If an issuer defaults, insurance firms can make sure your payments don’t stop

Puerto Rico’s recent history of municipal bond defaults has highlighted the potential benefits of a niche part of the municipal (muni) bond market — insured municipal bonds. Insured munis have accounted for only around 6% of all municipal issuances in the past three years,1 but we believe they can play a role for investors who want assurance that their bonds’ interest and principal will be paid on time — even if the issuer defaults.

What are insured muni bonds?

Municipal bond insurance companies issue insurance policies on muni bonds, which guarantee that the insurance company will make timely interest and principal payments on those bonds in the event that the issuer defaults. The cost of the policy is reflected in the bonds’ yields — an insured bond will typically have a somewhat lower yield than an identical uninsured bond. However, the true value of the policy can be seen when an issuer gets into financial trouble.

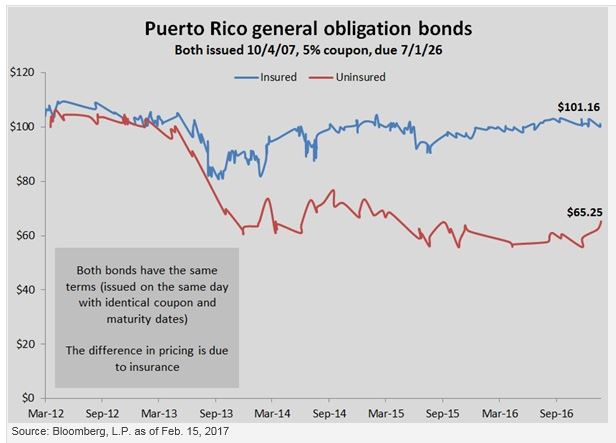

The chart below shows pricing for two Puerto Rico general obligation bonds with identical terms — but one is uninsured and the other is insured by Assured Guaranty. The insured bonds performed over 35 points better than the uninsured bonds following Puerto Rico’s defaults.

Who insures muni bonds?

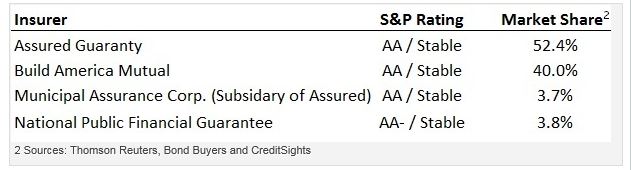

A key concern for investors, of course, is that these insurance companies are financially stable. Even after the Puerto Rico defaults, their credit ratings indicate that they are.

Two municipal bond insurers with exposure to Puerto Rico — Assured Guaranty (AA/stable) and National Public Finance Guarantee (AA-/stable) — had their ratings affirmed by Standard & Poor’s (S&P) in 2016. Build America Mutual (AA/stable), a municipal bond insurer with no exposure to Puerto Rico, also had its ratings affirmed by S&P in 2016.

How does the insurance process work?

Bonds can be insured when they are issued, or they can become insured after they are issued. At Invesco Unit Trusts, we carefully assess the fundamentals of bonds that are already insured, and we also seek to leverage our strong relationships with broker-dealers and municipal bond insurance firms to create unique and attractive opportunities for muni bond investors. How?

- We work with broker-dealers to identify attractive, favorably priced bonds that are not insured.

- We identify insurance companies that are willing to insure that specific bond, and seek to negotiate the best price possible for the policy.

- We then purchase the “new” insured bond from the broker-dealer.

Talk to your advisor

Interested in the security that insured municipal bonds can provide? Talk to your financial advisor and explore the Insured Municipals Income Trust, a diversified portfolio of insured muni bonds that provides investors with professional bond selection and ongoing active surveillance based on the underlying credit quality of each municipal issuer.

1 Source: CreditSights, “Bond Insurance: 2016 Market Share Rankings,” Feb. 15, 2017

Greg Rawls, CFA, CAIA

Investment Research Analyst

Greg Rawls is an Investment Research Analyst on the Unit Trust Investment Research Team, responsible for investment recommendations, surveillance and research.

Mr. Rawls has seven years of industry experience, including equity and corporate debt research. He has a diverse knowledge base with experience in equity, private equity and corporate fixed income securities.

Mr. Rawls earned a BS degree in finance from Marquette University, where he was a member of the Applied Investment Management Program, and is currently pursuing an MS degree in finance from the University of Notre Dame. He is a CFA charterholder and a CAIA charterholder.

Important information

Blog header image: Oil and Gas Photographer/Shutterstock.com

Coupon is the annual interest rate paid on a bond, expressed as a percentage of the face value.

Municipal securities are subject to the risk that legislative or economic conditions could affect an issuer’s ability to make payments of principal and/or interest.

Puerto Rico’s economic problems increase the risks associated with investing in Puerto Rican municipal obligations, including the risk of potential issuer default, and heighten the risk that the prices of Puerto Rican municipal obligations, and the fund’s net asset value, will experience greater volatility. See the prospectus for more information.

There is no assurance that a unit investment trust will achieve its investment objective. An investment in this unit trust is subject to market risk, which is the possibility that the market values of securities owned by the trust will decline and that the value of trust units may therefore be less than what you paid for them. This trust is unmanaged. Accordingly, you can lose money investing in this trust.

An investment in a trust should be made with an understanding of the risks associated therewith, such as the inability of the issuer or an insurer to pay the principal of or interest on a bond when due, volatile interest rates, early call provisions and changes to the tax status of the bonds. As interest rates rise, bond prices fall.

The value of the bonds will generally fall if interest rates, in general, rise. Given the historically low interest rate environment in the US, risks associated with rising rates are heightened. The negative impact on fixed income securities from any interest rate increases could be swift and significant. No one can predict whether interest rates will rise or fall in the future.

A bond issuer may cease to be rated or its ratings may be downgraded. Such action may adversely affect the value of the bonds in the trust and the value of the units.

The insurance provides coverage for the bonds held by the trust, not on units of the trust.

Ratings are based on S&P. A credit rating is an assessment provided by a nationally recognized statistical rating organization (NRSRO) of the creditworthiness of an issuer with respect to debt obligations, including specific securities, money market instruments or other debts. Ratings are measured on a scale that generally ranges from AAA (highest) to D (lowest); ratings are subject to change without notice. NR indicates the debtor was not rated and should not be interpreted as indicating low quality. If securities are rated differently by the rating agencies, the higher rating is applied. Credit ratings are based largely on the rating agency’s investment analysis at the time of rating, and the rating assigned to any particular security is not necessarily a reflection of the issuer’s current financial condition. The rating assigned to a security by a rating agency does not necessarily reflect its assessment of the volatility of a security’s market value or of the liquidity of an investment in the security. For more information on the rating methodology, please visit http://www.standardandpoors.com and select “Understanding Ratings” under Ratings Resources on the home page.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. Each entity is an indirect, wholly owned subsidiary of Invesco Ltd. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC, investment adviser. Invesco PowerShares Capital Management LLC (PowerShares) and Invesco Distributors, Inc., ETF distributor, are indirect, wholly owned subsidiaries of Invesco Ltd.

©2017 Invesco Ltd. All rights reserved.

Insured municipal bonds may offer added security for investors by Invesco