Not long ago, we suggested that investors who wanted to make their equity portfolios less volatile add a dash of high-yield bonds. There’s a similar low-volatility strategy available to high-yield investors: shorten duration and focus on quality.

As noted in a previous blog, high yield, when combined with equities, can reduce overall risk without sacrificing much return. This is partly because high-yield bonds provide a consistent stream of income that helps to offset stocks’ higher level of volatility.

But what about limiting the volatility associated with high yield? In today’s uncertain environment, that question is top of mind for many income-oriented bond investors who typically invest in the high-yield market. The answer, in our view, is to narrow your focus to shorter-maturity BB- and B-rated bonds.

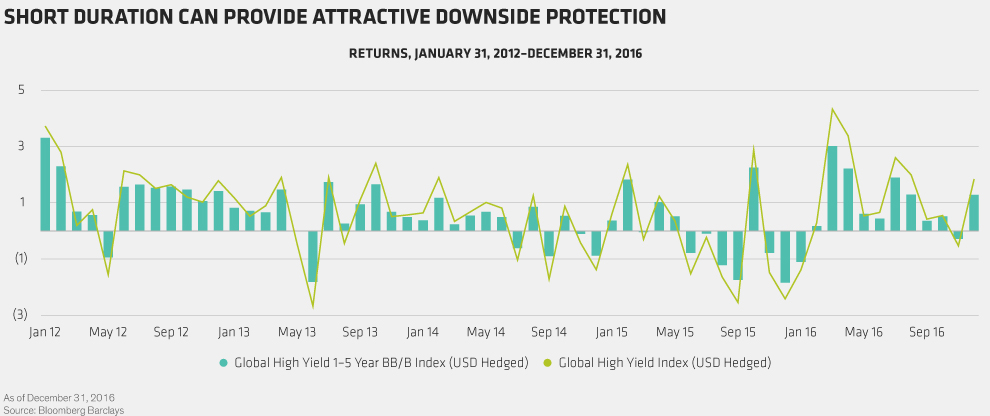

The relationship between strategies that rely on high-quality, short-duration bonds and those that invest in the broader high-yield market is much like that between broader high yield and equities. Over time, short-duration high-yield strategies have dampened volatility and held up better in down markets than has a broad high-yield allocation, while still capturing most of the market’s returns when times are good (Display).

Why does this combination work so well? First, let’s consider duration, a measure of a bond’s sensitivity to changes in yield. In general, bonds are highly sensitive to yield changes—when yields rise, prices fall. The shorter the duration, the less damage a rise in yields will do.

That’s important today because there’s plenty of room for yields to rise. In US high yield, average yields and credit spreads—the extra yield that high-yield bonds offer over comparable government bonds—are at multi-year lows. If higher inflation prompts the Federal Reserve to start raising interest rates more aggressively, slowing overall growth, yields could rise and spreads could widen quickly.

Shortening duration, though, is only half the battle. Credit risk in a short-duration strategy can still be substantial, particularly with the US credit cycle well into its ninth year. That’s why limiting exposure to low-quality CCC-rated “junk” bonds is critically important. It’s the interplay of the two—short duration and high quality—that accounts for the superior downside protection.

High-yield investors who rely on their portfolios to generate income understand that they must take some risk to get returns. That makes abandoning high yield altogether a risky move. While sizable corrections aren’t unusual, the market tends to bounce back quickly.

A better approach, in our view, is one that maintains exposure while limiting downside risk. Over time, high-quality, short-duration strategies have done just that.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.