During the next two decades, an estimated 76 million baby boomers – the bulge of the Western population born between 1946 and 1964 – will begin the process of going from growing and accumulating earnings to retiring and distributing their wealth. This generation, whose leading edge is now 71 years old, is one of the largest ever to go through a modern economy. Last year marked the first year baby boomers began taking required minimum distributions from their retirement accounts. And this is only the first step. Over the next 20 years, this concentration of the population will be scaling back their lifestyles, entering retirement, and drawing on their investment portfolios. This shift will have a significant impact on economic growth.

Baby boomers are the first generation to have control over their own retirement accounts through their IRAs and 401ks. Before them, retirement was covered by a pension plan – or it was just a dream. Not only are the baby boomers a large group spanning most of the first world, but they are also an affluent one. It is estimated that between 70-80% of the wealth in the U.S. is controlled by baby boomers. While their prosperity has accumulated over the past decades, these investors have driven up asset prices to a point where stocks, bonds and real estate assets are simultaneously at or near all-time highs. One of the most basic drivers of investment return is to buy low and sell high. But when prices of assets rise far beyond their reasonable value, the outlook for further returns starts to look bleak. Ironically, while the management of this money is now more vital than ever to the lifestyles of this wealthy generation, expected returns of capital markets are remarkably low. This creates quite a conundrum for investors.

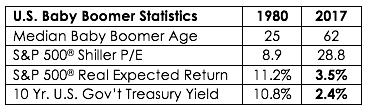

The events leading to our current situation of vast investible wealth and limited reasonable expected return options didn’t happen overnight. It all began back in 1980, when the average boomer was just 25 years old. The global economy was suffering from years of stagflation; inflation and interest rates were high; and asset prices had monotonously drifted lower. The economy had not yet fully embraced globalization and was largely a slow-moving, low-leverage, cash-based system. Interest rates were near historic highs and the U.S. stock market was near valuation lows. Accordingly, the yield for core fixed income assets was approximately 11% a year, and the expected return for the S&P 500® was 11% a year plus inflation. In hindsight, with low asset prices and a weak economy, this was the perfect time to begin a career and a pattern of lifelong investing.

Over the next twenty-seven years, the baby boomers drove and grew economic prosperity and by 2007 had taken it to epic proportions. They contributed to revolutions in technology, medicine, and financial services, just to name a few. Baby boomers also fully embraced the dual income lifestyle. Women didn’t just enter the work force—they built careers and greatly improved household incomes. Furthermore, with a relatively stable and pro-business political environment, global economic collaboration and no major wars, the economy was helped by what is now referred to as the “peace dividend”. Yet the most remarkable pivot was that falling interest rates spurred financial services innovation. This marked the shift from a cash economy to a debt-based economy, and from savings-based to capital markets-based investments. Debt levels and leverage in the economy expanded significantly, and almost everyone became an investor.

The results were inevitable. With a large percentage of the population of working age, growth in the economy was driven by productivity gains and leverage, and the wealth followed. From 1980 to 2007, U.S. Real GDP grew at a rate of 3% a year, and personal debt expanded from 47% of GDP to 95% of GDP. What is significant is that the ensuing accumulation of wealth was not saved in traditional banks or savings instruments, but was poured into capital markets. This created a virtuous, at the time, circle of a leveraged economy leading to rising capital markets asset prices. Astoundingly, the S&P 500® earned 13% a year over this same time period, while Barclays Aggregate Bond Index earned 9% a year. Investors couldn’t lose.

Then came 2008. A near-complete collapse of the entire financial system that drove both borrowing and investing put a full stop on leverage. Something else noteworthy happened, too. Besides the disintegration of the underpinnings of a highly-leveraged debt based economy, 2008 was also when the Boomers began exiting the economy. The leading-aged baby boomers were 62 years old, and likely no longer borrowing and expanding their lifestyles.

Yet the years following 2008 have represented a period of hope, in more ways than one. From 2008 to 2015, U.S. Real GDP grew at just 1% a year. Economic frustration led to eight years of zero percent interest rate policy (ZIRP) and quantitative easing (printing of money). Central banks across the first world have pulled out all the stops to try to orchestrate a return to the baby boomer years of prosperity. While the economy was experiencing the slowest recovery in history, hope had returned to capital markets. With time running out, and with banks and fixed income instruments paying savers little to no interest, investors simply bought riskier and riskier assets in an effort to achieve a reasonable return. During these eight years, money still needed a home, and investors continued to pour money into stocks, bonds and real estate, driving prices back to all-time highs.

Today, we find ourselves in an environment of slow growth, high asset prices, and low capital markets’ expected returns – precisely the opposite of what the baby boomers had experienced during their accumulation phase. From a macro view, the economy and earnings are driven by population growth, leverage, and productivity gains. Population growth presents a significant problem as birth rates across the first world have greatly slowed to below replacement rates; as immigration has become politically unpopular; and as baby boomers are retiring. Leverage is also a detractor, as debt levels are not likely to increase and deleveraging is inevitable and profoundly contractionary. Furthermore, the enticement of low interest rates hurts retirees, as they are no longer borrowing, but rely on higher interest rates for fixed income returns. The only card left is productivity growth; providing more and higher paying jobs to more people. However, productivity cuts both ways. The technology build-out that helped drive growth over the past two decades now enables the economy to operate with less workers. Clearly, this is not quite as strong a tailwind for the economy as we have experienced in the previous decades.

Going forward, the challenge is going to be maintaining and growing retirement accounts in a slow growth, low interest rate, and low capital markets return environment. This is an environment that Frontier Asset Management is uniquely positioned to handle. The hallmarks of Frontier’s investment process are risk management, added value, and consistent returns. During bull markets of rising prices, the benefits of risk management are not obvious. But when investors become retirees and rely more heavily on the outcomes of their portfolios, and when asset prices are high, risk management becomes a priority. If we are in fact in a low return environment, the excess returns that Frontier can achieve from active management decisions will have a greater impact on a client’s overall realized return. Finally, as retirees become more dependent on their portfolio outcomes to support their lifestyles, more consistent return patterns become a point of comfort.

Frontier has managed money through some of the greatest and toughest market environments in recent history. We know that when the economy is performing well and asset prices are rising rapidly, we need to become more alert to alternative outcomes. While the future will be clouded by this inevitable demographic shift, it seems that short-term animal spirits have returned to capital markets. But when short-term risk aversion turns into risk seeking, we at Frontier have learned that it is worth stopping to look around to evaluate the big picture and focus on the long-term.

Past performance is no guarantee of future returns. Nothing presented herein is or is intended to constitute investment advice or recommendations to buy or sell any types of securities and no investment decision should be made based solely on information provided herein. There is a risk of loss from an investment in securities, including the risk of loss of principal. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable or suitable for a particular investor's financial situation or risk tolerance. Diversification does not ensure a profit or protect against a loss. All performance results should be considered in light of the market and economic conditions that prevailed at the time those results were generated.

Exclusive reliance on the above is not advised. This information is not intended as a recommendation to invest in any particular asset class or strategy or as a promise of future performance. Information provided herein reflects Frontier’s views as of the date of this newsletter and can change at any time without notice. Frontier obtained some of the information provided herein from third party sources believed to be reliable but it is not guaranteed and Frontier does not warrant or guarantee the accuracy or completeness of such information. The use of such sources does not constitute an endorsement. Sources include Vanguard, fool.com, multpl.com, data.oecd.org, fred.stlousi.org, tradingeconomics.com, frbsf.org and the US Census Bureau. All calculations by Frontier Asset Management, LLC.

© Frontier Asset Management

© Frontier Asset Management

Read more commentaries by Frontier Asset Management