Key Points

- Momentum, breadth, sentiment, earnings, valuation and macro conditions currently support a bias within the U.S. equity market toward large caps over small caps

- Small caps' 18-year outperformance phase may be ending

- Large caps' defensive nature could serve as ballast to portfolios during pullbacks

Many investors are wondering whether the stock market has come too far too fast. The latest consolidation brought the S&P 500 down only 2%, but the average stock was down more than that. Although we remain steadfast believers in this eight-year secular bull market, we have been reminding investors about the power of disciplined rebalancing around and diversification within strategic allocation. For those investors who like to take a more tactical approach, we recently changed our bias within U.S. equities toward large caps. This report details why, in a chart-heavy, word-light format.

The tides have recently shifted and now it's a confluence of factors—including momentum, breadth, sentiment, earnings, valuation and macro conditions—that we believe support a bias toward large caps over small caps. The slightly greater defensiveness of large caps could serve as ballast for portfolios if the so-far mild equity market pullback has legs.

Momentum/trend

Coming out of the early-2016 correction, small caps outperformed large caps initially; with a second burst of outperformance in the immediate aftermath of the U.S. presidential election. Since the second week in December, however, the Russell 2000/Russell 1000 (small caps/large caps) ratio has given back about half those relative gains.

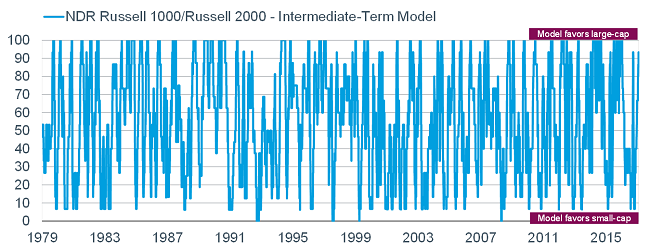

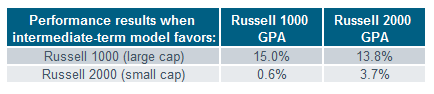

I keep tabs on the trend work from Ned Davis Research (NDR), and as you will see in the charts below, all three time periods have the models favoring large caps over small caps- with the longest-term trend model just recently confirming the short- and intermediate-term models. As you can see in the accompanying table for each, these signals have historically led to outperformance by large caps over small caps.

Source: Ned Davis Research, Inc. (Further distribution prohibited without prior permission. Copyright 2017© Ned Davis Research, Inc. All rights reserved.), as of March 10, 2017.

Market breadth

We've been highlighting the short-term deterioration in market breadth overall since U.S. stocks began their mini-consolidation phase which ushered in the month of March. Stronger breadth—which measures the price and volume action of rising stocks vs. falling stocks—tends to favor small caps over large caps since there are more small caps in the indexes than large caps. The cumulative advance/decline (A/D) lines for the S&P 500 (a large cap index) and Russell 2000 are shown in the chart below. As you can see, although the lines largely tracked each other through the end of 2016, they have diverged more recently in favor of larger caps.

Source: Bespoke Investment Group (B.I.G.), as of March 10, 2017. Each A/D line normalized using percentage of issues rather than number given differential in number of stocks in each index.

Since the Russell 2000's high on March 1, it's down a bit over 3%. At down only 2.25% mid-last week, there were already more 52-week lows than highs; which is unusual. In fact, since 1995, there were only six prior instances when this pattern occurred. As you can see in the table below, looking at subsequent six-, and 12-month returns, small cap stocks tended to see meaningful relative weakness, with high "relevance" scores (see footnote).

Source: SentimenTrader, as March 10, 2017. Relevance > 95% suggests significance; Risk = average max loss; Reward=average max gain.

Sentiment

One of my favorite sentiment indicators is the NDR Crowd Sentiment Poll, because it's an amalgamation of seven distinct and separate indicators. It is presently showing excessive optimism—based largely on attitudinal, not behavioral, measures of investor sentiment. Frothy sentiment tends to be more negative for small caps than large caps; and the strongest signal for large caps tends to come when optimism comes off the boil- which has already begun courtesy of the market's mild pullback of late.

Behavioral measures of investor sentiment have only just begun to shift—and fund flows have been decidedly toward the larger cap passive exchange-traded funds (ETFs). There has been some institutional rotation as well back into large cap U.S. equities, likely aided by the greater liquidity associated with large caps.

Macro conditions

Small cap stocks are generally more economically-sensitive and tend to outperform in the earlier stages of economic recoveries/expansions. As such, their valuations tend to rise to a point they become rich relative to large caps in the more mature phase of the expansion (more on that later in this report). In this more mature phase, interest rates are starting to rise at a more rapid clip. Note: We expect the Fed to raise rates at this week's meeting.

A strong dollar has historically (and recently) benefitted small caps over large caps; as the former have a greater domestic-orientation and are therefore less exposed to weaker exports which typically accompany a strong dollar. However, a strong dollar is being accompanied by higher interest rates here in the United States, which tend to benefit large caps to a greater degree. In fact, historically the offset has been strong enough to put large caps in the leadership position.

Earnings/valuations

After several flat-to-negative quarters for earnings growth, large caps (and mega-caps) have seen surging earnings growth rates. The table below shows the progression over the past year, broken down into capitalization zones.

Source: The Leuthold Group, as of March 7, 2017.

For the stock market though, valuations on forward expected earnings are more relevant. The table below shows the current price/earnings (P/E) ratios for each capitalization range on both expected 2017 and 2018 operating earnings. Presently, small caps are trading at a 10% premium to large caps on 2017 earnings and 6% on 2018 earnings.

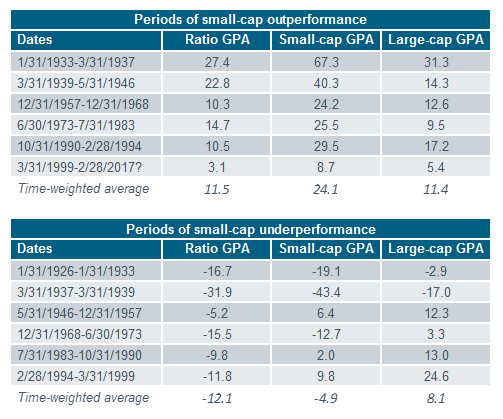

You can see two additional time periods highlighted. June 1983 represents the peak of the 1973-1983 small cap leadership run, when small caps achieved a relative P/E premium of 10% (like today). Small caps did however achieve an even higher 14% premium at the end of the cyclical run from 1999 to 2006. The largest discount ever for small caps was in December 1999, as seen below, which was at the height of the dot com large-cap-favoring bubble.

Source: The Leuthold Group, as of March 7, 2017. P/E calculations use operating earnings, which exclude extraordinary items and discontinued operations.

Technicals

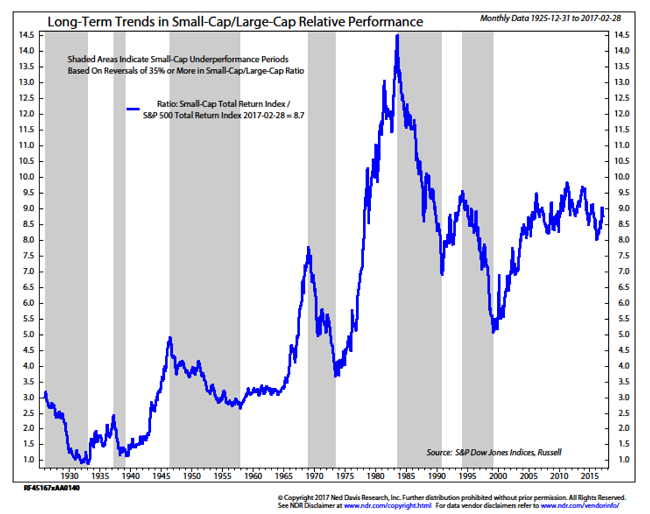

I'll conclude with a compelling chart highlighting the long-term cycles of small and large cap out performance periods (the shaded areas highlight secular periods when large caps were outperforming). We are currently in the longest stretch of small cap outperformance in history. It began in 1999, and assuming the recent high doesn't represent the ultimate cycle high, it's lasted for nearly 18 years (with some cyclical pullbacks along the way).

Note though the 23-year high made in 2011; which has served as meaningful resistance for small caps since which time they've been making a series of lower highs and lower lows, a technical warning sign as detailed recently by NDR.

Source: Ned Davis Research, Inc. (Further distribution prohibited without prior permission. Copyright 2017© Ned Davis Research, Inc. All rights reserved.). December 31, 1925-February 28, 2017.

In sum

There is some risk that small caps are simply just taking a breather after their recent run of outperformance. However, we think the weight of the evidence—including technical, macro, earnings/valuation, breadth and sentiment—suggests we could be entering an environment where large caps shine relative to small caps.

Important Disclosures

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

(0317-WEXB)

© Charles Schwab

© Charles Schwab

Read more commentaries by Charles Schwab