The Deep Causes of Secular Stagnation and the Rise of Populism

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIn a companion paper, “Six Impossible Things Before Breakfast,” we present evidence that asset markets are generally priced for “secular stagnation,” and argue that this requires a number of extreme assumptions on the part of investors. However, we didn’t really explore the root causes and consequences of secular stagnation in that paper. We remedy that with this paper, which is a deep dive into the murky world of secular stagnation, its sources, and its impact.

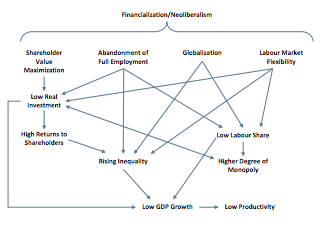

The rise of populism has been one of the broad themes to emerge over the last few years. This has left many within the establishment scratching their heads as to the cause of their fall from grace. From our perspective, the rise of populism has its roots in the same sources that have given rise to socalled “secular stagnation.” That is, a broken system of economic governance. This system – which we will hereafter refer to as “neoliberalism” – arose in the mid-1970s and was characterised by four significant economic policies: the abandonment of full employment as a desirable policy goal and its replacement with inflation targeting; an increase in the globalisation of the flows of people, capital, and trade; a focus at a firm level on shareholder value maximisation rather than reinvestment and growth; and the pursuit of flexible labour markets and the disruption of trade unions and workers’ organisations.

Exhibit 1: Secular Stagnation Without Unicorns

Source: GMO

The orthodox view on secular stagnation seems to adopt one of two perspectives: either that secular stagnation is caused by a situation where the real interest rate has to be negative in order to generate a return to growth (a demand-side explanation), or that something has gone very wrong with the nature of productivity in the economy (a supply-side explanation).

We have been outspoken critics of this framework1 of thinking. Rather than being the result of some unobservable figment of economists’ imaginations (as we believe the natural rate of interest to be), or some strange exogenous productivity event,2 we argue that it is the policies that have been pursued that have led to the observed “stylized facts” of secular stagnation (Exhibit 2). The neoliberal regime has given rise to: lower inflation; lower growth rates; lower investment rates; lower productivity growth; increasing income and wealth inequality; diminished job security; and a serious deflationary bias in the world economy that was only temporarily “plugged” by dangerously high levels of private sector debt accumulation. These are long-term trends that have been visible for decades, but they were severely exacerbated by the collapse of the global debt bubble in 2008-09.

Exhibit 2: The Stylized Facts of Secular Stagnation

Source: FRED, GMO

As the citizens of various countries around the world gradually woke up to the fact that the quick-fix solutions put in place after the crisis merely kept a lopsided and increasingly dysfunctional system ticking over, they rebelled. It was then that they started to cast votes for various populist political candidates in an apparent effort to shake up the system. Without such a splash of cold water to the face, there is every chance that the system would march on regardless of its dysfunction until it decayed to such an extent that it simply collapsed – not unlike what happened in the non-democratic Soviet Union. If we are to prevent our own sickly Brezhnev era from slipping into a terminal state, we must understand clearly the causes of our current morass.

The Four Pillars of Neoliberalism

Inflation targeting and the NAIRU

The first of the four key pillars of neoliberalism is the abandonment of full employment policy and its replacement with inflation targeting. After the Second World War governments around the world realised that they could easily generate full employment through spending and taxation policies. This realisation came because of the economic experiments undertaken during the war – experiments that were necessitated by the war but that were consciously structured in line with the economic approach outlined in Keynes’ 1936 book The General Theory of Employment, Money and Interest. As Nicholas Kaldor wrote, “The formal obligation to maintain high and stable levels of employment… emerged as a joint impact of the Keynesian revolution in economic thought and the Second World War.”3

These policies were remarkably effective, and the decades after the war are generally known today as capitalism’s Golden Age. The Golden Age was characterised by high rates of employment, economic growth, and an equitable distribution of income and wealth. In the mid-1970s, however, these policies were abandoned because they were thought to be causing inflation. This was an incorrect assessment, as the inflation was actually generated by oil shocks imposed by the OPEC cartel in response to US foreign policy in the Middle East combined with poor labour relations in the English-speaking countries that led to class conflict and strikes over who should bear the brunt of these higher oil prices.

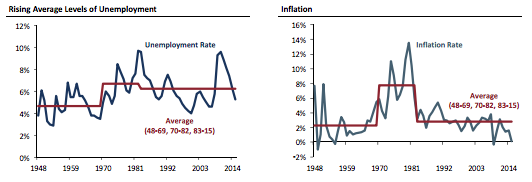

But the economics profession at the time did not realise this. Their theories told them that it was the full employment policies that were generating the inflation, and so they encouraged policymakers to abandon these policies and instead have the central bank attempt to control inflation through the use of monetary policy. The impact of these policies in the US could not be clearer, as shown in Exhibit 3.

Exhibit 3: The Impact of Abandoning Full Employment Policies in the US

Source: Fred

In these charts we see three periods: 1948-69 is the Golden Age of Keynesian full employment policy; 1970-82 is the crisis period of rising inflation due to OPEC oil price hikes and poor labour relations; and, finally, 1983-2015 is the period of inflation targeting. We can see immediately that after the crisis period the economy stabilised at a more normal level of inflation (although not quite as low as in the Golden Age). But unemployment did not. In fact, unemployment never went back to its Golden Age average – it stayed permanently elevated. This was simply due to the fact that governments stopped targeting full employment and instead turned their attention to inflation.

The rationale for this policy choice was the economic theory of the “Non-Accelerating Inflation Rate of Unemployment” (NAIRU). The NAIRU is supposedly the rate of unemployment at which inflation supposedly starts to accelerate ad infinitum. It is another one of those many wonderful “unobservables” that seem to dominate economic thinking. We cannot observe the NAIRU directly and so we do not know when we are crossing it. The NAIRU is only obvious after the fact; by the time it shows up in the statistics it is too late! It is a bit like a sailor in the medieval era confronted with the terrifying prospect that there might be dragons beyond a certain point on the map. The dragons are not an observable fact, but by the time they show up our poor sailor figures he will already be lunch. So he thinks it safer to stay within the known boundaries despite the fact that dragons are silly and imaginary.

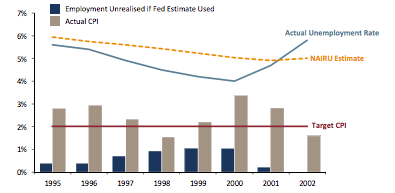

The other problem with the NAIRU is that it does not do what it is supposed to do. When economists try to actually estimate the NAIRU they tend to do a terrible job. In the 1990s, for example, most economists put the NAIRU in the US at around 5-6%. But because central banks ignored their economists and allowed the economy to continue to grow, unemployment fell much lower without substantial inflationary pressures. The ship set sail and the dragons never appeared. It was all a bit of a farce. Exhibit 4 lays out the NAIRU debacle of the mid to late 1990s.

Exhibit 4: The Uselessness of the NAIRU Estimate

Source: GMO

In this chart the orange dotted line represents the average NAIRU estimates produced by the Federal Reserve for that year. The blue line is the actual realised unemployment rate in that year. The blue bars represent the amount of employment that would have been “lost” if the Federal Reserve had taken the NAIRU estimates seriously, used them as a policy target, and succeeded in hitting this target. Finally, the beige bars are the actual CPI inflation rate and the red line represents the Federal Reserve target inflation rate.4 This chart tells a strange story – at least, if you believe that economists can estimate a NAIRU. In 1995 and 1996 the actual unemployment rate is very close to the NAIRU estimate and yet inflation is above target. Then in 1997 and 1998 unemployment falls substantially below the NAIRU estimate and yet inflation falls below the target level. In 1999 inflation begins to pick up again, and in 2000, when it breaks through the target rate, the Federal Reserve hikes interest rates and creates a recession. But it seems far more likely that something else was causing this inflation and that the Federal Reserve research team was focusing on the NAIRU while ignoring what was actually leading to inflation. All the evidence suggests that the complete opposite of what the Federal Reserve economists expected to happen actually happened: As unemployment began to fall below the NAIRU in 1997 and 1998, inflation actually fell. It did not rise as the Federal Reserve economists would have predicted. Not only did the NAIRU prove empirically useless, but if the Federal Reserve had taken it seriously between 1997 and 1999, substantially more US workers would have been needlessly unemployed than actually proved to be the case.5

The NAIRU was a failure, although many still adhere to the principles involved. Even the economic equivalent of Mr. Magoo, Alan Greenspan, has written that the NAIRU “was continually revised and did not offer a stable platform for inflation forecasting or monetary policy.”6 But even though many policymakers distrusted the NAIRU, it provided a rationale for their desired policy actions. It also gave governments a rationale to stop taking responsibility for full employment policy. In short, it provided the ideological justification for the high unemployment period of inflation targeting.

Globalization and the free movement of… everything!

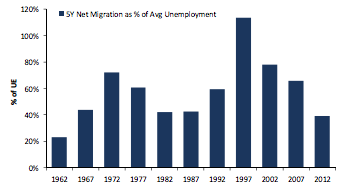

In the neoliberal era, politicians also advocated for the free movement of capital, labour, goods, and services. The free movement of labour has certainly gotten a lot of coverage in the news media. It is clear to us that this is the complaint that has driven many people to the populist parties. People seem to zero in on the issue of migration in order to articulate their frustration with the system. They perceive migrants as taking their jobs and driving down wages. Insofar as taking jobs goes, it is not hard to see where this perception comes from. Exhibit 5 plots five-year net migration into the US adjusted by the average number of people unemployed in the five-year period in question.

Exhibit 5: The Free Movement of Labour and the Rise of Populism

Source: FRED, GMO

Looking at this chart, it is not hard to see why people tend to blame their economic problems on migrants. We have already seen that unemployment has reached structurally higher levels after the Golden Age of capitalism. This has been accompanied by increases in net migration into the US. It is not difficult to understand why unemployed people would tend to take this correlation to imply causation and blame their joblessness or job insecurity on migration.

But the key impact that globalisation has had on working people is not to encourage the free movement of labour, but rather to encourage the free movement of goods and services. This has both pros and cons. On the pro front, the US consumer has benefited from lower prices. The cons include reduced domestic demand and job losses.

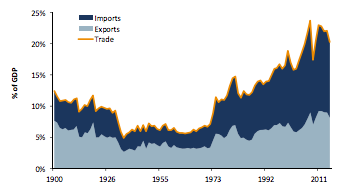

This is reflected in the rhetoric of many populist campaigners who tell their constituents that globalisation has served to take their jobs and create unemployment. This assertion is by no means without merit. Exhibit 6 plots trade broken down into its components in the US as a percentage of GDP since 1900.

Exhibit 6: The Impact of Globalisation on the Trade Balance (1900 – 2015)

Source: GMO

We can see from this chart that the new neoliberal-globalisation regime that emerged in the mid- 1970s was not simply aimed at increasing trade. While it is true that trade has increased since this time, the trend that really stands out is how rapidly imports have increased as a share of GDP. Exports have increased in this period, but not by nearly as much. The real story here is that the globalisation-neoliberal regime has led Americans to buy more and more goods from abroad without being compensated for this by having foreigners buy more American goods in return.

In fact, this is a structural tendency of the US economy itself that was noted just before the globalisation-neoliberal regime began. In 1969 the economists Houthakker and Magee noted that “disparities in income elasticities [for trade] appear to be significant in the case of [the US].”7 This meant that the US had a tendency to suck in more imports as it grew than the rest of the world absorbed in the form of US exports. The Houthhakker-Magee finding strongly suggested that if trade increased as a percentage of US GDP it would have a detrimental effect on the balance of trade.

This deterioration in the trade balance acted as a deflationary vacuum, sucking demand out of the US economy. Hence, people raising concerns about the trade arrangements that the US currently subscribes to are not wrong. These trade arrangements are job killers.

Once again, it was orthodox economic theory that justified these arrangements. The 1990s were the pivotal period in which so-called free trade between countries was pushed; this was the era of the Clinton administration’s NAFTA, for example. The theory that was used to justify trade liberalisation was that of the simple Ricardian comparative advantage model presented to undergraduates in classrooms worldwide. The model basically states that countries are better off specialising in products that they are better at producing. In essence, it is simply Adam Smith’s division of labour argument applied to countries rather than people: If you are a talented gardener and I am an expert at fixing cars, then rather than you learning how to repair your car and me learning how to garden, I’ll fix your car and you tend my garden. This simple model is sometimes scaled up to a general equilibrium model called the Hecksher-Ohlin model, but the assumptions and conclusions are basically the same. It was this general equilibrium model that was used to justify trade liberalisation in recent years. For example, in 1996 Michel Camdessus, then Managing Director at the IMF, said the following in a speech entitled “Promoting Freer Trade”:

In our work with 181 member countries, we repeatedly see that opening economies to external trade helps get domestic prices “right,” so that market signals improve domestic resource allocation, increase efficiency, and create conditions under which domestic firms can compete successfully in foreign markets.

There are any number of theoretical problems with the comparative advantage/general equilibrium model. It assumes full employment in all countries, for example, but most economies are not operating at full employment at any given moment in time. It also assumes perfect competition and a homogenous production function that perfectly allocates transferable capital (“putty capital”) according to how it is required – whereas in reality, perfect competition never exists, homogenous production functions are logically incoherent, and the notion of putty capital is a disingenuous fiction.8

There are other problems with the framework, but perhaps most importantly from our perspective: The model assumes that trade imbalances will not occur. Yet, Houthhakker and Magee showed clearly that such imbalances would and did occur. Today, liberalised trade has led to a “decimation” of high-paid manufacturing jobs in the US. In 1970 around 25% of the US workforce was employed in manufacturing; by 2011 this number had fallen to around 9%. While some of this decline may have had to do with technological advances, a good portion was due to trade liberalisation.

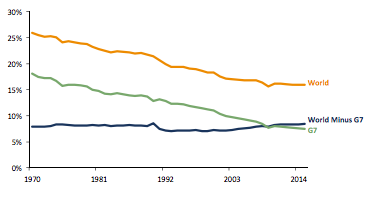

This is shown in Exhibit 7, which plots manufacturing output as a percentage of world GDP for both the world and for various regions.9 As we can see, world manufacturing as a share of GDP has declined substantially in the past 35 years – from around 26% of GDP to around 16%. But as we can also see, this decline has been completely concentrated in the G7 countries; non-G7 countries have seen absolutely no decline in their manufacturing as a share of GDP. This suggests that there has been an overall decline in manufacturing as a share of GDP that is probably being driven by technology and other factors, but this decline has been totally borne by the advanced G7 economies.

Exhibit 7: Manufacturing as a Percent of World GDP (1970 – 2015)

Source: GMO

Economic theory would lead us to believe that increases in technological progress should actually impact the developing economies rather than the advanced economies. This is called the “convergence hypothesis,” which states that developing economies should be able to “catch up” with or copy the developed economies’ technology. The fact that the developing countries have held their manufacturing share of GDP constant while the developed economies have seen their share crater makes a strong case that globalisation is the main force driving the decline in manufacturing in the G7 countries. Technological progress has been real, but has been a secondary impact on the deindustrialisation that we have seen in the G7 economies over the past 35 years.

The result of this deindustrialisation has been the destruction of high-paid, stable, often unionised manufacturing jobs and the growth of low-paid, unstable, and non-unionised service sector jobs. This has proved to be a key causal factor in the soaring wealth and income inequality that we showed earlier.

The Rise of Shareholder Value Maximisation

The third pillar is one that we have written an entire paper on.10 The mantra of shareholder value maximisation (SVM) is ubiquitous these days, but it is based on the same poor economics as the other pillars of neoliberalism. As we wrote in that paper:

From a theoretical perspective, SVM may well have its roots in the work of Arrow and Debreu (in the late 1950s/early 1960s). These authors demonstrated that in the presence of ubiquitous perfect competition and fully complete markets (neither of which assumption bears any resemblance to the real world,11 of course) a Pareto optimal outcome will result from situations where producers and all other economic actors pursue their own interests. Adam Smith’s invisible hand in mathematically obtuse fashion.

However, more often the SVM movement is traced to an editorial by Milton Friedman in 1970.12 Given Friedman’s loathing of all things Keynesian, there is a certain delicious irony that the corporate world is so perfectly illustrating Keynes’ warning of being a slave of a defunct economist! In the article Friedman argues that “There is one and only one social responsibility of business – to use its resources and engage in activities designed to increase its profits...”

Friedman argues that corporates are not “persons,” but the law would disagree: Firms may not be people but they are “persons” in as much as they have a separate legal status (a point made forcefully by Lynn Stout in her book, The Shareholder Value Myth). He also assumes that shareholders want to maximize profits, and considers any act of corporate social responsibility an act of taxation without representation – these assumptions may or may not be true, but Friedman simply asserts them, and comes dangerously close to making his argument tautological.

Following on from Friedman’s efforts, along came Jensen and Meckling in 1976. They argued that the key challenge when it came to corporate governance was one of agency theory – effectively, how to get executives (agents) to focus on maximizing the wealth of the shareholders (principals)…

Under an “efficient” market, the current share price is the best estimate of the expected future cash flows (intrinsic worth) of a company, so combining EMH with Jensen and Meckling led to the idea that agents could be considered to be maximizing the principals’ wealth if they maximized the stock price.

This eventually led to the idea that in order to align managers with shareholders they need to be paid in a similar fashion. As Jensen and Murphy (1990) wrote, “On average, corporate America pays its most important leaders like bureaucrats.” They argued that “Monetary compensation and stock ownership remain the most effective tools for aligning executive and shareholder interests. Until directors recognize the importance of incentives and adopt compensation systems that truly link pay and performance, large companies and their shareholders will continue to suffer from poor performance.”

The practical upshot of this obsession with SVM is that managements with short tenures and loaded with stock options prefer to focus on financial engineering rather than long-term aims such as growth. Data presented in our prior paper showed that CFOs would willingly pass up on good investment projects if doing so meant that quarterly earnings would fall short of expectations. We also presented evidence from Asker et al., which showed that public firms invested about half as much as private firms.

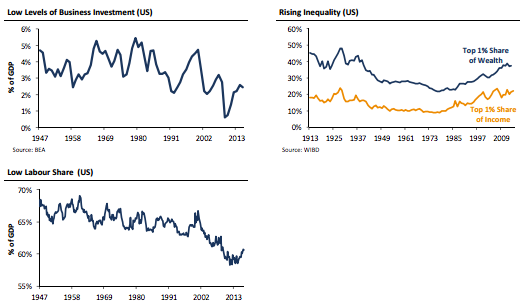

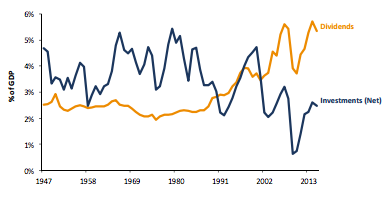

This preference for payouts over investment is clearly seen in Exhibit 8, which shows the same business net investment as shown earlier, and dividends. Historically, investment used to be over 4% of GDP and dividends around 2%. Today the complete reverse is seen. The obsession with returning cash to shareholders under the rubric of SVM has led to a squeeze on investment (and, hence, lower growth), and a potentially dangerous leveraging of the corporate sector.

Exhibit 8: Dividends vs Investment for USA Inc.

Source: BEA

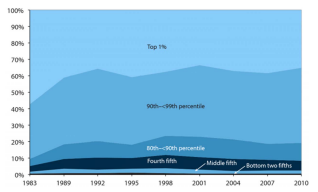

To see how this is related to the rising inequality that we have seen, it is only necessary to understand who benefits from a rising stock market (i.e., who gets the “benefits” of the SVM and its buyback frenzy). The identity of this group is revealed in Exhibit 9. The top 1% own nearly 40% of the stock market; the top 10% own 80% of the stock market. These are the beneficiaries of SVM.

Exhibit 9: Wealth Group Shares of Total Household Stock Wealth (1983 – 2010)

Source: Wolff (2012)

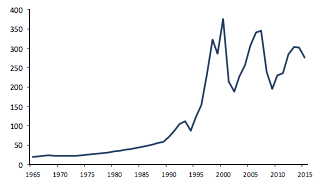

Another reflection of the role of SVM in creating inequality can be seen by examining the ratio of CEO-to-worker compensation. Before you look at the evidence, ask yourself what you think that ratio is today and what you think is “fair.” A recent study by Kiatpongsan and Norton (2014) asked these exact questions. The average American thought the ratio was around 30x, and that “fair” would be around 7x.

The actual ratio is shown in Exhibit 10. It turns out the average American was off by an order of magnitude! If we measure CEO compensation including salary, bonus, restricted stock grants, options exercised, and long-term incentive payouts, then the ratio has increased from 20x in 1965 to a peak of 383x in 2000, and today sits somewhere just short of 300x!

Exhibit 10: US CEO-to-Worker Compensation Ratio (1965 – 2015)

Source: EPI

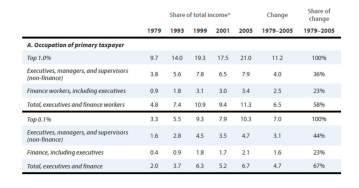

We can see this has been a driving force behind the rise of the 1% thanks to a study by Bakija, Cole, and Heim (2012). The rise in incomes of the top 1% has been driven largely by executives and those in finance. In fact, executives and those in finance accounted for some 58% of the expansion of the income for the top 1%, and 67% of the increase in incomes for the top 0.1% between 1979 and 2005 (Exhibit 11). Thus, there can be little doubt that SVM has played a major role in the increased inequality that we have witnessed.

Exhibit 11: Role of Executives and Financial Sector in Income Growth of Top 1.0% and Top 0.1% (1979 – 2005)

Source: EPI

This makes the decline in the labour share even more dramatic for those outside of the top 1%. Exhibit 11 includes the top 1%, so if we were to exclude them, the share of GDP going to the rest of labour would be even lower. In fact, if we look at the bottom 90% we would see their labour share of GDP going from around 42% in the late 1940s to approximately 27% today.

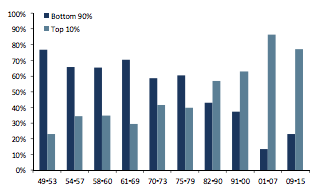

If one looks at the income gains during expansions as shown in Exhibit 12, one will find that during the last two expansions the income gains have gone largely to the top 10%.

Exhibit 12: Distribution of Average Income Growth During Expansions

Source: Piketty, Saez and Zucman – Distributional National Accounts, GMO

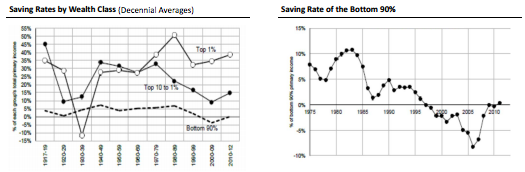

The problem with this (apart from being an affront to any sense of fairness) is that the 90% have a much higher propensity to consume than the top 10%. Thus, as income and wealth is concentrated in the hands of fewer and fewer, growth is likely to slow significantly. A recent study by Saez and Zucman (2014) provides us with the evidence. As Exhibit 13 shows, 90% have a savings rate of effectively 0%, while the top 1% have a savings rate of 40%.

Exhibit 13: Savings Rates by Wealth Group

Source: Saez and Zucman (2014)

The role of SVM in declining labour share should be obvious, because it is the flip side of the profit share of GDP. If firms are trying to maximize profits, they will be squeezing labour at every turn (ultimately creating a fallacy of composition where they are undermining demand for their own products by destroying income).

Flexible Labour Markets

The idea of a “flexible” labour market sounds pretty appealing. After all, we all like “work flexibility,” “flexible working hours,” and a whole other host of “flexiblisms” in our working lives – so shouldn’t we also like “flexible labour markets?” The mainstream economists would argue that we should. They tell us that flexible labour markets produce optimal outcomes. They ask us to view labour markets as we would the market for apples or bananas. We are told that the market for apples and bananas works best when we can haggle over the price because, if we can, the supply of and demand for apples can be brought into a nice, neat equilibrium.13 We are then told that the market for labour works the same way.

In the labour market, we are told, there is a price of labour – this is the wage rate – and there is also a quantity of labour – this is the number of people willing and able to work. A higher wage rate leads to more people wanting to work, while a lower rate leads to less. Employers determine what wage rate works for them and offer it on the market. Workers are then given the choice whether they want to work for this rate and the number of hours they are willing to work. The wage rate then adjusts in order to satisfy everyone involved and the labour market reaches a tidy equilibrium – that is, the market clears. This is the economist’s vision of a flexible labour market.

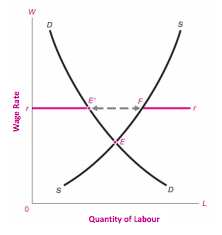

An inflexible labour market, on the other hand, is one in which the wage rate is not allowed to adjust. This is typically said to occur because trade unions organise workers and demand a wage rate that employers do not want to pay. This leads to too high a wage rate for market-clearing equilibrium to occur and unemployment results. In their popular textbook Economics14 Paul Samuelson and William Nordhaus lay out the graph in Exhibit 14 depicting this scenario.

Exhibit 14: Labour Demand Shift and Market Clearing

Source: Samuelson and Nordhaus

They write:

Raising the standard wage to rr increases wages and decreases employment in the unionized labor market. Because of supply and demand imbalance, workers from E to F cannot find employment in this market (p 259).

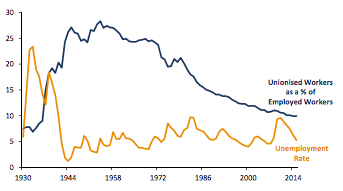

The problem with this theory is that it is not supported by the evidence. If the theory were correct then we would expect the rate of worker unionisation to be negatively correlated with the rate of unemployment. But this is not the case at all. In fact, when the rate of unionisation in the US was at relatively high levels, there were very low rates of unemployment, and when it was at very low levels, there were very high rates of unemployment – although trying to detect a strict correlation is difficult (Exhibit 15).

Exhibit 15: US Unionisation Rates and Unemployment Rates (1930 – 2015)

Source: CBO, FRED, GMO

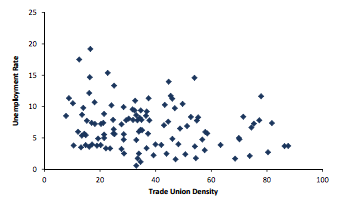

The theory also proves false when examined cross-sectionally. If the theory were true, then the rate of unemployment would be higher in countries with higher rates of unionisation. The scatterplot diagram in Exhibit 16 lays out the 10-year averages of the unemployment rate and the trade union density of 33 countries from 1960-2010.

Exhibit 16: Average Rate of Unemployment and Trade Union Density (1960 – 2010)

Note: Total number of observations = 114.

Source: ILO, GMO

It is clear that there is little or no relationship between trade union density and the unemployment rate. In fact, if anything the relationship is negative – implying that a higher trade union density is correlated with a lower rate of unemployment; the exact opposite of what the theory predicts!

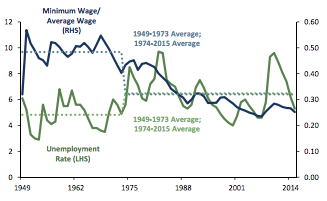

Another component of the labour market flexibility dogma is that there should be no minimum wage. The argument against the minimum wage is identical to the argument against trade unions: The minimum wage provides an arbitrary barrier to workers and employers forming agreements as to what the wage should be. The effect, we are told, is to render low-productivity workers who may have been offered wages lower than the minimum wage unemployed.

Again, this is a nice story but it does not fit with the facts. If this were true, then the higher the minimum wage (relative to the average wage), the more people would be rendered unemployed. But when we turn to the data we find that this is not the case. Exhibit 17 plots the US minimum wage (relative to the average wage) against unemployment. As we can see, the minimum wage was actually higher during the period of low unemployment than it was in the era of high unemployment – the exact opposite of what the theory would suggest. The relationship is not very strong and it is not something that we would want to hang our hat on, but it has the wrong sign from the standard theory viewpoint.

Exhibit 17: US Minimum Wage and Unemployment Rate (1949 – 2015)

Source: FRED

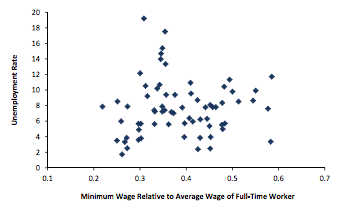

As with the trade union data, the evidence also runs contrary to the theory when we examine it cross-sectionally. The scatterplot in Exhibit 18 plots the 10-year averages of the minimum wage and the unemployment rates for 25 different countries from 1960-2010. If the theory were true, we would expect to see a strong positively-sloped relationship – indicating that countries with higher minimum wages tended to have higher unemployment. In actual fact there is no strong relationship between the two variables.

Exhibit 18: Average Rate of Unemployment and the Average Minimum Wage (1960-2010)

Note: Total number of observations = 81.

Source: OECD, GMO

Neoliberalism based on economic fallacies

In light of all this evidence, we believe it is safe to say that the mainstream theory is false. Is there, then, an alternative theory? In fact, there is. The alternative theory says that the distribution of income is a fundamental, “deep” component of the structure of the macroeconomy that determines other macroeconomic relationships – most notably the structure and level of aggregate demand. According to this theory, if too much income accumulates in too few hands – due to low wages relative to the productive capacity of the economy – then there will be a shortfall of demand for the output of the economy because richer people consume less out of their income than less rich people. This will lead to unemployment and low economic growth.

The alternative theory is based on a vision of the labour market as being fundamentally different from other markets and determined by the relative class strength of workers and capitalists. Trade unions and minimum wage laws are seen as bulwarks against capitalists accumulating too much power, wages falling, and the economy tipping into stagnation. In stark contrast to the mainstream theory, lower, not higher, wages are associated with unemployment-biased outcomes.

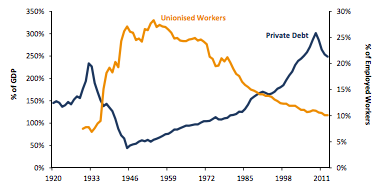

The other thing the low income workers can do to buttress their flagging income is accumulate large amounts of debt. If wages are too low because worker bargaining power is too low, the demand gap that results can be “plugged” through workers accumulating large amounts of debt. But this accumulation of debt is limited. As more and more debt accumulates, the marginal borrower becomes less and less creditworthy. Eventually this leads to what the economist Hyman Minsky called “Ponzi lending,” where the borrowers have to take on more debt just to meet the interest repayments on the old debt.15 Soon after the borrowing cycle enters the Ponzi phase, the credit bubble blows up and the economy experiences a sharp recession or depression, which then turns into stagnation. Empirically, this theory holds up far better than its mainstream rival as can be seen in Exhibit 19, which plots trade union density in the US versus the accumulation of private sector debt.

Exhibit 19: US Private Debt Ratio and Trade Union Density Source: GMO

Source: GMO

Labour market flexibility may sound appealing, but it is based on a theory that runs completely counter to all the evidence that we have. The alternative theory suggests that labour market flexibility is by no means desirable as it results in an economy with a bias to stagnate that can only maintain high rates of employment and economic growth through debt-fuelled bubbles that inevitably blow up, leading to the economy tipping back into stagnation.

Neoliberalism: A project spelled D.I.S.A.S.T.E.R.

Neoliberalism is a political and economic project that literally could not be worse for either politics or economics. The policies that it prescribes are deeply unpopular and dysfunctional. Citizens reel at their loss of jobs, stability, and incomes while the economy tips into instability and stagnation. It is also a project that benefits the few at the expense of the many. It results not only in a spoiled class of high income individuals, but also a class of detached technocrats. This detachment allows them to pursue their misguided policies that throw the economy into chaos... all the while drawing comfort from economic theories that conflict with reality.

Populism is a response to neoliberalism. It has taken 40 years for the true effects of neoliberalism to become clear. But now that they are clear they are dramatic. Most developed economies have been hollowed out and are now empty shells of what they used to be. They run enormous trade deficits and they make less and less of the goods that people actually consume. Meanwhile, all they produce are jobless workers and unsatisfied citizens. It is obvious that at some point the neoliberal consensus had to break as newcomers to the political scene offered to solve these problems while the political establishment just offered more of the same.

Escaping Neoliberalism

There are ways to escape from the stagnation and instability of neoliberalism. But they involve restructuring our economies on more equitable and sustainable lines by addressing the problems that we raised above. Let us take each of these problems in turn and provide what is likely to be the most powerful single policy response.

Inflation Targeting and the NAIRU: Policymakers have been telling central bankers to steer the economy using monetary policy while always keeping an eye open for the non-existent NAIRU in order to shirk responsibility for maintaining full employment. This is no longer acceptable. Fiscal policy is a far more effective tool to maintain full employment. But many are concerned that governments will go overboard and spend until they generate inflation. The best solution to these two problems is to replace the NAIRU – the Non-Accelerating Inflation Rate of Unemployment – with the NAIBER – the Non-Accelerating Inflation Buffer Employment Ratio.

The NAIBER concept is similar to the notion of a “buffer stock” that many readers will be familiar with in relation to commodity markets. When the harvest is good and the market price is low, the government offers a fixed price for the commodity. This ensures that farmers do not see their incomes fall. When the harvest is poor, the government releases the stored commodity into the market, thereby driving the price down. This ensures that end consumers do not starve and there is no price inflation. The NAIBER aims to do the same thing in the labour market.

The government offers a fixed wage for any labour that is forthcoming. This wage acts as the de facto minimum wage, below which no labour will be forthcoming to private sector employers. When unemployment is high, workers will flow into the government scheme, and when the economy starts to grow, private employers “hire off the top” of the scheme by offering a wage above the NAIBER wage. The workers can be outsourced to private charity groups to do any number of jobs that are currently not done. They might clean rivers, help the disabled, care for the elderly, clean up graffiti, plant public gardens… the list of potential useful things these people might do is boundless.16

The program ensures full employment at all times. It also smooths the level of aggregate demand in the economy through the NAIBER wage. In addition to this, it maintains workers as workers – that is, it does not leave them idly wasting away their skills on welfare, ultimately rendering them unemployable. Finally, it provides a check on inflation because the NAIBER wage is set by the government and cannot rise unless the government chooses. Because the wages cannot grow, neither can the price level.

A NAIBER program would solve the unemployment problem in developed economies. It would also provide discontented people drawn to populist movements with a sense of purpose and train them to work for a living. The NAIBER is probably the single best policy that could be implemented by any government trying to stave off stagnation and populism.17

Globalisation and Trade: The impact of globalisation on the trade balances of developed economies is not as simple a problem to solve as unemployment. This is because it has resulted, as we have seen, in a fundamental restructuring of our economies – away from high productivity/high export manufacturing and toward low productivity/low export services. The best way to deal with this problem is for governments to run a beefed-up policy of import substitution.

Import substitution works by governments identifying the products that are currently imported from abroad that could easily be produced domestically. So, for example, cheap Chinese toasters are probably substitutable, while foreign diamonds are probably not. The government then offers significant direct subsidies to companies that are willing to produce these goods. The subsidy is then passed through to the consumer as a lower price, which will render the product competitive with the cheaper foreign good.

This is probably the most potent policy that can be undertaken to decrease reliance on foreign imports and return manufacturing to the domestic economy. But it should be thought of as part of a broader program for reindustrialisation – an industrial policy for the 21th century that involves directed investment in domestic industry, as was done in France after World War II.18

Shareholder Value Maximisation (SVM): SVM is not the result of a policy choice. It is the result of a shift in how corporations govern themselves – a corporate choice, not a government one, if you will. It can easily be stopped if corporations take it upon themselves to stop engaging in it. As we have seen above, doing so will probably render them more profitable and more competitive. Beyond that, we would simply say that while we do not think of SVM as a policy choice, a government in the future may begin to think of it in these terms if corporations do not get their own houses in order. If they value their independence they might heed this warning now before it is too late. Populists have policies too, you know.

Flexible Labour Markets: The NAIBER policy mentioned above will give workers a far stronger bargaining position as they will no longer be as fearful of unemployment. It will also implement a de facto minimum wage that will be impossible for unscrupulous employers to evade. In addition to this, a serious import substitution and industrial policy will help return high-wage, (often) unionised jobs to developed countries. But none of this is a substitution for governments promoting reasonable, equitable policies to allow for unionisation.

For the past four decades unions have been demonised as slippery devils, always willing to sabotage the public purpose for their own narrow interests. But unions can play a fundamental role in ensuring that the distribution of income is fair, thus ensuring that the macroeconomy is balanced in such a way that workers can consume what they produce. If policymakers fear striking workers and hot-headed shop stewards they should look to the Scandinavian countries where capitalist-worker-government relations are excellent because everyone treats one another with respect, everyone gets a seat at the table, and equitable outcomes are reached.

The policy choices embodied within neoliberalism have delivered us unto a world of secular stagnation. Populism was born out of the resulting economic malaise (just as it has been in the past). However, it doesn’t have to be this way; alternative policies are available. They require “unlearning” a wide variety of economic theories that are oft held to be self-evident, and as Keynes long ago noted, “The difficulty lies, not in the new ideas, but in escaping from the old ones, which ramify, for those brought up as most of us have been, into every corner of our minds.”

James Montier is a member of GMO’s Asset Allocation team. Prior to joining GMO in 2009, he was co-head of Global Strategy at Société Générale. Mr. Montier is the author of several books including “Behavioural Investing: A Practitioner’s Guide to Applying Behavioural Finance”; “Value Investing: Tools and Techniques for Intelligent Investment”; and “The Little Book of Behavioural Investing.” Mr. Montier is a visiting fellow at the University of Durham and a fellow of the Royal Society of Arts. He holds a B.A. in Economics from Portsmouth University and an M.Sc. in Economics from Warwick University.

Philip Pilkington is a member of GMO’s Asset Allocation team. Prior to joining GMO in 2014, he contributed to numerous online and print media outlets as a freelance economic journalist and ran a popular economics blog. He is also the author of the book “The Reformation in Economics: A Deconstruction and Reconstruction of Economic Theory.” Mr. Pilkington earned his B.A. in Journalism from the Independent Colleges, as well as his M.A. in Economics from Kingston University.

Disclaimer: The views expressed are the views of James Montier and Philip Pilkington through the period ending March 2017, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Appendix: Why “Productivity” Does Not Measure Productivity

As mentioned in the main essay, the supply side explanation for “secular stagnation” is usually shrouded in the language of our ills resulting from a low rate of productivity growth. This provides many economists with comfort because it absolves them of guilt in the face of economic stagnation and populist insurgencies. Rather ironically, the decline in productivity is generally attributed to a lack of technological innovation – this is ironic because, as we have seen, the decline in manufacturing is explained by reference to a high rate of technological innovation (which should of course produce high levels of productivity). But then, no one ever praised economists for their consistency!

It is true today that measured productivity growth is quite slow. But there is an alternative way of looking at this variable. The mainstream position is basically that productivity is “exogenous” or “given” – a result of technological innovation that is not much influenced by the broader economy.19 The conclusion is that stagnation in the economy is driven by stagnation in the development of technology. This is a dreary message, but it effectively tells us that we cannot do much about our lot and that it is not really anyone’s fault.

The alternative view is that measured productivity does not actually measure productivity. In order to understand this we must understand how productivity – and here we refer to labour productivity – is measured.20 It really is quite simple and can be stated as such:

This is an intuitively simple measure; it tells us how many units of output are produced by each worker. Economists often assume that this tells us the potential productivity of each worker. But what is interesting about the measure is that it is a residual. It is not a directly observed statistic like GDP or employment numbers, which are both collected through surveys and other direct methods. Rather, it is derived by dividing one metric by another.

But, being a residual, it is highly likely that it is just reflecting changes in the two metrics that it is constructing out of; that is, GDP and employment. It is really just reflecting what might be referred to as the “labour content of GDP” at any given moment in time. But what explains this labour content of GDP is anyone’s guess. It could be any number of things from a weak recovery that generates poor jobs to an increase in precarious part-time work.

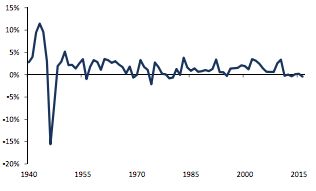

This becomes obvious if we look at the full statistics. Often productivity numbers are presented from 1948 onwards. This is what the Bureau of Economic Analysis (BEA) in the US publishes. But these figures leave out a giant natural experiment: the Second World War. Here was a moment in history when aggregate demand was rapidly increased in the US economy while a large number of skilled workers were sent overseas to fight. If the productivity measure is truly measuring what it claims to measure, then we should see it behave with reasonable stability in this era – or perhaps even falling slightly as unskilled workers fill the roles of skilled workers. But we do not. Instead, as Exhibit 20 shows, the productivity measure soars.

Exhibit 20: US Labour Productivity Growth (1940 – 2015)

Source: GMO

Between 1941 and 1944 US productivity growth increased by 34%. This was at a time when about 19% of the skilled labour force (5.3 million males) was mobilised for war and replaced by unskilled labour that required training. Meanwhile, as demobilisation occurred between 1945 and 1947, US productivity growth fell by 22%. This was while GIs came back to work in the factories. It is clear from these numbers that “productivity” is merely a residual statistic that says almost nothing whatsoever of interest. All that productivity statistics tell us is what happens when we divide real GDP by total employment – but we may as well divide the number of divorces by the number of foxes killed on highways. Neither statistic can be given any firm economic meaning.

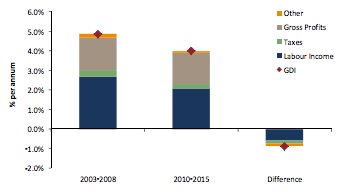

Looking at the more recent period,21 we can see in the US that Gross Domestic Income (which has to equal GDP) has been low since the financial crisis because labour income has been low (Exhibit 21).

Exhibit 21: Composition of Gross Domestic Income

Source: BEA, GMO

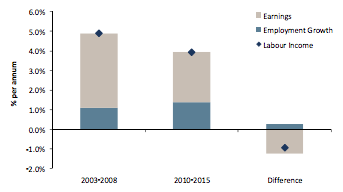

In turn, Exhibit 22 indicates that labour income has been low because earnings have been low.

Exhibit 22: Composition of Labour Income

Source: BEA, GMO

Hence, we can say that output is lower because labour income is lower, and labour income is lower because of earnings. Thus low productivity looks to have a strong demand component to it. The important thing to note here is that productivity is not some exogenous concept that has a life of its own.

That said, it seems to us that real productivity – however we would actually measure the concept – is highly likely to be negatively affected by the neoliberal policy platform. This is because real productivity is probably driven by the investment in new research and development, machines, and so on. If investment is negatively impacted because aggregate demand for goods and services is low and unstable, then it is likely that actual productivity will also take a hit.

1 See, for example, “The Idolatry of Interest Rates, Part I: Chasing Will-’o-the-Wisp,” May 2015. This white paper is available with registration at www.gmo.com.

2 We argue that the slowdown in productivity largely reflects the slowdown in growth, rather than causing it. This hypothesis is explored in the appendix to this paper.

3 Nicholas Kaldor, Essays on Economic Policy: Volume 1, p 96, 1964.

4 This 2% target is a completely mystical construction. While very high inflation may be undesirable and substantial deflation damaging, there is no “right” level of inflation according to any accepted economic theory. The Federal Reserve economists are simply engaged in assertion when they write on their website: The Federal Open Market Committee (FOMC) judges that inflation at the rate of 2 percent is most consistent over the longer run with the Federal Reserve’s mandate for price stability and maximum employment. Over time, a higher inflation rate would reduce the public’s ability to make accurate longer-term economic and financial decisions. On the other hand, a lower inflation rate would be associated with an elevated probability of falling into deflation, which means prices and perhaps wages, on average, are falling – a phenomenon associated with very weak economic conditions. Frankly, the Federal Reserve has no idea what level of inflation is best for the economy. Nor does it have any reasonable argument as to why such a hypothetical ideal level should be constant over time. Yet this target is sacrosanct in the halls of central banks across the world. This pseudo-statistical absurdity, which resembles old practices of Biblical numerology, will not be lost on future historical observers of human folly.

5 The Philadelphia Federal Reserve webpage that contains the NAIRU estimate data gives the reader the following, rather ironic, warning: The Federal Reserve staff’s real-time estimates of the NAIRU should be interpreted with caution. First, there is no unique conceptual definition of the NAIRU, and the definition used in Federal Reserve staff estimates of the NAIRU has evolved over time. No unique conceptual definition!? And this metric is supposed to tell policymakers when to start throwing people out of their jobs!? Surely this is among the worst modern excesses of an intellectual bureaucracy taking its imaginary models and pseudo-statistical jargon far too seriously.

6 Alan Greenspan, The Age of Turbulence: Adventures in a New World, p 170, 2008.

7 H.S. Houthhakker and Stephen Magee, “Income and Price Elasticities in World Trade,” The Review of Economics and Statistics, May 1969.

8 See: Geoffrey Harcourt, Some Cambridge Controversies in the Theory of Capital, Gregg Revivals, 1991. 9 The graph uses data drawn from the UN. It is slightly complicated by the fact that this data is published as manufacturing as a share of Gross Value Added (GVA) rather than as a share of Gross Domestic Product (GDP). In order to aggregate this data we have had to adjust it using the UN’s GDP data for each country as it does not publish GVA. We have assumed that GDP and GVA are basically identical and any slippage between the two series will not bias the reconstructed data. This does not seem farfetched given that the correlation between GDP and GVA growth is very tight; for example, in the US the correlation (R^2) between the two series is around 0.93. This should not be a surprise because GVA + taxes on products – subsidies on products = GDP.

9 The graph uses data drawn from the UN. It is slightly complicated by the fact that this data is published as manufacturing as a share of Gross Value Added (GVA) rather than as a share of Gross Domestic Product (GDP). In order to aggregate this data we have had to adjust it using the UN’s GDP data for each country as it does not publish GVA. We have assumed that GDP and GVA are basically identical and any slippage between the two series will not bias the reconstructed data. This does not seem farfetched given that the correlation between GDP and GVA growth is very tight; for example, in the US the correlation (R^2) between the two series is around 0.93. This should not be a surprise because GVA + taxes on products – subsidies on products = GDP.

10 James Montier, “The World’s Dumbest Idea,” December 2014. This white paper is available with registration at www. gmo.com.

11 Break these assumptions and you break the link between shareholder value maximization and social welfare. But trivial details like the critical realism of assumptions never seem to bother the average economist.

12 It is quite staggering just how many bad ideas in economics appear to stem from Milton Friedman. Not only is he culpable in the development of SVM, but also promotion of that most facile theory of inflation known as the quantity theory of money. Most egregiously of all, he is the father of the doctrine of the “instrumentalist” view of economics, which includes the belief that a model should not be judged by its assumptions but by its predictions.

13 We are not told to ignore the fact that when most of us visit the supermarket to buy apples and bananas we actually face fixed-price markets in which we are not able to haggle with the shop assistant. But we assume that we should ignore this because… well, the theory is really quite clever and tidy.

14 Paul Samuelson and William Nordhaus, Economics, McGraw-Hill Education, 19th edition, April 8, 2009. (Nineteenth edition… popular book!)

15 Hyman Minsky, “The Financial Instability Hypothesis.” Available at: http://www.levyinstitute.org/pubs/wp74.pdf

16 One of the commonly raised objections to the Job Guarantee Schemes is the question as to how they can be financed. Our take on fiscal deficits and functional finance has been outlined in the white paper “Market Macro Myths: Debts, Deficits, and Delusions.” To wit, we believe functional finance and the Job Guarantee Schemes sit very comfortably together.

17 For more detail on the NAIBER program and its relation to the NAIRU see: William F. Mitchell, “The Buffer Stock Policy and the NAIRU – The Path to Full Employment.” Available at: http://e1.newcastle.edu.au/coffee/pubs/wp/1997/bse.pdf

18 See: Marianna Mazzucato, “The Myth of the Meddling State.” Available at: http://www.publicfinanceinternational.org/ news/2013/06/myth-meddling-state

19 Although it should be said that there is a variety of mainstream economic theory that states that productivity growth is related to economic growth. This theory is called “endogenous growth theory” and views productivity growth as a result of investment in plant and equipment. If investment falls, say, due to demand-induced stagnation, this theory may imply that productivity growth is stifled. However, the theory takes a very long view of the link between investment and productivity and would be hard-pressed to explain any sharp productivity slowdown. We have some sympathy for this theory and believe it contains a great deal of truth – although we would note that it was articulated by post-Keynesian economists long before endogenous growth theory became fashionable – but, we shall see. We believe that the explanation for low measured productivity growth is much simpler.

20 Criticisms of so-called “Total Factor Productivity” (TFP) are legion and could easily be an essay in their own right. However, suffice it to say that TFP really measures some weighted average of wage and profit growth – nothing more, nothing less. See the excellent paper by Jesus Felipe, “What Policymakers Should Know About Total Factor Productivity,” for more on this. Available at: http://www.jesusfelipe.com/download/WHAT%20POLICY%20MAKERS%20SHOULD%20 KNOW%20ABOUT%20TFP.pdf

21 We would recommend this very clear paper for those interested in the subject further, https://www.tuc.org.uk/sites/ default/files/productivitypuzzle.pdf

Copyright © 2017 by GMO LLC. All rights reserved.

© GMO

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All