This week I was in beautiful Argentina with a diverse team of investors and mining executives, including my good friend Frank Giustra; Ian Telfer, founder of Silver Wheaton and current Chairman of the Board of Goldcorp, which has sizeable investments in Argentina; and Serafino Iacono, Chairman of the Board of Pacific Exploration & Production (formerly Pacific Rubiales), which is active throughout South America. Together we toured various natural gas and crude oil mining projects in Tierra del Fuego, Mendoza and Santa Cruz, where we had the opportunity to speak with Governor Alicia Kirchner, elder sister to former Argentinian president Néstor Kirchner.

|

One of the highlights of the trip was meeting with current president Mauricio Macri in Buenos Aires. Macri, as you might know, was elected in late 2015 on his credentials as a businessman and former mayor of Buenos Aires. His administration ends more than a decade of socialist rule by Kirchner and his wife Cristina Fernández, who was indicted this past December on corruption charges.

Even with Macri at the helm, corruption remains a problem in Argentina. The South American country currently ranks 95th in Transparency International’s 2016 Corruption Perceptions Index.

But economic conditions are improving. After contracting 1 percent in 2016, country GDP is expected to grow as much as 2.8 percent this year. Macri’s mission to make Argentina great again has already led him to abolish currency controls, return to world credit markets, attract foreign investors and set in motion a plan to reduce the fiscal deficit. After that, he hopes to get around to tax reform. In the meantime, there’s the energy sector.

A Plan to End Natural Gas Imports by 2022

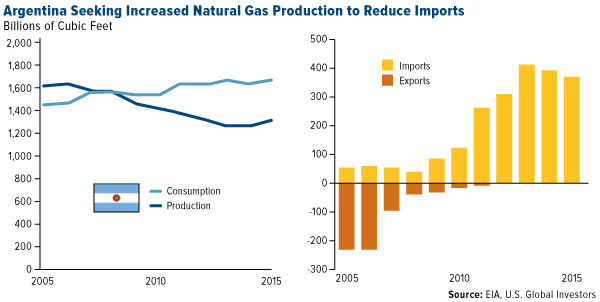

Since 2008, Argentina has been a net importer of hydrocarbons, mainly natural gas, which represents more than half of the country’s energy matrix. Prices are low right now, so the economic impact is not detrimental. Should prices begin to rise substantially, however, it could destroy the economy. As such, my friends and colleagues were invited to help develop the fields and prevent further overreliance on imports. The government, in fact, wants to end them altogether by 2022.

click to enlarge

Production declined mainly because of underinvestment during the two Kirchner administrations. Stringent regulations forced companies to sell product in the domestic market at a discount to international prices. Capital dried up to reinvest in the fields, and the natural decline of well production drove the overall output down. Making matters worse, companies lacked access to capital markets due to the Argentina sovereign debt default in 2001.

As I said, the country is fabulously rich in hydrocarbons such as natural gas and petroleum. It’s estimated to have the world’s third-largest natural gas reserves and, according to the independent research Wilson Center, it “could possibly be the country with the most promising shale prospects outside of the United States.” Its most promising formation is Vaca Muerta (“Dead Cow”), located in the Neuquén basin, which has been compared to Texas’ prolific Eagle Ford play in terms of depth and thickness.

YPF, the government’s oil company, has already done exceptional exploration work, so there are numerous areas ready to be developed. This is the opportunity for us.

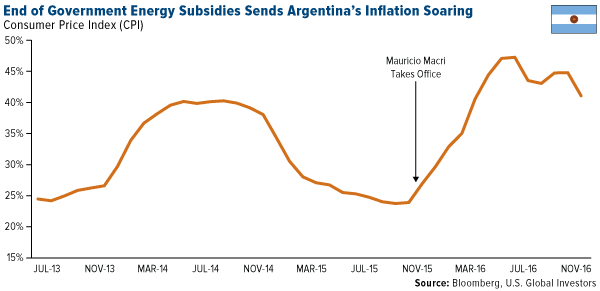

Having seen the projects firsthand and spoken to policymakers, I’m confident Macri can help open up Argentina’s energy sector and streamline production. Upon taking office, one of the president’s first acts was to slash the previous administration’s energy subsidies, which cost the government more than $51 billion over the past 13 years. Electricity bills in Buenos Aires rose a reported 500 percent as a result, but the move allowed the government to save a much-needed $4 billion in 2016 alone.

click to enlarge

Policy Change in the U.S. Has Also Had Amazing Consequences

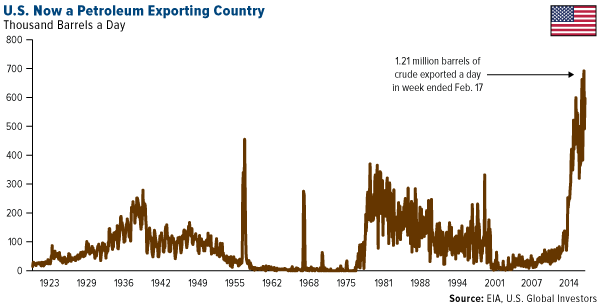

As for the U.S. energy sector, crude exports have never been stronger. After Congress lifted the U.S. oil export ban in December 2015, exporters didn’t hesitate to turn on the spigots. Now, for the second week as of February 17, the U.S. sent more than 1 million barrels of crude onto world markets, filling the gap created by the Organization of Petroleum Exporting Countries (OPEC) in December when it agreed to trim production.

click to enlarge

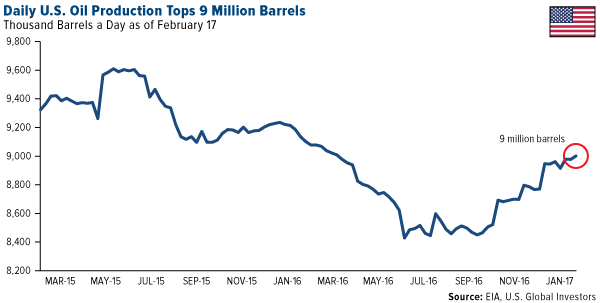

Producers are also ramping up activity. In the week ended February 17, companies pumped more than 9 million barrels a day for the first time since April 2016. The recent weekly record of 9.6 million barrels a day, set in July 2015, could be tested if producers continue their upward trend.

click to enlarge

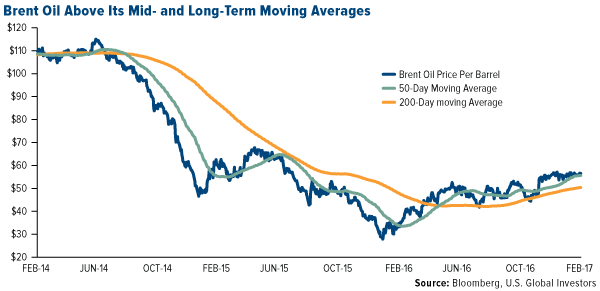

Even with increased output, prices continue to creep up. From its low of just over $30 a barrel last February, Brent crude has climbed 88 percent.

click to enlarge

I’ll have more to add on Argentina next week. In the meantime, happy investing!

The Economy and Bond Market

Strengths

- Existing-home sales jumped to a 10-year high. Sales of existing condos, co-ops, townhomes, and single-family houses increased by 3.3 percent, at a seasonally adjusted annual rate of 5.69 million, the highest since February 2007, according to the National Association of Realtors.

- The 2017 Business Leaders Outlook found that business executives from small and mid-sized firms across the U.S. are more optimistic about the global and national economies and think that the Trump administration will be a positive for the country. JPMorgan surveyed roughly 1,400 executives, and 80 percent said they were optimistic about the national economy. That's up nearly 41 points from the 2016 edition of the survey. About 68 percent said they were encouraged about the outlook for their local economies, an 18-point increase from the year before. Only 3 percent and 5 percent of these executives were pessimistic about the national and local economies respectively, according to JPMorgan.

- European PMIs crushed expectations. Markit's composite purchasing managers' index figure for the eurozone came in at 56.0 in February, well ahead of the 54.3 that economists were anticipating. German manufacturing (57.0) and French services (56.7) were especially impressive.

Weaknesses

- Consumer confidence fell for the first time since Trump's election, according to the University of Michigan's bimonthly survey. The sentiment index in February fell to 96.3 from a January reading of 98.5.

- The preliminary February reading of the Markit U.S. Manufacturing PMI came in at 54.3, below the expected 55.4.

- The December FHFA House Price Index showed growth of 0.4 percent, lower than the expected 0.5 percent.

Opportunities

- Trump's Treasury secretary said tax reform should be passed by August. Steven Mnuchin told CNBC that he expected the overhaul of corporate and personal taxes to be signed into law by the August recess.

- The Dallas Police and Fire Pension is getting behind a Texas lawmaker’s plan to save the retirement system from financial collapse. The fund’s board voted 9-0 on Monday to back a proposal by Dan Flynn, chair of the pensions committee in the state’s House of Representatives, that would raise the retirement age to 58 from 55, eliminate cost-of-living adjustments and lower a multiplier used to determine the size of officers’ and firefighters’ benefit checks, according to a summary on the pension’s website. The plan would also increase Dallas’ annual contribution to 34.5 percent of payroll plus $11 million per year. The city contributed 27 percent in 2015, according to audited financial statements. Employee contributions would climb to 13.5 percent of their pay from 8.5 percent.

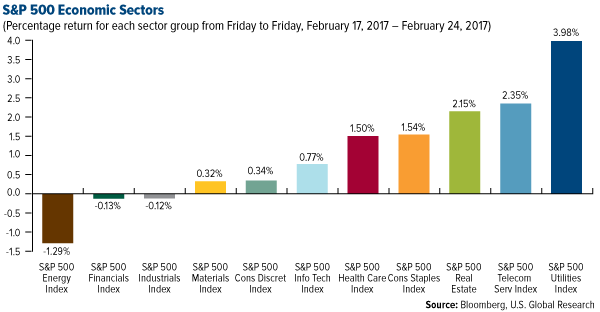

- Oil investors are placing historic bets. Fund managers hold more Brent oil futures and options contracts than at any time on record, equivalent to some 480 million barrels of oil, Reuters reported.

Threats

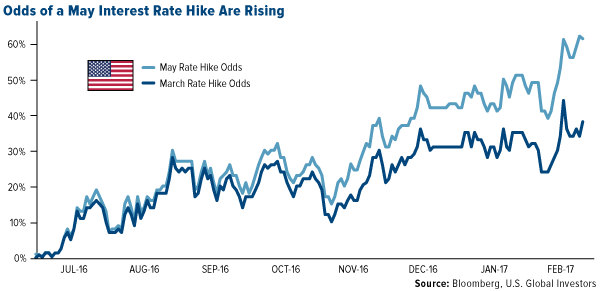

- At least four of Wall Street’s biggest banks are breaking with their bulge-bracket brethren, telling clients that the Federal Reserve will probably raise interest rates before June. BNP Paribas SA, JPMorgan Chase & Co. and Mizuho Securities USA Inc. predict a hike at May’s meeting, even though there’s no press conference scheduled and it comes days before a vote in France’s presidential election that could roil markets. Jefferies Group LLC is alone among Fed primary dealers in calling for an increase next month, while noting that it’s a close call between March and June. As for the rest of the 23 firms, most are set on June, though two points to September, a Bloomberg survey shows. An earlier move than expected could hurt bonds that have not priced the rate hike in.

click to enlarge

- Reports indicate that the Trump administration is pushing back infrastructure investments. Axios reported (citing Republican insiders) that the massive infrastructure plan promised by Trump is likely to not go ahead until 2018.

- Chicago’s school district, the nation’s third largest, is one of the most fiscally disadvantaged in the nation, according to a report from the Education Law Center released yesterday. Illinois has a "highly regressive” school funding system, the report found. School funding in the state is marked by wide funding disparities between low- and high-poverty districts. The city gets 79 percent of its funding from state and local revenues, and has a 1.62 poverty ratio. The rankings are based on a combination of higher-than-average student needs and lower-than-average resources.

Gold Market

This week spot gold closed at $1,257.19, up $22.24 per ounce, or 1.80 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower though by 2.80 percent. Junior-tiered stocks outperformed seniors for the week, as the S&P/TSX Venture Index slipped just 0.91 percent. The U.S. Trade-Weighted Dollar Index finished the week up by just 0.19 percent.

| Date |

Event |

Survey |

Actual |

Prior |

|

Feb-22

|

Eurozone CPI Core YoY

|

0.9%

|

0.9%

|

0.9%

|

|

Feb-23

|

U.S. Initial Jobless Claims

|

240k

|

244k

|

238k

|

|

Feb-24

|

U.S. New Home Sales

|

571k

|

555k

|

535k

|

|

Feb-27

|

Hong Kong Exports YoY

|

8.4%

|

--

|

10.1%

|

|

Feb-27

|

U.S. Durable Goods Orders

|

1.6%

|

--

|

-0.5%

|

|

Feb-28

|

U.S. GDP Annualized QoQ

|

2.1%

|

--

|

1.9%

|

|

Feb-28

|

U.S. Conf. Board Consumer Confidence

|

111.0

|

--

|

111.8

|

|

Feb-28

|

Caixin China PMI Mfg

|

50.8

|

--

|

51.0

|

|

Mar-1

|

Germany CPI YoY

|

2.1%

|

--

|

1.9%

|

|

Mar-1

|

U.S. ISM Manufacturing

|

56.0

|

--

|

56.0

|

|

Mar-2

|

Eurozone CPI Core YoY

|

0.9%

|

--

|

0.9%

|

|

Mar-2

|

U.S. Initial Jobless Claims

|

245k

|

--

|

244k

|

Strengths

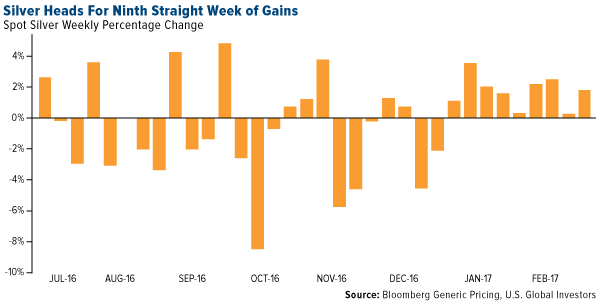

- The best performing precious metal for the week was platinum, with a gain of 2.32 percent and closely followed by silver and then gold. Gold traders and analysts surveyed by Bloomberg continue their bullish stance on the yellow metal for the ninth straight week, as prices climb to November highs. Silver is also on a roll, reports Bloomberg. As you can see in the chart below, silver is up for the ninth straight week, which is the longest run of gains since May 2006. A 9.6 percent decline in supply over a 36-month rate of decline in supply for the metal is the steepest production decline since the World Bureau of Metal Statistics began tracking production in 1995.

click to enlarge

- According to a spokeswoman for the Finance Ministry, Ecuador has repaid a $400 million loan to Goldman Sachs due on February 20 of January 2017, reports Bloomberg. The $400 million loan included interest calculated at a three-month LIBOR rate, plus 4 percent. Thus, there is no threat that the gold collateral for the loan would be monetized.

- Russia increased its gold reserves by 37 metric tons in January, reports Sputnik News, which is equivalent to more than a million troy ounces. Last month’s purchase comes after a pause in December when Russia did not buy any gold.

Weaknesses

- The worst performing precious metal for the week was palladium, down 0.81 percent. Toyota announced mid-week that they have developed a new smaller catalytic converter that uses 20 percent less platinum group metals, but is just as effective as current technology. Toyota plans to introduce the new module into its production lineup later this year.

- Following the Fed’s rate hike outlook earlier this week, the dollar strengthened sending gold to its lowest in nearly a week, reports Bloomberg. Philadelphia Fed President Patrick Harker said that a March rate hike is not off the table. “There seems to be growing consensus among FOMC members that there is an increasing urgency to normalize rates; hence the narrative that every meeting is a ‘live’ meeting,” said Jonathan Chan, an analyst at Phillip Futures in Singapore.

- Primero Mining reported that its December 31 gold reserves fell 24 percent and its silver reserves dropped 20 percent year-over-year, reports Bloomberg. The company says the decrease is primarily attributable to mining depletion and modified modeling parameters.

Opportunities

- Gold continued near a three-month high this week as the dollar weakened, reports Bloomberg. The price movement followed U.S. Treasury Secretary Steven Mnuchin’s remarks that he expects low borrowing costs to persist. In an interview with CNBC, Mnuchin said that issuing ultra-long Treasury bonds is something we “should seriously look at,” with interest rates likely to stay low for a long period.

- After selling all of his gold on November 8 following the election, Stanley Druckenmiller has returned to the yellow metal. While his decision may have been a smart one, Trevor Gerszt writes, it was only smart in the short-term. “Contrary to his prediction, the U.S. Dollar Index began to see significant declines beginning in late December, through January,” Gerszt says. It’s important to remember that gold is not a “get rich quick” investment. Hedge fund manager David Einhorn is also a proponent of gold right now, reports Bloomberg. “Our long-term outlook remains bullish,” for the metal, Einhorn said. “The new Trump administration comes with a high degree of uncertainty, and its policy initiatives appear to be focused on stimulating growth and, with it, inflation.”

- According to the latest fund manager survey by Bank of America Merrill Lynch, gold was viewed as the best hedge against protectionism, reports FTAdviser. In addition, a record amount of fund managers have said gold is undervalued, backing its safe-haven qualities in the event of a rise in anti-trade policies. Similarly, in a recent report from Morgan Stanley, the bank reviews why it is bullish on China, highlighting the Asian nation’s transition from a middle-income nation to a prosperous, high-income nation (sometime between 2024 and 2027). This will likely lead to an increase in gold consumption with more disposable income.

Threats

- Philippines lawmakers will be deliberating on the fate of Environmental Secretary Gina Lopez’s fate as DENR secretary tomorrow. Currently, Lopez’s confirmation is facing opposition because of her decision to cancel 75 agreements for mining projects near watersheds, saying that no new contracts will be issued in sensitive areas. The Philippines president is back and forth on the matter – originally backing Lopez, but more recently deciding to observe due process, and then again using language supportive of her stance.

- The World Bank continues its outlook on gold, writes Kitco News, and it’s not a positive one. John Baffes, the lead author of the bank’s quarterly Commodity Markets Outlook report, reiterated his call that gold could fall 8 percent this year. The forecast, which came out in the bank’s January report, remains grim roughly one month later.

- Although a bright outlook for gold in the first quarter has become as predictable as spring, explains Gadfly, over the past four years the rally has only held throughout the entire year one time, in 2016. Perhaps this means that gold’s strong performance may be nearing its end. Gold prices has always shown a pronounced seasonality, driven largely by the period from early November to mid-February, but of course there was no Trump Whitehouse in the prior four-year study Gadfly examined.

China Region

Strengths

- The Shanghai Composite Index finished the week as the region’s top gainer. The index rose 1.60 percent in the last five trading days and is now only about 1.5 percent off of its 52-week highs.

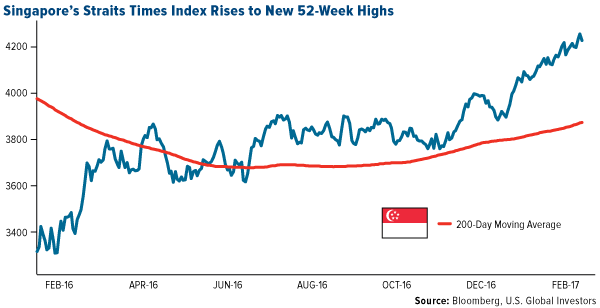

- Singapore’s Straits Times Index soared to new 52-week highs on Friday.

click to enlarge

- Hong Kong’s fourth-quarter GDP print of a 1.2 percent quarter-over-quarter growth rate beat expectations, coming in ahead of an anticipated 0.7.

Weaknesses

- Thailand’s fourth-quarter GDP slowed to 0.4 percent growth, below estimates for growth of 0.7 percent. Thailand’s annual GDP growth for 2016 also missed slightly, coming in at 3.2 percent growth, shy of expectations for 3.3 percent growth, but still up from 2015’s 2.9 percent annual growth.

- Year-over-year export orders in Taiwan came in up 5.2 percent, a little lighter than expectations, for a gain of 7.4 percent and down from January’s 6.3 percent print.

- Singapore’s year-over-year industrial production came in up 2.2 percent, shy of expectations for 9.5 percent and down from last month’s gain of 21.3 percent.

Opportunities

- Bloomberg reports that Malaysian budget airline AirAsia Bhd. is pursuing a dual listing in either Hong Kong or New York.

- Next week investors get PMI data from a number of spots in the region. In addition to official China government Manufacturing and Non-Manufacturing PMI and the Caixin China Manufacturing and Services PMI, investors can look for Nikkei Taiwan PMI, Nikkei Indonesia PMI, Nikkei Singapore PMI, Nikkei Thailand PMI, and Nikkei South Korea PMI.

- Comments from new U.S. Treasury Secretary Steven Mnuchin seem to indicate no urgency to label China a “currency manipulator.”

Threats

- Despite steps to curb property appreciation in Hong Kong, existing home prices in the world’s priciest property market nonetheless climbed to a record ahead of next month’s vote to elect a new chief executive for the city.

- HSBC Holdings Plc (5 HK) dropped this week after missing earnings estimates, blaming the miss in part, according to Bloomberg News, on “slowing growth in its core markets of Hong Kong and the U.K.”

- Particulars for U.S. trade policies with the region remain somewhat unclarified.

Emerging Europe

Strengths

- Romania was the best performing country this week, gaining 2.7 percent. According to Wood & Company research published this week, Romania’s economy will enjoy high GDP growth (+4.5 percent in 2017 and 4 percent in 2018), has low inflation and stocks offer one of the highest dividend yields. Romanian stocks trade at a 30 percent discount to the MSCI Emerging Market Index and 5 percent discount to their five-year average. Finally, Romania’s chances for possible reclassification by the MSCI from frontier to the emerging markets group have increased.

- The Turkish lira was the best performing currency this week, gaining 70 basis points against the dollar. The lira continues its rebound from record low levels supported by the central bank’s unconventional moves.

- The consumer discretionary sector was the best performing sector among eastern European markets this week.

Weaknesses

- Hungary was the worst performing country this week, losing 2.8 percent. The Budapest index was dragged down by a sell-off in OTP Bank and Magyar Telekom. Citi downgraded OTP Bank to a “Sell” rating on margin pressure from the sharp decline in Hungarian interbank rates over the past three quarters. Magyar Telekom was cut to “Neutral” from “Buy” rating at Goldman Sachs on its outperformance and decreased dividend visibility.

- The Romanian leu was the worst performing currency this week, losing 70 basis points against the dollar. The European Union warned that Romania’s deficit may increase to 3.6 percent of GDP this year and 3.9 percent in 2018, after the government cut taxes, increased wages and payments for pensioners.

- The consumer staples sector was the worst performing sector among eastern European markets this week.

Opportunities

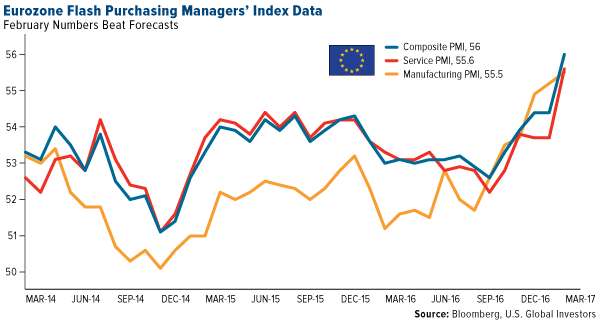

- The Eurozone Composite PMI increased from 54.4 to 56 in February, indicating that the eurozone continues to expand. Both manufacturing PMI, especially in Germany, and service PMI posted strong gains. With domestic demand strengthening and a weaker euro boosting orders from abroad, the eurozone is seeing robust growth.

click to enlarge

- As inflation in Poland accelerated to 1.8 percent after the nation’s longest deflation, reaching the banks central bank’s target range for the first time in four years, policy maker Rafal Sura ruled out any monetary tightening, saying that the recent burst of inflation is temporary and poses no risk of breaching the central bank’s target for the longer term. No rate hikes in the near future should help the economy to grow.

- Russia overtook Saudi Arabia as the world’s largest crude producer in December. Russia pumped 10.49 million barrels a day in December, down 29,000 barrels per day from November, while Saudi Arabia’s output declined to 10.46 million barrels a day from 10.72 million barrels in November. OPEC members decided to restrict supplies by 1.2 million barrels a day for six month starting January1st, and want to achieve full compliance with a deal to trim the output.

Threats

- Eurozone consumer confidence weakened in February for the first time since August. The European Commission on Monday said consumer confidence fell to minus 6.2 percent from minus 4.8 in January, way below economists’ predictions for a drop of 4.9 percent. When consumers become pessimistic about their prospects, they tend to spend less, thereby weakening economic growth.

- Budapest abandoned its efforts to host the 2024 Olympics, after opposition gathered more than 250,000 signatures against the bid citing that the Games are a potential financial disaster. Hungary’s withdrawal is a blow to Victor Orban who supported the idea of his country hosting the Olympics. The next parliamentary elections are scheduled for spring 2018.

- The SPDR S&P Emerging Europe ETF has gained 13.6 percent in the past three months. Political noise in Europe and higher possibility for rate hikes in United States may trigger a correction.

© US Global Investors

www.usfunds.com

© U.S. Global Investors

Read more commentaries by U.S. Global Investors