The Biggest Trends in Family Wealth

Family wealth has emerged as the financial-industry topic of this decade, akin to what estate planning was in the ‘70s, investment planning in the ‘80s, financial planning in the ‘90s, and wealth management in the ‘00s. Today family wealth advisors serve 35,000 households that all together account for more than $5 trillion in assets. Also known as family office services or multi-family offices, this service sector continues to evolve, and here we highlight some significant trends that are shaping that evolution.

A Renewed Emphasis on Integrated Financial Planning

The first trend we see in the family wealth industry is a return to the fundamentals of integrated financial planning. Indeed, the wealth management services that grew up during the past decade began as a branch of financial planning. The idea was to apply the disciplines and techniques of comprehensive, integrated planning to the needs of wealthy households. It went beyond investments to address wealth transfer, asset protection, tax planning, risk management, and charitable legacy. This integrated approach was the essence of financial planning, as Harold Evensky made clear in his groundbreaking 1997 book Wealth Management. Evensky didn’t coin the term wealth management. Nonetheless, he placed it firmly where it belonged. “I have little doubt,” he wrote, “that wealth management is a specialty of financial planning.”1 In the ensuing years, things changed. Investments came to the fore, powered by rampaging bull markets. Integrated planning—unglamorous and costly to provide even though wealthy clients benefit greatly from it—receded in importance. It became common and remains so today for many firms to offer investments and nothing else yet to call themselves wealth managers. Who needs comprehensive, integrated planning?

Well, not so fast. In a welcome turn, financial planning is making a comeback and shows signs of reasserting its rightful place as the foundation of wealth management. This trend is evidenced by a renewed emphasis on identifying and achieving the family’s financial and personal goals. It has been heralded through the use of such terms as holistic planning and goals-based wealth management. Goals are identified and prioritized, then resources are directed to each of them as needed to make sure they are accomplished within the intended time horizon. Progress toward each goal is tracked and investments supporting individual goals are put on glide paths to reduce the risk profiles as the time for spending the assets approaches.

This development is a win-win for both firms and families. Firms are focusing on the service that can add the most value—integrated planning—though they often are challenged to demonstrate that value to clients. As investments become further commoditized and compression of asset management fees persists, firms that practice integrated financial planning will be better positioned to maintain their profit margins and families will be better positioned to achieve their financial and personal goals, too.

The Challenge of Increased Complexity

Family wealth firms are grappling with the issue of increased client complexity, which plays out in two ways. First, firms must build sufficient staff expertise to give clients the professional advice they need to handle increasingly complex financial lives. That’s expensive. Second, firms must be able to gauge and put a price on a given level of complexity in order to deliver services profitably. That’s risky. Unprofitable relationships bleed a firm dry.

Why are client lives becoming more complex? Longevity is one of many contributing factors. Increased longevity has added an extra living generation to many families, complicating wealth-transfer planning and family governance and prompting families to require more services. For example, many client families now ask their wealth-management providers for help with eldercare arrangements and administration, prompting the need for additional staff expertise.

Investments are more complex and esoteric strategies require greater expertise than plain old stocks and bonds. Taxes on investment income are more complex than they were two decades ago. Tax compliance is more onerous. For example, clients with overseas income, assets, bank accounts, etc. now need assistance with Foreign Bank Account Reports and the Foreign Account Tax Compliance Act. Consider as well the trend toward multiple ownership entities to hold family assets. Use of multiple entities may be motivated by wealth-transfer, tax, or asset-protection strategies, or a family’s penchant for direct ownership of multiple businesses. In any case, these factors and more play off each other and compound complexity.

Complex clients challenge firms to price relationships correctly. Multi-family offices participating in a recent Alliance Research study published by the Family Wealth Alliance cited the pricing of complex noninvestment services as their second-greatest overall challenge related to fees and pricing (the greatest challenge was communicating value in the context of price).2

Cost and complexity of client requirements also were listed as the most important factor both in setting overall pricing policy and in coming up with a fee for a particular client.

As growing complexity ratchets up client needs, firms that can meet those needs with essential advice will prosper. The challenge for firms is to marshal sufficient resources and correctly price their services.

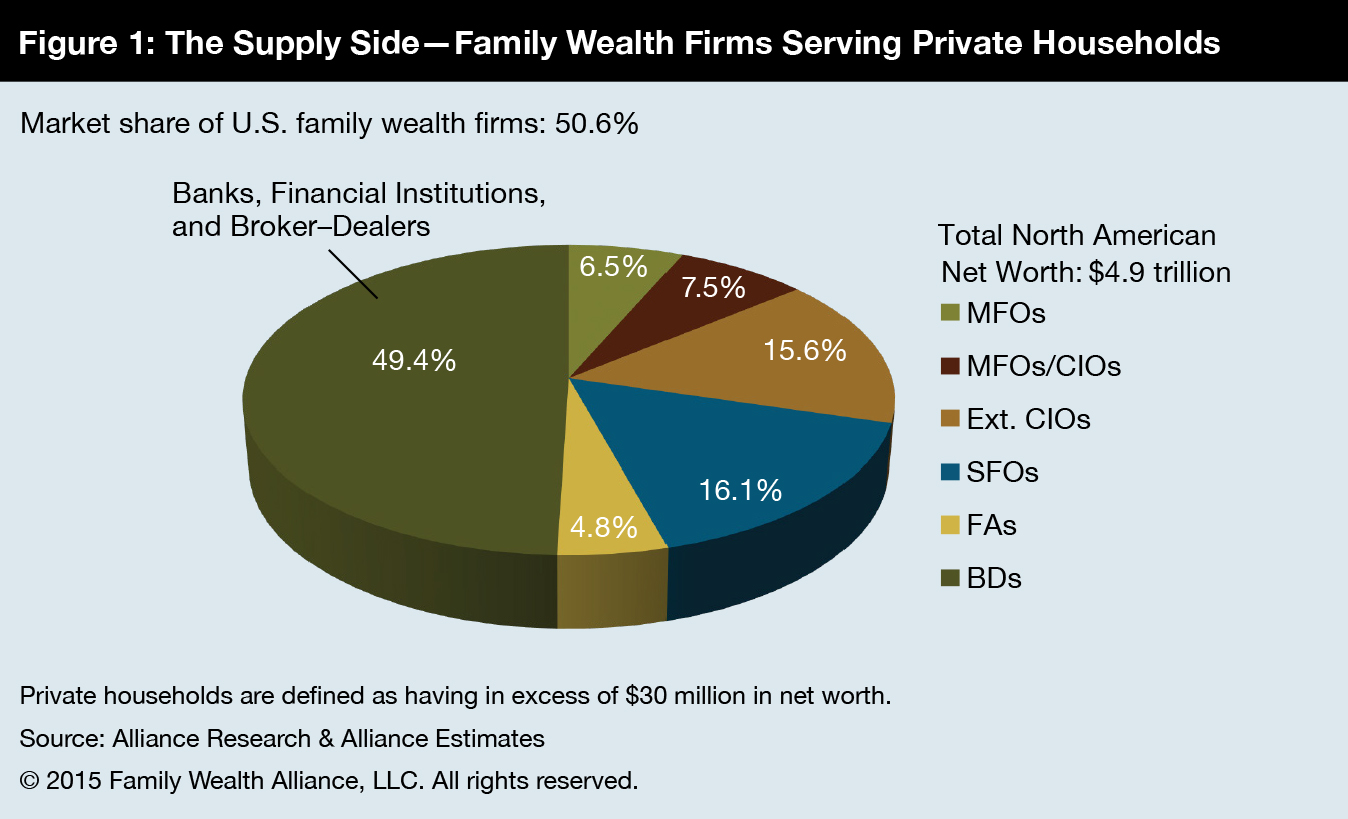

Figure 1 shows the market shares of various providers among $30 million and up households in North America.

Continue reading this article now.

Robert Casey is senior managing director of Alliance Research. He earned BS and MS degrees from the Medill School of Journalism of Northwestern University and an MBA from The Wharton School, University of Pennsylvania. Contact him at [email protected].

Thomas Livergood is founder and chief executive officer of The Family Wealth Alliance, a research and consulting organization that works with both private families and the firms that serve them. He earned a BA in liberal arts and an MBA in finance, both from Bradley University. Contact him at [email protected].

Endnotes

- See Harold Evensky, Wealth Management: The Financial Advisor's Guide to Investing and Managing Client Assets (New York: McGraw Hill Professional, 1997). The quote is from page XIV.

- Inaugural Fees and Pricing Study, Aligning Price with Value Delivered: The Challenge of Family Wealth, The Family Wealth Alliance, 2015, http://www.familywealthalliance.com/research-and-insights.

© Investment Management Consultant Association (IMCA)