By Peter Chiappinelli, CFA; GMO LLC

The trends are clear. 2016 was the year in which the investment community warmly embraced passive portfolios. Our worry, however, is that investors are feeling a false sense of security, particularly with passive bond portfolios–namely those funds and Exchange Traded Funds (ETFs) linked to a common benchmark, the Bloomberg Barclays U.S. Aggregate Bond Index (the Agg). There is nothing passive about this index, and we would argue it is aggressively taking on more risk at the worst possible time. There are three main reasons for our concern: the simple math of bond duration; the changing composition of the index; and the very logical financing behavior of corporate borrowers.

Bond math and duration

Without doing a rehash of intricate bond math, duration is an important calculation of bond risk. Though it has many variants, at its root duration measures the sensitivity of a bond’s price to a shift in yields. For example, a bond (or a bond portfolio) with a duration of 5 years means that for every 1% shift upwards in yields, there is a 5% drop in the price of the bond. Duration is measured in years because it is a function of the timing and magnitude of a bond’s cash flows (coupons and principal repayment): the more distant the cash flows, the higher the sensitivity (i.e., higher risk) to a change in interest rates, all else held equal. The cleanest example of this is the 30-year zero-coupon bond, which pays a single massive cash flow 30 years down the road, and therefore this bond has a duration of exactly 30 years. There are no coupon payments along the way that would dampen its sensitivity to a change in yields. Generally speaking, the smaller the coupon, the higher the duration (and vice versa); the longer the maturity, the higher the duration (and vice versa). That’s just how the math of bond risk works.

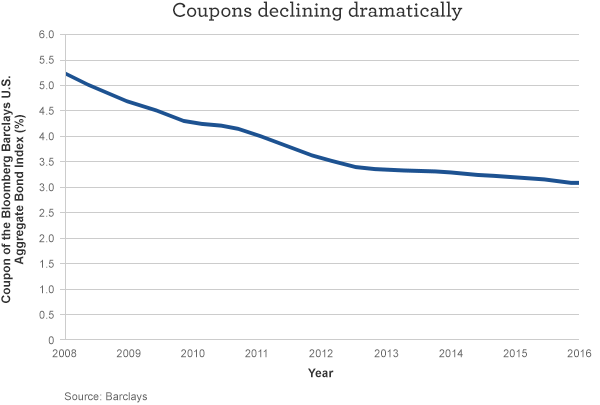

Unfortunately for investors in passive bond portfolios or ETFs tied to the Agg, bond math is making this “safer” bond portfolio much riskier than it was even a few years ago. It is now much more sensitive to a possible rise in bond yields (as we saw in November) due simply to a lower “cushion” of coupons. As shown in the chart below, coupons have dropped dramatically since the Financial Crisis of 2008 and the introduction of Quantitative Easing by the Federal Reserve (Fed). For many years leading up to 2008, the Agg happily paid its investors a healthy coupon of over 5%, but today it is a measly 3%, a number that is among some of the lowest ever recorded. This is problem number one.

Changing composition of the Agg

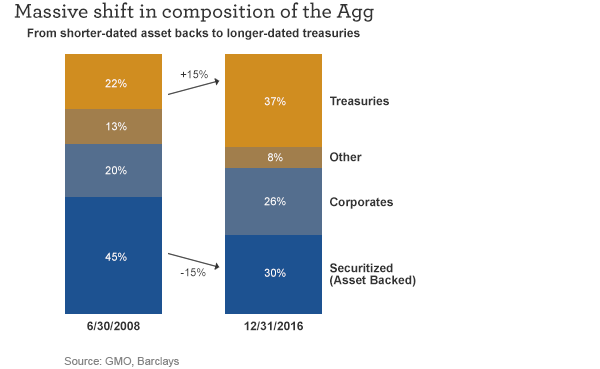

Problem number two is that the Agg has dramatically changed its stripes since the Financial Crisis. Eight years ago, the largest bond sector was securitized loans (e.g., asset-backed securities, mortgage-backed securities), and most of these types of securities have shorter maturities and duration. Today, longer-dated Treasuries are now the dominant sector of the Agg, while securitized bonds have dropped off significantly. This, again, has shifted both the maturity and duration of the Agg upward.

Corporate financing behavior

In June of 2016, Apple issued its first-ever 30-year bond … and it was NOT because Apple needed the cash! It was all about locking in unbelievably low financing costs for an extended period of time. Apple’s CFO did what any reasonable CFO would do in the face of historically low borrowing costs: Borrow as much as you can for as long as you can. It is logical to exploit a marketplace starving for yield. The problem, however, is that many, many CFOs are doing the same thing and this behavior is changing the composition of the Agg as more and more corporations shift their financing to longer-maturity bonds. The corporations are selling … and the Agg is buying! Or, rather, YOU are buying these longer-dated riskier bonds if you own a passive bond portfolio or ETF.

The Net-Net: More risk at the worst possible time

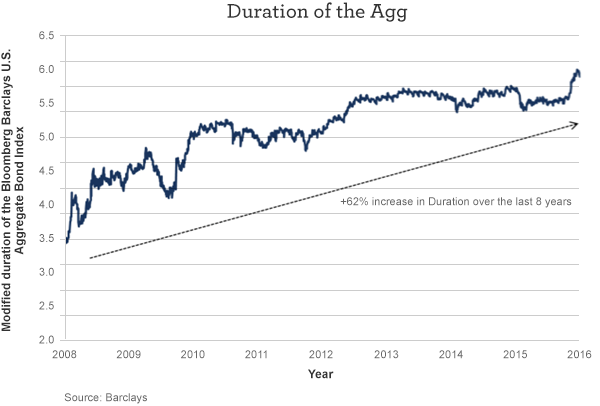

For the last 8 years in particular, the yield on the 10-year U.S. Treasury has been steadily decreasing. In July of 2016, just a few short months ago, it hit 1.37%, the lowest yield ever recorded in U.S. history. While of course it was possible that rates could have gone lower, prudence dictated that this was a period to be reducing risk by either shortening duration or reducing bond exposure. What has the Agg been up to these last few years? Just the opposite. The chart below clearly shows this to be the case.

The bond math of lower coupons, the changing composition of the Agg, and the issuance of longer-maturity bonds by corporate America all conspired to increase risk, at possibly the worst time. By any reasonable fiduciary standard, this was a time to be reducing duration, yet the Agg, and the passive bond portfolios and ETFs tied to it, has seen a 62% increase in duration over the past 8 years. There is nothing passive about the Agg–it has actually become more aggressive! Be careful.

Please visit our blog, AdvantageVoice, for additional viewpoints from Wells Fargo Asset Management’s investment strategists, portfolio managers, and practice management experts. You can also follow us on Twitter at @WFAssetMgmt for real-time updates. Are you an advisor or institutional investor? Check out our website for investment professionals.

The views expressed are as of 2-13-17 and are those of Peter Chiappinelli, CFA; GMO LLC, and Wells Fargo Funds Management, LLC. The information and statistics in this report have been obtained from sources we believe to be reliable but are not guaranteed by us to be accurate or complete. Any and all earnings, projections, and estimates assume certain conditions and industry developments, which are subject to change. The opinions stated are those of the authors and are not intended to be used as investment advice. The views and any forward-looking statements are subject to change at any time in response to changing circumstances in the market and are not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally, or any mutual fund. Wells Fargo Funds Management, LLC, disclaims any obligation to publicly update or revise any views expressed or forward-looking statements.

Wells Fargo Asset Management (WFAM) is a trade name used by the asset management businesses of Wells Fargo & Company. Wells Fargo Funds Management, LLC, a wholly owned subsidiary of Wells Fargo & Company, provides investment advisory and administrative services for Wells Fargo Funds. Other affiliates of Wells Fargo & Company provide subadvisory and other services for the funds. The funds are distributed by Wells Fargo Funds Distributor, LLC, Member FINRA, an affiliate of Wells Fargo & Company. Neither Wells Fargo Funds Management nor Wells Fargo Funds Distributor has fund customer accounts/assets, and neither provides investment advice/recommendations or acts as an investment advice fiduciary to any investor.

Not FDIC Insured • No Bank Guarantee • May Lose Value

© Wells Fargo Asset Management