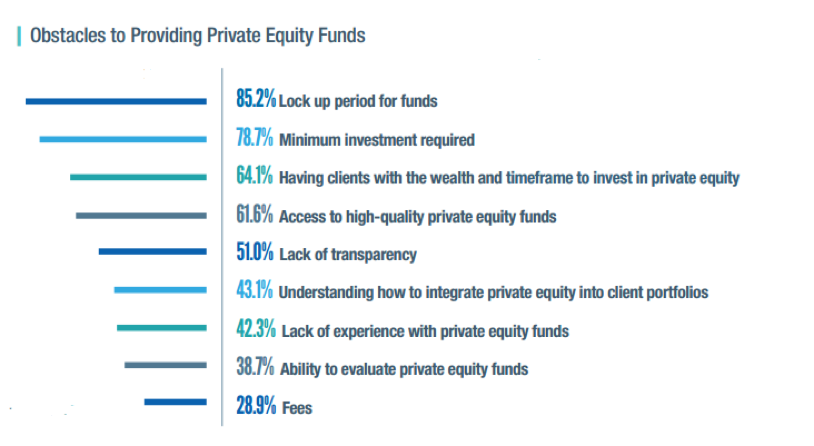

Relatively few investment advisors are making private equity available to their high-net-worth clients, according to new research from iCapital Network. In the same study, advisors cited nine obstacles to offering the asset class that include a range of issues related to the characteristics and mechanics of private equity as well as the advisors’ own proficiency with the investment category (Figure 1).

(Source: iCapital Network)

(Source: iCapital Network)

Practically speaking, the large majority of concerns named by advisors are easily surmounted with new trading platforms and educational tools that are available free-of-charge online.

The single biggest obstacle, as cited by 85% of advisors, is the lock-up period associated with an investment in private equity – something that will not change unless the fundamental nature of private equity changes. Private equity funds put money into private companies and instruments for which there is no public market, meaning that fractional interests cannot easily be priced or traded and are, in effect, illiquid until the entire fund has been monetized. The lock-up of capital during a private equity fund’s investment period is actually one of the ways managers attempt to generate returns, enabling managers to implement longer term value creation strategies that are not possible in a public market context.

First and foremost, the lock-up period means that private equity is not an appropriate investment for everyone. That said, there are a number of other factors that should be considered before eliminating illiquid investments as a potential component of a portfolio.

What should an advisor know about illiquidity?

- Liquidity is an important characteristic of investments and especially important for people who have cash flow needs. But for those who are not cash constrained, an allocation to an illiquid investment may provide certain benefits, such as diversification and enhanced return potential, to a portfolio above and beyond what is typically associated with more readily tradable assets. For most qualified purchasers (typically, individuals with over $5 million in investments), 100% liquidity is not required at all times. For reasons we describe in this article, investors who can “afford” illiquidity should consider investing in it.

- There is a well-documented return premium associated with illiquid investments1 based on historical data, meaning that an allocation to private equity has the potential to boost overall portfolio results. As of March 31, 2016, the Cambridge Associates US Private Equity index outperformed the S&P 500 and the Russell 2000 indices by 300-600 basis points over 10, 15 and 20 year periods.2 When making this comparison, it is also important to note that while investments in private equity funds provide potential for attractive returns, they also present significant risks in addition to illiquidity not typically present in public equity markets, including, but not limited to long term horizons, loss of capital and significant execution and operating risks

- It is a mistake to assume that all private equity investments have the same degree of illiquidity. For instance, private credit and real estate opportunities typically have shorter durations, say 4-5 years, while buyouts and growth equity tend to operate in the 8-10 year timeframe and venture capital and other early stage strategies may require lock-ups as long as 12 or 13 years. Different strategies allow for different liquidity scenarios and different investment goals.

- Behavioral science shows us that even the most sophisticated investors are vulnerable to selling on emotion at the wrong time. Allocating to private equity and illiquid investments generally can help prevent and cushion the impact of panic-driven selling in more liquid portions of a portfolio.

- Private investment strategies have the potential to introduce uncorrelated sources of return to a portfolio. This is critical to hedge the impact of public market movements and avoid having the entire portfolio increase or decrease in value at the same time, a situation that arose for many investors during the global financial crisis that started in 2008. As noted earlier, the capital lock-up associated with private equity is a reason the asset class can function as an uncorrelated return stream within a broader portfolio.

- There is an active secondary market that may allow some limited partnership interests to be sold to other qualified buyers during the investment period, offering a form of liquidity to certain investors that desire it.

As discussed above, advisors’ concerns with illiquidity may be surmountable depending on the specific investor, strategy and scenario in question. Nonetheless, advisors and their clients should thoroughly understand the realities of illiquidity before considering these types of investments.

Hannah Shaw Grove is Chief Marketing Officer of iCapital Network. Caroline Rasmussen is Vice President at iCapital Network.

These materials are for informational purposes only and are not intended as, and may not be relied on in any manner as legal, tax or investment advice, a recommendation, or as an offer to sell, a solicitation of an offer to purchase or a recommendation of any interest in any fund or security described herein. Any such offer or solicitation shall be made only pursuant to a fund’s final confidential offering documents which will contain information about each fund’s investment objectives and terms and conditions of an investment and may also describe certain risks and tax information related to an investment therein. This material does not take into account the particular investment objectives, restrictions, or financial, legal or tax situation of any specific investor. An investment in a private fund is not suitable for all investors.

Past performance is not indicative of future results. An investment in a private equity fund, such as the funds described, entails a high degree of risk and no assurance can be given that any alternative investment fund’s investment objectives will be achieved or that investors will receive a return of their capital. Further, such investments are not subject to the same levels of regulatory scrutiny as publicly listed investments, and as a result, investors may have access to significantly less information than they can access with respect to publicly listed investments. Prospective investors should also note that investments in the products described involve long lock-ups and do not provide investors with liquidity.

The information contained herein is subject to change and is also incomplete. This industry information and its importance is an opinion only and should not be relied upon as the only important information available. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission.

Securities may be offered through iCapital Securities, LLC, a registered broker dealer, member of FINRA and SIPC and subsidiary of Institutional Capital Network, Inc. These registrations and memberships in no way imply that the SEC, FINRA or SIPC have endorsed the entities, products or services discussed herein.

Additional information is available upon request.

1 Private Equity Performance and Liquidity Risk, Franzoni and Nowak (University of Lugano and Swiss Finance Institute) and Phalippou (University of Oxford and SAID Business School), 2011.

2 Cambridge Associates LLC US Private Equity Index and Selected Benchmark Statistics, Q1 2016; US Fund Index Summary: Horizon Pooled Return versus S&P 500 and Russell 2000 indices as of March 31, 2016. https://www.cambridgeassociates.com/our-insights/research/u-s-private-equity-2016-q1/

© iCapital Network

Read more commentaries by iCapital Network

(Source: iCapital Network)

(Source: iCapital Network)