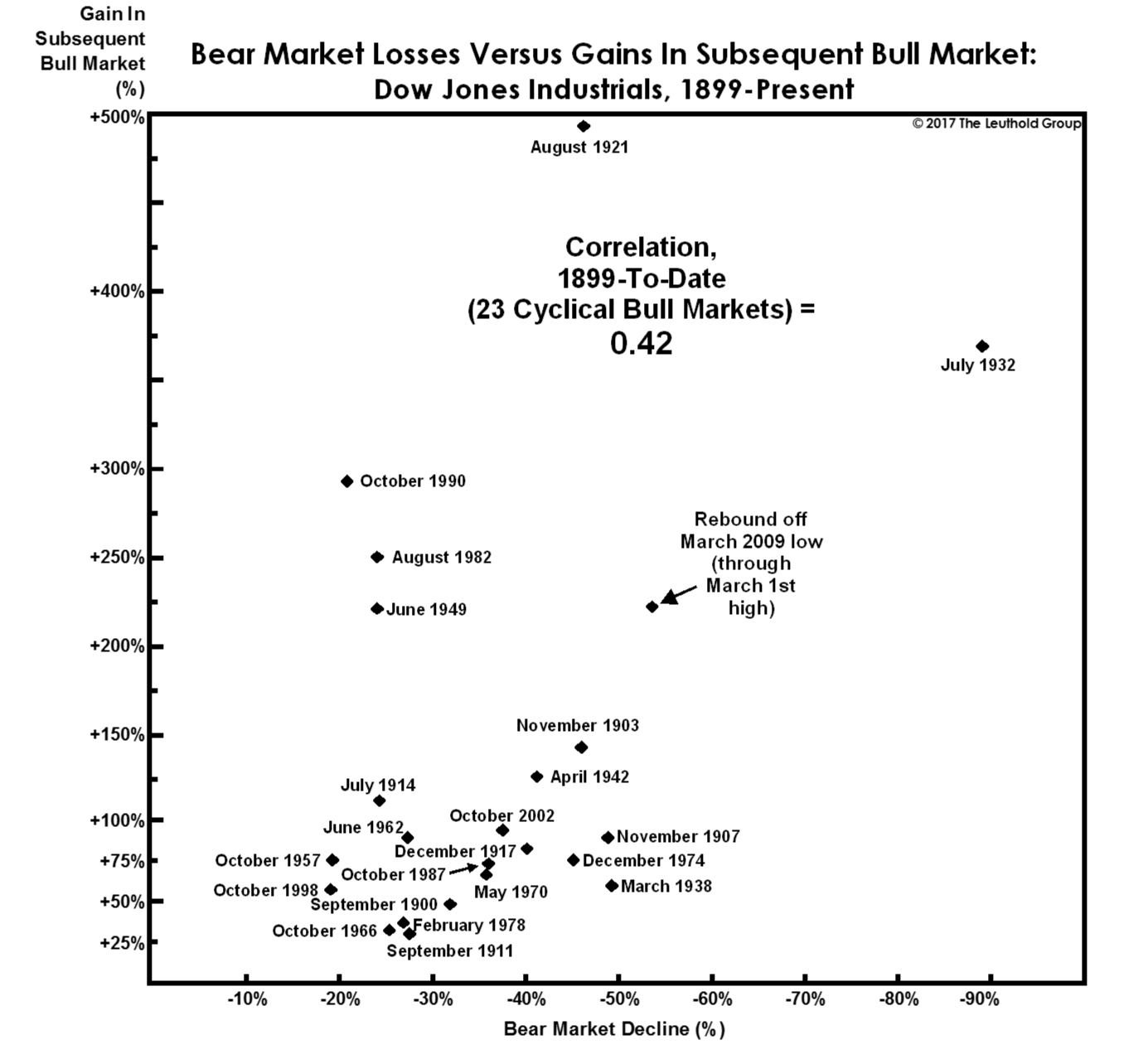

The scatterplot in Chart 2 provides another perspective. Cumulative DJIA bull market price gains are plotted against the depth of the preceding bear market. The correlation between the two series, at just 0.42, is lower than we expected.

With the benefit of hindsight it might now seem obvious that the DJIA was poised for a huge recovery following the 54% decline into its 2009 low. On the other hand, the three bull markets that followed the near -50% bears of 1907, 1973-74, and 1937-38 all failed to generate even a double in the DJIA. In short, a huge bear market loss is not a guarantee of an above-average subsequent bull market, but it’s certainly worked out that way in the current cycle.

© The Leuthold Group