North American equities led the way in 2016, providing double digit returns and bolstering investor confidence. As expected, the recent strength has naively led investors to flock into US equity funds in what may possibly be the tail end of US equity dominance over global equity markets.

This new wave of investor enthusiasm will inevitably pressure Investment Advisors to tilt more aggressively toward North American equities in the coming year. In this analysis we examine where US equity markets lie in terms of both cyclicality and valuation against other global equity markets, and assess where the best opportunities may lie going forward. We hope this article arms Advisors with the tools and data necessary to help their clients avoid the typical behavioural flaws that lead to poor timing and poor long-term returns. We make the case that this is best achieved via a thoughful, globally-diversified asset allocation.

ONE MARKET TO RULE THEM ALL

If you are a forward-thinking Advisor with a balanced and well diversified global portfolio, you have not been rewarded for your diligence and thoughtful diversification over the last 3, 6, and 9 year periods. In fact, there’s only been one game in town: US Equities. This has been an incredibly unsusual time for global markets as pretty much any other asset class has had low or negative returns since the Housing Bubble burst.

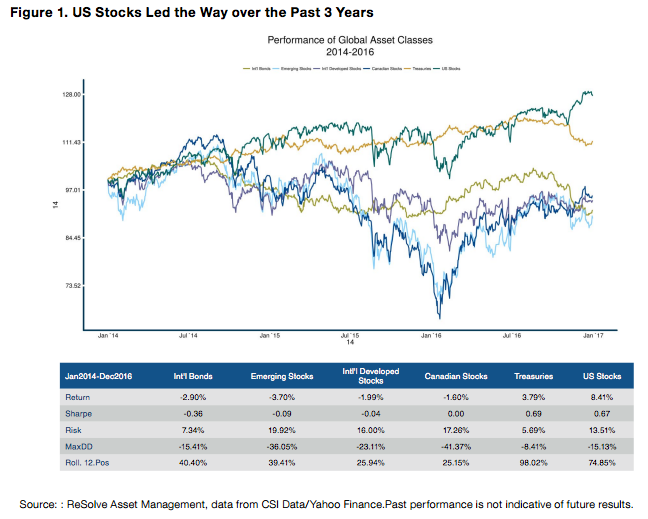

To illustrate, let’s start by analysing a wide variety of asset classes over the most recent 3-year period. Figure 1 shows that the only market that has delivered material returns in US dollar terms has been US equities. While US Treasuries also produced positive returns, they trailed US equities by a substantial margin. Note that Canadian equities delivered negative returns during this period.

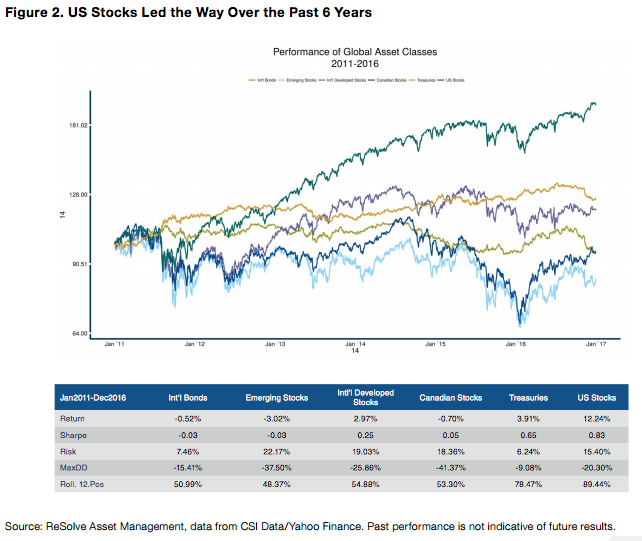

Next, we examine the most recent 6-year period. What we observe is the same market structure, but with an even more pronounced dynamic, as US equities annualized at over 12%, beating the next best asset class (again, US Treasuries) by over 7% per year. And yet again, Canadian equties delivered negative returns.

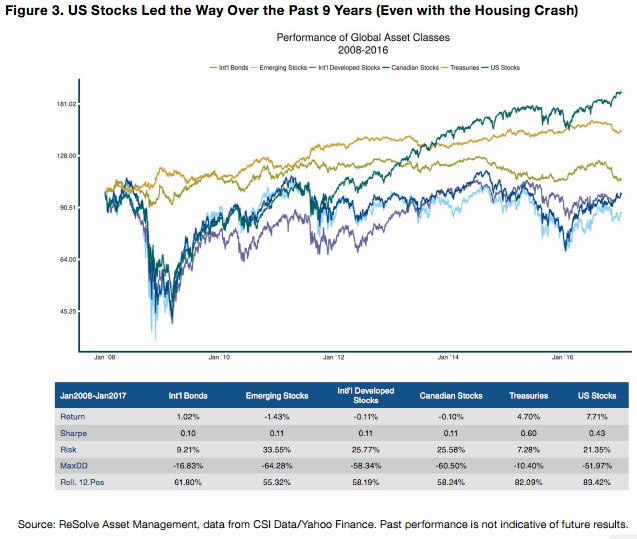

Finally, we examine the most recent 9-year period, starting from the Housing Crash in 2008. Here we see that US stocks were the only equity asset class with positive returns, returning 7.7% annualized (albeit with a 52% maximum drawdown).

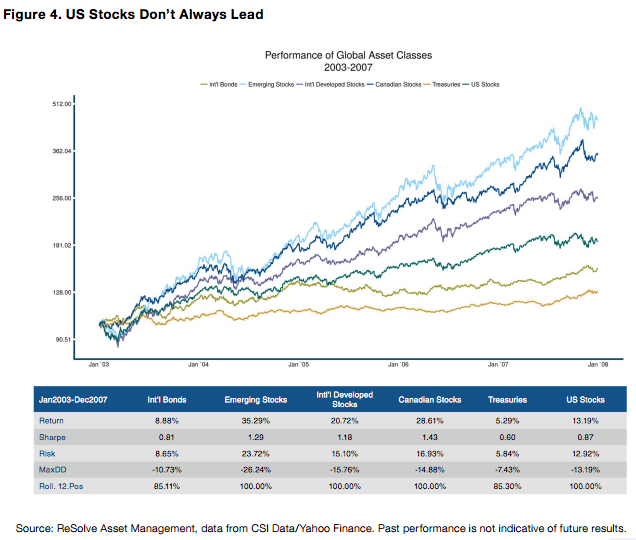

While it may feel like this lengthy period of US stock leadership and return disparity is the new normal, it’s important to remind ourselves that global asset class leadership inevitably rotates. As an important reminder (of a time most investors have likely forgotten), US stocks were a significant laggard compared to other global asset classes over the five-year period leading up to the Housing Crash.

During this period, US stocks earned 13.2% annualized. At the same time, Emerging stocks earned 35.3%, Canadian stocks earned 28.6%, and International Developed stocks earned 20.7%.

WHERE DO WE STAND IN TERMS OF CYCLICAL HISTORY AND PERFORMANCE DIFFERENTIALS?

While what we have addressed thus far is an important contextual reminder of the value of diversification, its fair to wonder if this is the right time to rotate away from North American equities. For clues, we examine the mounting evidence that, after many years of US equity leadership (this is soon to be longest bull market run in history), there is likely change afoot.

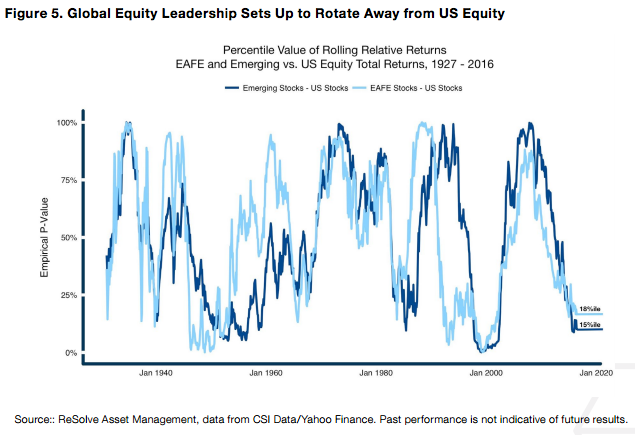

To put this sustained US outperformance into perspective, we calculated the differential between 5-year rolling equity total returns from International Developed markets (EAFE) and Emerging markets relative to US stocks going back to 1926.

The performance of International Developed stocks relative to US stocks is in the 18th percentile over the past 5 years, and the relative performance of Emerging stocks is in the 15th percentile. To translate, this means that the current proportion of outperformance that we observe from US stocks relative to both International and Emerging Market stocks has happened less than 20% of the time in the last 90 years.

While there are too few observations to make statistically significant conclusions from this analysis, the chart clearly shows that this performance differential oscillates over periods of 5-10 years. That we’re now 9 years into a period of extreme US equity leadership, and the return differential is near its historical inflection point, suggests international and asset class diversification is likely to pay off handsomely in the next half-decade.

HOW EXPENSIVE IS THE US MARKET AGAINST GLOBAL ALTERNATIVES?

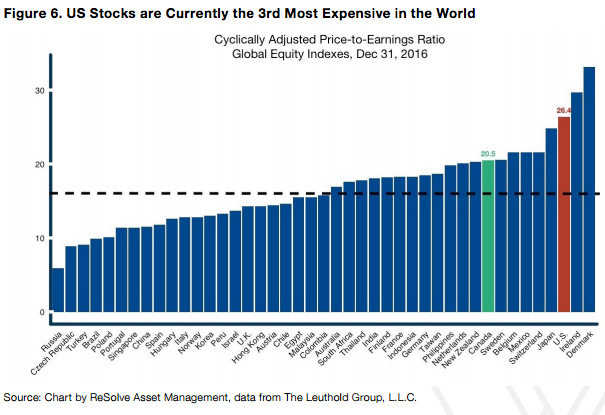

When US markets dominate other global asset classes by such a large magnitude, it often means US equities have become quite expensive relative to other global markets. And indeed, examination of the Shiller Cyclically Adjusted Price-to-Earnings ratio (CAPE) verifies that US stocks are now very expensive.

US stocks are the third most expensive market in the world, with a CAPE ratio fully 50% higher than average, and the second most expensive it has ever been. Canada is 9th most expensive, putting both in the top quintile.

A 10-year valuation ratio – which intentionally smoothes out business cycle effects – does not necessarily suggest an impending market crash. However, several studies show that this ratio is a good predictor of future returns over forecast horizons of 7-15 years. It’s fair to assume that future returns to US stocks face significant headwinds, and are likely to experience performance reversion.

HOW SHOULD YOU POSITION YOUR PORTFOLIO FOR THE REVERSAL?

Investors using the past 3-9 years to inform their investment decisions might conclude that international investing is a mug’s game, diversification is dead, and that they should throw all their savings at North American stocks. History shows that this period is an anomaly, and that strategies prioritizing global diversification across regions and asset classes deliver better performance over longer periods of time, with less risk.

While this analysis clearly points to likely lower returns for US equities over the next market cycle the question on everyone’s mind is which global asset class is going to take the lead? Gold? German Bunds? Europe? Emerging markets?

The reality is that nobody knows.

This being the case, thoughtful advisors need to consider transitioning into a well-diversified set of global asset classes in a risk-balanced way. If this is not your forte, it may be a good time to partner with a specialist global asset allocation firm that can help you create risk-responsive portfolios, identify emergent trends early on, and navigate through these troubled waters.

ReSolve Asset Management offers Global Tactical Asset Allocation strategies designed to deliver an absolute return character by dynamically allocating across global asset classes.

© ReSolve Asset Management

Read more commentaries by ReSolve Asset Management