Since the election we’ve heard the rally in stocks characterized as a “Trump Trade” or a “reflation” trade. We think there is a really important element missing from this analysis that could change very quickly over the next several weeks.

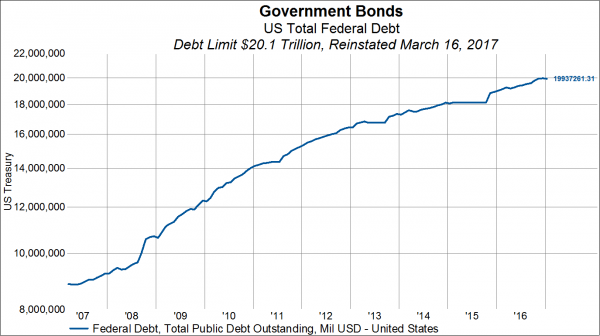

On March 16, 2017 (the day after the Federal Reserve is expected to raise interest rates for the third time) the US Federal debt ceiling comes back into law at $20.1 trillion. At the end of January, total federal debt was $19.93 trillion, and in real-time using US Debt Clock (http://www.usdebtclock.org/) it is $19.93 trillion.

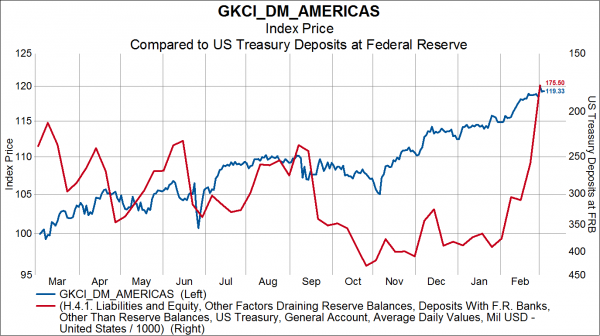

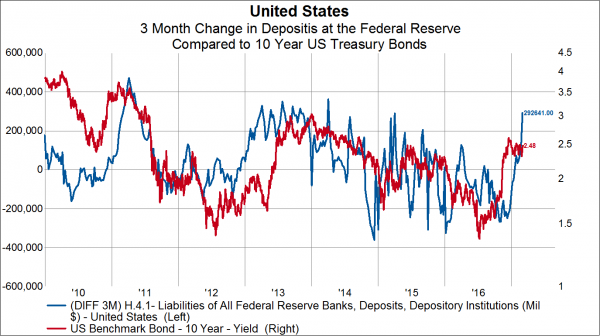

In anticipation of the debt ceiling coming back into force, since November, US Treasury deposits held at the Fed have dropped from over $400 billion to around $175 billion, unleashing over $200 billion of liquidity into the markets. In the chart below, one can see how US stocks leapt one week after the peak in US Treasury deposits at the FRB.

This has served to create the appearance that the Federal Reserve has been easing lately. Since 2014, the Fed has been slowly starting to reign in monetary accommodation. First it was by tapering, then in December 2015, the Fed began its current rate hiking cycle. Now, the Fed is still using the federal funds rate as the reference rate for monetary policy. This means that in order to lift the fed funds rate, the Fed needs to trim excess reserves in the banking system.

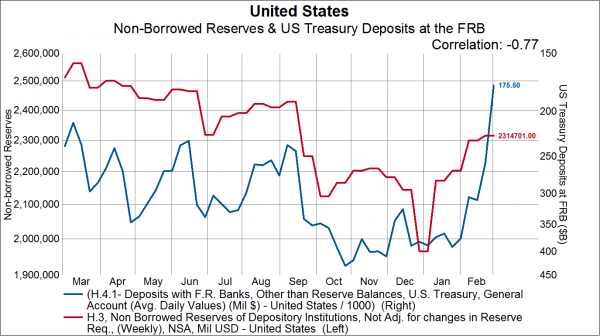

As can be seen in the chart below, the increase in commercial bank reserves is basically a mirror image of the US Treasury drawing down its balance with the Fed. The net effect of this is an unintended liquidity injection into the economy. To be clear, the increase in bank reserves is entirely a function of the US Treasury making preparations to hit the debt ceiling in the next couple months.

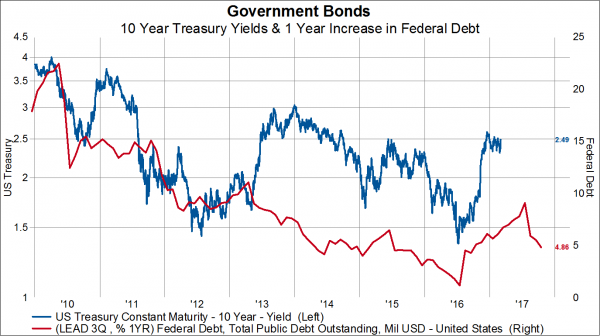

Taking a step back, it is important to understand the relationship between federal debt and interest rates. The suspension of the debt ceiling in the fall of 2015 led to an explosion in federal debt in 2016—helping to propel the economy (and likely in an effort to help the executive branch stay in Democrat control). This isn’t to say economic growth wasn’t for real in 2016, but it was heavily influenced by a surge in federal debt. If we move the year over year change in federal debt forward by three quarters, there is a very good relationship with the US 10 Year Treasury. The peak in debt growth several months ago could mark the near term peak in interest rates.

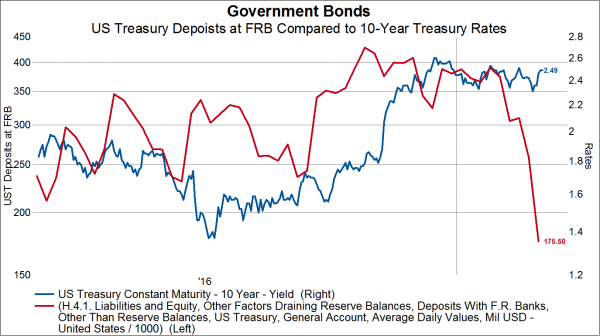

In the next chart, we show commercial bank deposits at the Fed overlaid on 10 Year US Treasury rates. The close relationship is hard to mistake.

Going a step further, the recent precipitous drop in US Treasury deposits at the Fed could telegraph a significant decline in interest rates this year. Why? Let’s say the debt ceiling is raised and the US Treasury wants to rebuild its account at the Fed similar to how it operated in 2011. The US Treasury will then issue a bunch of bonds, stick the proceeds at the Fed and basically remove several hundred billion in liquidity from the markets. This will manifest itself in lower commercial bank deposits at the Fed and a reduction in banking liquidity.

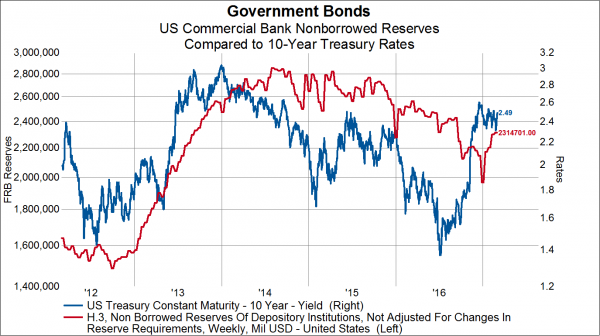

With the Fed set raise interest rates on March 15 and the debt ceiling set to kick in the next day, we think there is reason to question the recent appearance of abundant liquidity that has pushed up interest rates and supported stocks. Experience over the last few years is that each major reduction in commercial bank reserves leads to a lower interest rates and a stumble in stocks. We worry that we may be on the cusp of a difficult Ides of March.

© GaveKal Capital

Read more commentaries by GaveKal Capital