We have another holiday-shortened week with little fresh data. While there are some Fed speakers on tap, it is not enough to feed the avaricious punditry. There are two competing themes: the spike in inflation and the continuing assessment of Trump Administration policies. Once again, I expect the two to be joined in most commentaries. Pundits will be asking:

Will Trump policies extend the business cycle?

Last Week

Last week the economic news was mostly positive, and stocks responded.

Theme Recap

In my last WTWA I predicted a conjunction of two themes as Fed Chair Yellen testified to Congress and President Trump considered candidates for several Fed vacancies. I was only half right. Yellen got plenty of attention from Congressional questioners and revealed that she plans to finish her term as Chair. She also gave some non-specific agreement with some of Trump’s principles about regulation. GOP questioners wanted to talk about the Fed balance sheet. President Trump did not comment about this. This topic will have continuing interest. Presidents are rarely fans of rising interest rates.

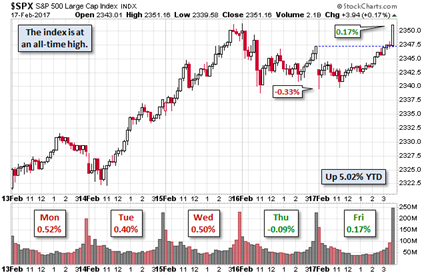

The Story in One Chart

I always start my personal review of the week by looking at this great chart from Doug Short via Jill Mislinski. She notes the record high and the overall gain of 1.51% for the week.

Doug has a special knack for pulling together all the relevant information. His charts save more than a thousand words! Read his entire post for several more charts providing long-term perspective.

The News

Each week I break down events into good and bad. Often there is an “ugly” and on rare occasion something very positive. My working definition of “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

This week’s news was mostly positive.

The Good

-

LA Port traffic surges. Calculated Risk analyzes the factors, concluding that imports and exports both helped, and explaining the dip in 2015.

-

Rail traffic improves, but mostly due to coal and grain Steven Hansen (GEI) reports.

-

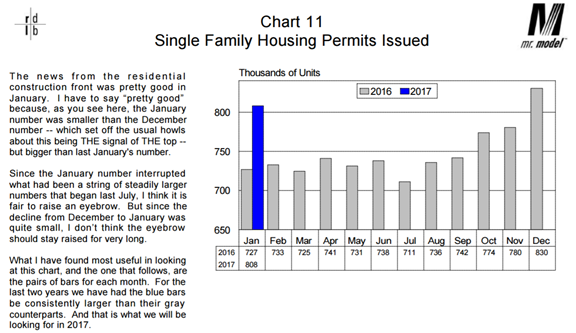

Building permits rose 4.6%. This is one of my favorite leading indicators, since permits cost money and represent a serious commitment. Bob Dieli has a nice chart in his regular data review (subscribers only).

-

Retail sales increased 0.4% beating expectations of a flat report. December’s data was revised to a 1% gain from the prior 0.6%.

-

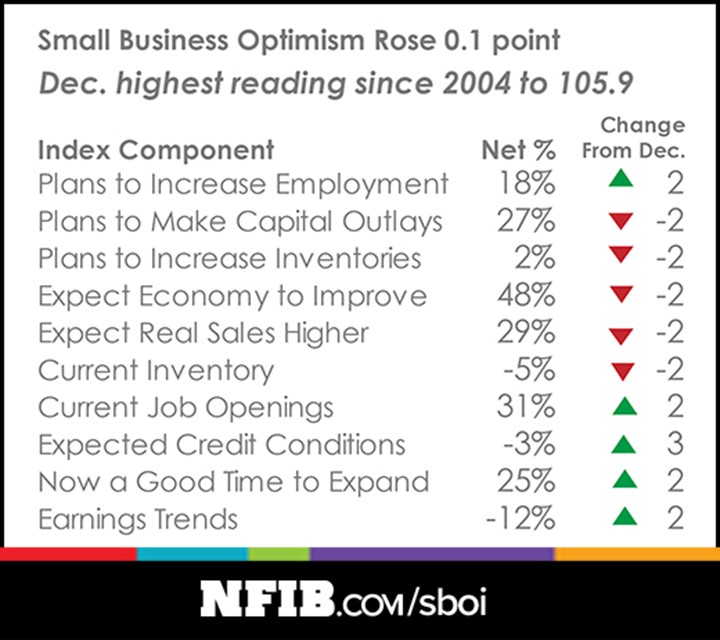

NFIB small business optimism shows that “economic growth is coming.” Dr. Ed opines that this must be a Trump effect.

-

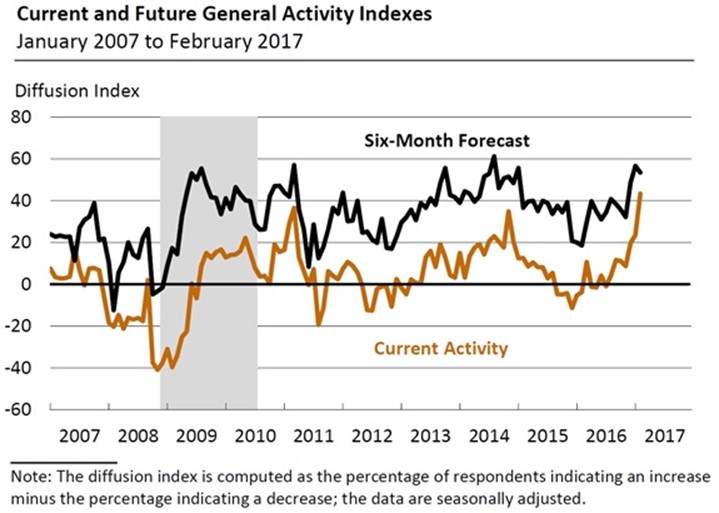

Philly Fed survey rose 43.3, crushing expectations of 17.5 and the prior month’s 23.6. The six-month outlook also remains very strong. From the report:

-

Leading indicators remained strong increasing 0.6% and slightly beating expectations.

The Bad

-

Industrial production dropped 0.3%, missing expectations for a flat report.

-

Fewer developed market stocks are outperforming – 44% versus the 57% average. Eric Bush of GaveKal explains that this has a negative correlation with the overall market.

-

Kim Jong-un took two provocative actions, two days apart. Jonathan D. Pollack at Brookings wrote “…North Korea’s impetuous young leader, yet again reminded the outside world of his determination to defy international norms by all available means”. The ballistic missile test was a flagrant violation of agreements, and the assassination of his half-brother continues a policy of killing potential rivals. So far, the market has taken little notice of such events or other possible challenges to the new president.

-

Inflation data showed price increases greater than expected (Briefing.com consensus in parentheses). PPI was up 0.6% (0.3%). CPI up 0.6% (0.3%). Core CPI up 0.3% (0.2%).

-

Housing starts declined in January, so I am scoring this as a negative. The prior months were revised higher, and the result was a slight beat of expectations.Calculated Risk, one of the top sources on housing matters, ascribes the shifts to the volatile, multi-family sector. Bill expects starts to increase 3% – 7% in 2017. The range may seem wide, but he is careful to explain the expected error around his forecasts, which have been quite good. See the full post for charts splitting out multi- and single-family.

The Ugly

Malware is winning the race against antivirus software. Users are not taking the most important precautions. Hint: Strong passwords and a password manager. (Slate).

The Silver Bullet

I occasionally give the Silver Bullet award to someone who takes up an unpopular or thankless cause, doing the real work to demonstrate the facts. This week’s award goes to Josh Brown for his thoughtful analysis of debt, and what it really means. The arguments about excessive debt, the types of debt, and the threats to the system are easily made. It takes only a chart, and most readers are pre-convinced.

Explaining the data requires a deeper, second-order analysis. In his well-sourced aricle, Josh takes a comprehensive look at employment and lending. You need to read the entire post (twice) but the no-nonsense conclusion captures the key point for investors:

When bankers complain, the rhetoric is almost always a caricature of the reality. Today is no different. There’s probably room to streamline or clean up the crisis era regs, but to make the claim that “the banks can’t lend” flies in the face of the actual facts.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react. That is the purpose of considering possible themes for the week ahead. You can make your own predictions in the comments.

The Calendar

We have a very light week for economic data, with all reports in a three-day period.

The “A” List

- New home sales (F). Gains expected in this important sector.

- Michigan sentiment (F). Important indicator for employment and spending.

- Initial jobless claims (Th). How long can the amazing strength continue?

The “B” List

Fed Presidents will be on the speaking trail. Earnings reports continue. Early actions from the Trump Administration have captured the spotlight and will continue to do so.

Next Week’s Theme

If the market did not have the extreme Trump focus, the question would be whether incipient inflation suggests the need for more aggressive Fed policy and the probably end of the growth portion of the business cycle.

With the daily parsing of tweets, executive orders, and (somewhat conflicting) policy statements, analysts are scrambling to define and re-define the “Trump Effect.”

In a holiday-shortened, light week for data, I expect a combination of these two themes:

Will Trump Policies Extend the Business Cycle?

Discussion of this topic includes both the policies and the business cycle. Most are not rigorous in separating them.

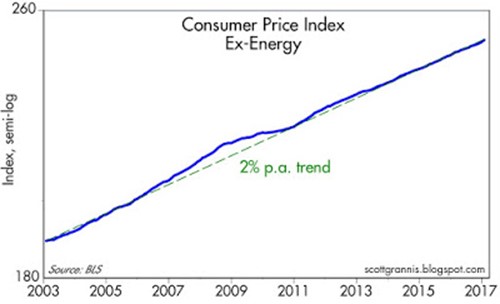

Scott Grannis does a good job by focusing on the inflation effect and the business cycle. He notes that core CPI inflation has been rather stable, and that it is “a stake through the heart of the deflation demon”.

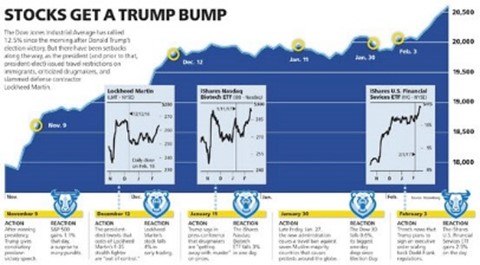

By contrast, Barron’s focuses on the stock and market effects. In their cover story, they review each Administration move:

Will the week ahead provide any more clarity and focus? Maybe not, but investors should look for the following key points:

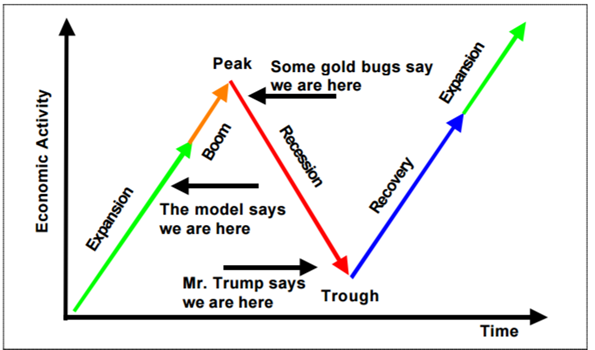

- Is there evidence of a business cycle peak? Here is Bob Dieli’s take, vividly comparing the disparate opinions:

- Will Trump policies extend the cycle? Some are citing confidence from both businesses and consumers as evidence of a return of “animal spirits.” The Trump administration is forecasting much stronger growth than does the CBO. (MarketWatch).

- Many Trump moves are generating opposition, sometimes with the Republican party.

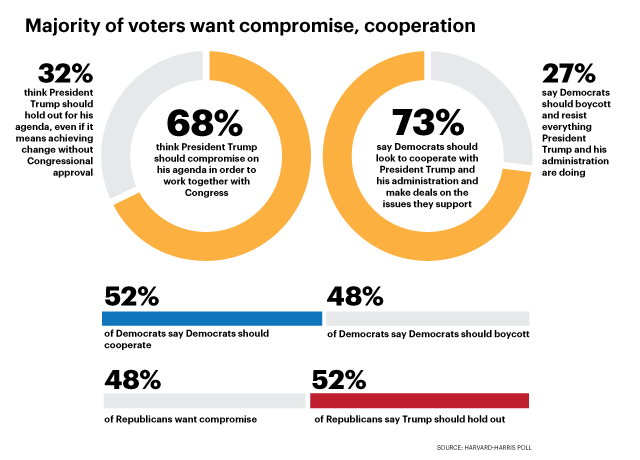

- Most voters are looking for compromises. This is true of both parties. “The Hill.”

What does this mean for investors? As usual, I’ll have a few ideas of my own in today’s “Final Thought”.

Quant Corner

We follow some regular great sources and the best insights from each week.

Risk Analysis

Whether you are a trader or an investor, you need to understand risk. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update.

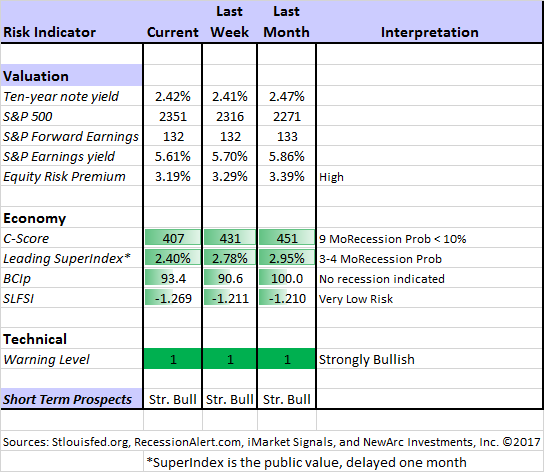

The Indicator Snapshot

The C-Score has again moved lower, reflecting more inflation via gasoline prices. The level is still not worrisome.

The Featured Sources:

Bob Dieli: The “C Score” which is a weekly estimate of his Enhanced Aggregate Spread (the most accurate real-time recession forecasting method over the last few decades). His subscribers get Monthly reports including both an economic overview of the economy and employment. (see below).

Holmes: Our cautious and clever watchdog, who sniffs out opportunity like a great detective, but emphasizes guarding assets.

Brian Gilmartin: Analysis of expected earnings for the overall market as well as coverage of many individual companies.

Doug Short: The World Markets Weekend Update (and much more).

RecessionAlert: Many strong quantitative indicators for both economic and market analysis. While we feature his recession analysis, Dwaine also has several interesting approaches to asset allocation. Try out his new public Twitter Feed.

Georg Vrba: The Business Cycle Indicator and much more.Check out his site for an array of interesting methods. Georg regularly analyzes Bob Dieli’s enhanced aggregate spread, considering when it might first give a recession signal. His interpretation suggests the probability creeping higher, but still after nine months.

The Brooklyn Investor looks at Warren Buffett’s returns, comparing them to other great investors and probability estimates.

Michael Hartnett’s (BofA Merrill Lynch) methods suggest a “melt-up” of 10%. I can’t argue. When CNBC interviewed me about my 2010 call for Dow 20K, I suggested that the next 8-10% would be pretty easy.

How to Use WTWA (especially important for new readers)

In this series, I share my preparation for the coming week. I write each post as if I were speaking directly to one of my clients. Most readers can just “listen in.” If you are unhappy with your current investment approach, we will be happy to talk with you. I start with a specific assessment of your personal situation. There is no rush. Each client is different, so I have eight different programs ranging from very conservative bond ladders to very aggressive trading programs. A key question:

Are you preserving wealth, or like most of us, do you need to create more wealth?

Most of my readers are not clients. While I write as if I were speaking personally to one of them, my objective is to help everyone. I provide several free resources. Just write to info at newarc dot com for our current report package. We never share your email address with others, and send only what you seek. (Like you, we hate spam!)

Best Advice for the Week Ahead

The right move often depends on your time horizon. Are you a trader or an investor?

Insight for Traders

We consider both our models and the top sources we follow.

Felix and Holmes

We continue with a strongly bullish market forecast. All our models are now fully invested. The group meets weekly for a discussion they call the “Stock Exchange.” In each post I include a trading theme, ideas from each of our four technical experts, and some rebuttal from a fundamental analyst (usually me). We try to have fun, but there are always fresh ideas. Last week the focus was when and how to “buy the dips” with a current example from Holmes.

Top Trading Advice

Dr. Brett is back on the job, with several great posts this week. It is difficult to pick a favorite! He has advice on picking the right instruments to trade, identifying real trader education, and why you need to ask the right questions if you are to learn. Do you, for example track prices right after you are stopped out of a trade? There are several other tough, but valuable questions.

Consider attending his trading workshop at the upcoming NY Trading Expo.

Ralph Vince identifies three factors highly correlated with the price of private property. Traders often forget that guessing when to be short is against the odds.

Insight for Investors

Investors have a longer time horizon. The best moves frequently involve taking advantage of trading volatility!

Best of the Week

If I had to pick a single most important source for investors to read this week it would be Chuck Carnevale’s discussion of MLPs. This is a popular investment for those seeking income. Many just look at the yield. Chuck demonstrates the complexity of these partnerships, explaining valuation, tax considerations, and whether you are simply getting your money back. You should not invest in an MLP without reading this first. In addition to his general warning, he provides several ideas worthy of consideration.

Stock Ideas

Airline stocks. Warren Buffett? Really? His famous jocular quote was that a capitalist at Kitty Hawk should have shot Orville Wright to save money for his kids. Philip Van Doorn (MarketWatch) presents the story of this changed attitude. Josh Brown explainswhy Mr. B can be flexible while adhering to long-time principles.

Rural broadband? This could be a big beneficiary from an infrastructure plan (Brookings). Also, see my final investing thoughts below.

Our trading model, Holmes, has joined our other models in a weekly market discussion. Each one has a different “personality” and I get to be the human doing fundamental analysis. This week the dip-buying Holmes sold Nielsen (NLSN) on some strength and add General Electric (GE).

Seeking yield?

Blue Harbinger notes that Verizon’s yield has moved higher despite a reasonable payout ratio. I agree, but I prefer to write calls against stocks like this. If you stick to short-term calls (with the most rapid time decay) you can generate a cash flow of 9 or 10%, including both dividends and premiums from call sales. If the stock is called away, you find a new candidate, since you have gained 4-5% in six weeks. If the stock declines, you sell a new round of calls. If you merely break even, in the long term, on stocks, you are meeting your income objective. I do not typically mention trades before we do them, but we are looking at a buy/write against the April 50 call, which closed at 77 cents bid. You will collect a 58-cent dividend in early April. If the stock does not move, that is over 2 ½ percent in a few weeks. If it is called away, you make about 4.5% and can look for a new trade. This is a great idea for DIY investors who understand options. Naturally, this is an illustration, not a general recommendation. Do not consider it without consulting your financial advisor (yada yada)!

Personal Finance

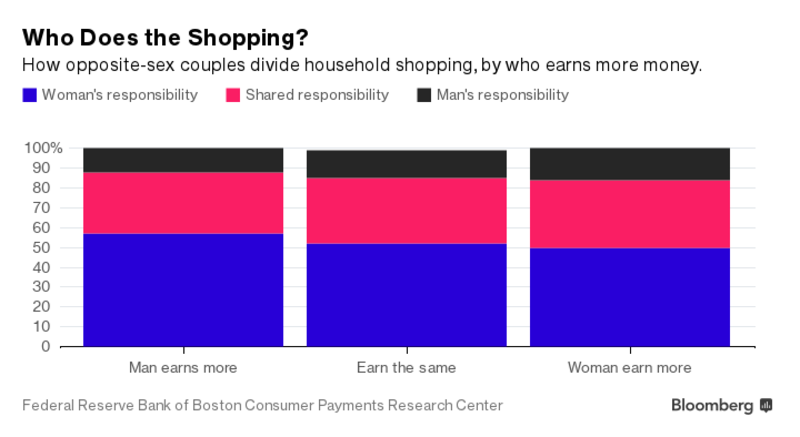

Professional investors and traders have been making Abnormal Returns a daily stop for over ten years. If you are a serious investor managing your own account, this is a must-read. Even the more casual long-term investor should make time for a weekly trip on Wednesday. Tadas always has first-rate links for investors in his weekly special edition. The piece about the importance of a will is great. I liked the one helping you teach kids about money. (I tried to do this with poker chips, and you can guess the ending). My favorite was gender control over family finances. Do you think it matters who is earning more? (Hint: Mrs. OldProf regards it as completely irrelevant).

Seeking Alpha Editor Gil Weinreich’s strong series is ostensibly aimed at financial advisors – a must-read for them. It also attracts many DIY investors. The topics are always interesting, and the discussion is often spirited. Active versus passive investing is naturally a current hot topic.

Ben Carlson explains how to consider housing expenses as part of your overall financial plan.

In case you missed it, you might enjoy my brief, mid-week post on The Fastest Way to Improve Your Investment Results.

Watch out for…

Overpriced dividend stocks. SD Davis explains the need for looking beyond the hoped-for payments.

Yield plays with “dividends” that are merely a return of your own capital.

Emerging market bonds. Lisa Abramowicz at Bloomberg explains the risks, including a decline in foreign currency reserves.

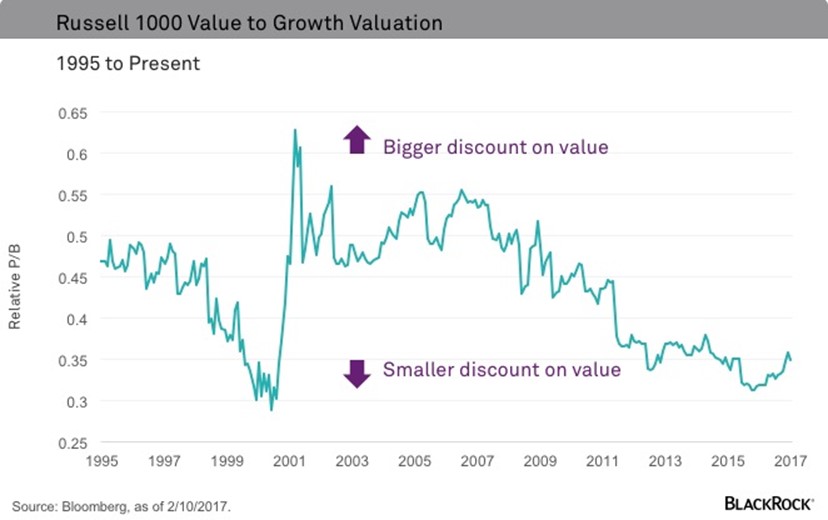

And more on value investing

Black Rock’s Russ Koesterich demonstrates why this style can work in what is perceived as a tough market. Here is his illustrative chart:

Final Thoughts

After years of warnings about deflation and impending recessions, the economy is showing some real signs of strength. For whatever reason, much of the punditry clings to the “end of the up-cycle” thesis, in both the economy and in stocks. Neither economic cycles nor bull markets die of old age.

Inflation concerns are premature. The Fed prefers the core PCE measure, which has less emphasis on housing. It runs “cooler” than the CPI. The Fed has also indicated willingness to exceed the 2% inflation target for some time. They can fight inflation more readily than deflation. I do not expect Trump appointments to reverse this consensus.

Most importantly, the punditry calls it a Trump rally since it occurred at about the same time as the election. There is no analysis of reduced uncertainty or improved fundamentals. The main impact seems to be the promise of reduced regulation.

To summarize, there is a significant improvement in confidence, which is great for the economy and corporate earnings. The reasons for more confidence include many sources.

Investing Conclusion

Finding good ideas from major policy changes is an excellent approach — in theory.

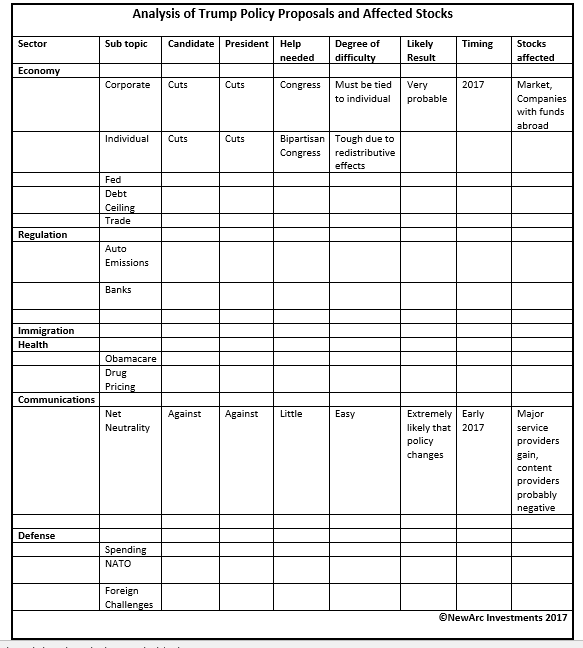

In practice, there are many traps. Too often there are incentives for analysts to be first, rather than to be right. While I have suggested caution on this front several times, it is easier for me. I am not required to fill a TV time slot or write a report for brokerage firm clients. If there is no solid conclusion, I am not forced to act. My approach requires good information, including some which is not yet available. The matrix below is a partial representation of my results. There are more sectors, of course, and I have hundreds of tagged articles in a supporting database. I have preliminary entries for most of the cells. The table below is just an illustration of my approach.

© NewArc Investments, Inc.

Read more commentaries by NewArc Investments, Inc.