As earnings season rumbles on, analysts remain fixated on the bottom line of company reports. But earnings tell only a partial story. There’s a better way to identify businesses that can generate long-term growth.

Just look at the news headlines and it’s clear that earnings are what matters most for many investors. “Time Warner earnings beat expectations.” “Whole Foods slides after missing on earnings.” “Coca-Cola earnings retreat 5%.”

ARE EARNINGS THE BEST BAROMETER?

Yet earnings might not really be the best barometer to gauge a company’s true economic prospects. Earnings can’t tell you how skillfully a management team deploys capital. They offer no insight into the quality of a company’s profit streams. And earnings alone can’t really identify companies that can generate long-term value for shareholders, in our view.

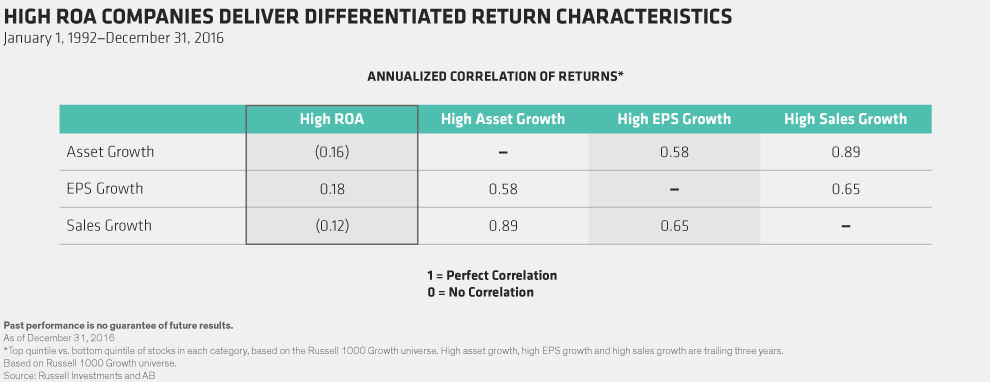

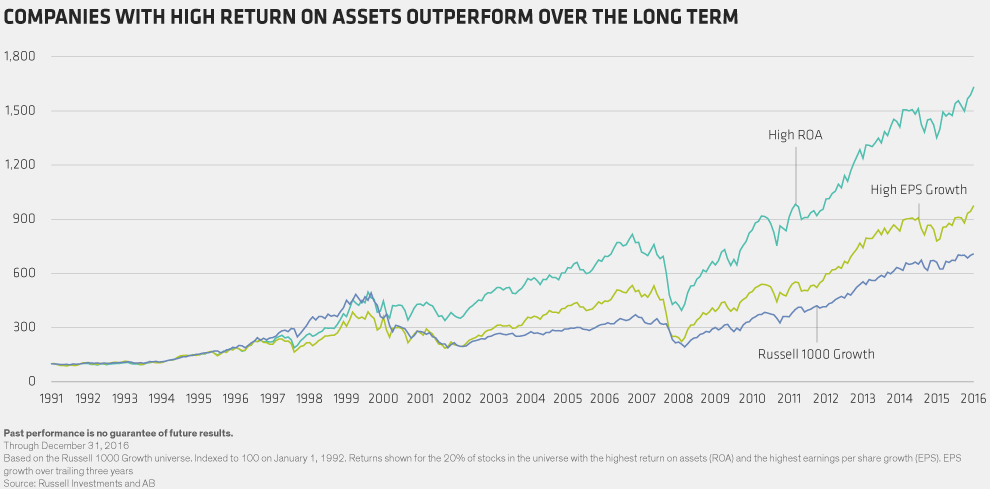

Fundamental returns—which are a way of looking at business profitability—are much more insightful. By putting returns on invested capital (ROIC) or return on assets (ROA) at the center of company research, we believe investors can discover whether a company is investing intelligently to generate its profits. That’s why US stocks with high ROA have consistently outperformed stocks with high earnings per share (EPS) growth—as well as the Russell 1000 Growth Index—over more than three decades (Display).

COST OF CAPITAL MATTERS

Conventional wisdom on Wall Street suggests that investor sentiment about future earnings determines a company’s stock price. We disagree. What we think matters most is the amount of capital—financial or physical—that a firm deploys to generate its earnings. After all, any dollar management invests is a dollar shareholders could have invested for themselves. So a firm’s ROIC must exceed a certain threshold, the so-called “cost of capital,” for its stock to perform well over the long term.

Cost of capital is elusive. Yet although it isn’t listed in a company’s reports, its influence is everywhere. For example, when a company’s shares plunge after announcing a large acquisition that’s “accretive” to EPS, investors are really reacting to an inefficient investment decision. Without a focus on cost of capital, companies seek to enhance value using all sorts of tricks—from aggressively buying back shares to rapidly growing assets. Ultimately, companies pursuing low-return/high-growth strategies like these are punished for their recklessness.

DON’T IGNORE THE BALANCE SHEET

Earnings are much more visible. But earnings growth can be driven by things that have nothing to do with a company’s business, such as a cyclical industry recovery, accounting changes or financial engineering. What’s more, earnings ignore balance sheets—which can provide vital signals on business health and long-term growth.

Under Armour (UA) is a case in point. From the end of 2013, the sportswear company’s stock rallied as earnings advanced by 20% a year on strong sales. But many analysts missed something: a 35% annual increase in UA’s asset growth. As a result, marginal returns were diminishing and profit margins were shrinking on every incremental dollar of sales. ROA dropped from over 16% at the end of 2013 to about 11% in 2016 (Display, left chart), while UA’s asset base doubled. Profit growth wasn’t keeping up and could not fund its expanding asset base (Display, right chart). Its return on incremental capital fell well below its cost of capital at 7%. In other words, the company destroyed value by growing earnings—and making bad investments. Eventually, the market caught up and the stock price declined from late 2015.