Big Winners in the Neglected Frontier Universe

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsFrontier markets were mixed in 2016, with most of the Middle East and Africa lagging the rest of the universe and a few markets surging ahead 30-40% on the year. We discuss the leading markets individually (below), but we also would like to note the significant structural changes afoot in the MSCI Frontier Markets (FM) index. In 2016, several of the largest markets left in the frontier were flagged for promotion to emerging markets status. These include Pakistan (already emerging markets [EM] in FTSE/Russell and will re-upgrade to EM for MSCI in May 2017), Argentina (watchlisted for EM upgrade by MSCI), and Romania (watchlisted for EM upgrade by FTSE/Russell).

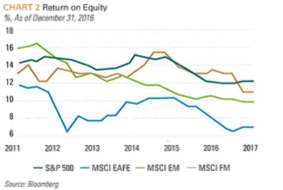

Meanwhile Nigeria may be on its way out of the major indices (watchlisted for expulsion by FTSE/Russell) if it cannot sort out its own exchange rate and convertibility issues soon. Although Vietnam has been busy adding significant breadth and depth to its own market, we still see a dramatic concentration of the opportunity set currently defined as "frontier" on the horizon over the next two years. Overall, the liberalized access to these markets that such upgrades represent is positive for investors, if somewhat dizzying for index watchers. For our investment outlook, we see little directional change from last year's views, and remain bullish on Argentina, Vietnam, frontier Europe, and temporarily Pakistan (new call) and bearish on most of the Middle East and Africa. Overall, frontier markets remain very attractively priced relative to all other major market segments with much lower valuations and ROEs comparable to the S&P 500

(see CHART 1 and CHART 2).

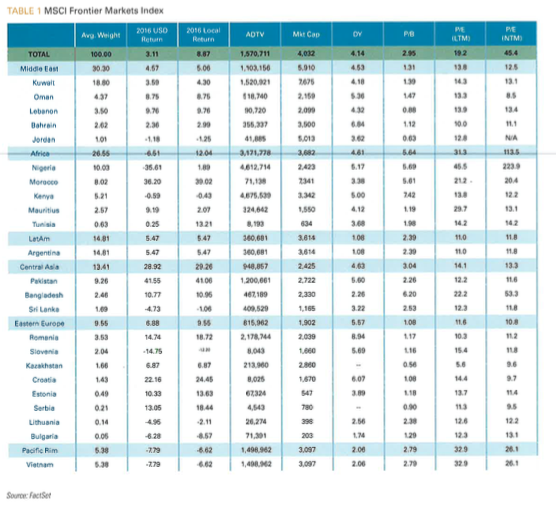

See Table 1

ARGENTINA

2016 portended a year of great change, as reformist President Mauricio Macri began his experiment with market-friendly policies to undo the decade of Peronist populism that left Argentina in stagnation under the previous regime. On the heels of removing export taxes, most capital controls, and allowing the currency to free float at the end of 2015, Macri began 2016 with the priority of reintegrating Argentina into global capital markets. Following a charm offensive in Davos, Macri and his finance team secured a deal with the "holdouts': i.e. the remaining holders of Argentine sovereign debt dating back to their 2001 default. With the majority of the easiest-to-implement aspects of Argentina's market friendly shock therapy in place, Macri then turned to lifting the massive fuel and electricity subsidies and bringing billions back into the economy through a major tax amnesty in an effort to reduce the fiscal deficit (tax revenues were up 34% y/y in 2016).1 In addition to the fiscal benefits, this tax amnesty offers its own unique upside to the market, as it has netted about $10 billion in new private investments from wealthy Argentines that are most likely to be deployed into an array of new real estate and infrastructure funds. The investments themselves will buoy construction and real estate while the fees from the funds will accrue to the banks and asset managers that will administer the funds, which has contributed to our own tactical position in Argentina which we have held since the Spring 2016 in our tactical accounts with EM exposure. For context, the listed segment of Argentina's entire financial sector is a mere $12 billion in market cap.

The Argentine market will get a further boost, with the removal of the final barrier to reopening the local stock market to foreign investment with the capital markets law currently in Congress and whose passage is expected by March.

With access to the global debt pool reopened, Argentina spent much of 2016 splashing into it like a kid on a hot summer day. Reports indicate that about $30 billion in new foreign debt was issued (about $20bn from the federal government and $10bn from the provinces) with expectations for more to come in 2017. Some of those proceeds were used to refinance debt including the buyout of the holdouts from Argentina's last default, but much will go into new spending to cover the fiscal deficit. Looking ahead, and perhaps most importantly, this public debt issuance will also pave the way for the critical relevering of an economy with a mere 18% private debt to GDP, which compares very favorably globally and to its regional peers (See Table 2)

'TPCG Research.

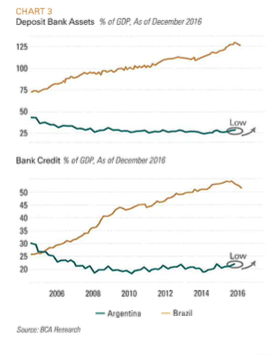

Argentina's banks are especially under leveraged (see CHART 3) and uniquely underexposed to external debt (see CHART 4) offering further runway to reasonable re-gearing and thus economic expansion.

See Table 2 and Chart 3, 4, 5

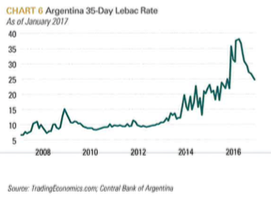

But re leveraging will not occur in the absence of lower interest rates, which in turn necessitates lower inflation, which had been running at over 25-30% under the previous government. The initial results appear very promising on both fronts with the most recent inflation data pointing to a mere 14.4% annualized inflation (see CHART 5) and interest rates coming down concomitantly. But herein lies the biggest risk to Argentina and Macri's agenda is that they fail to contain inflation, undermining confidence in the government and the political consensus necessary to continue the necessary reforms of cutting Argentina's bloated and overpaid public sector and thus the fiscal deficit. And with mid-term legislative elections set for Oct. 29 of this year, the clock is ticking. The key data to watch is INDEC's Consumer Price Index. If monthly inflation stays above 2% for more than 2-3 months in a row, be on guard, and if it crests much higher or persists for more than 6 months in a row, sell. Otherwise, Argentina continues to look like a strategic hold, with forward P/E at a mere 11.8x (for the MSCI Argentina), consensus 2017 GDP growth of 3%, positive macro reform, and last, but certainly not least, a very likely (re)upgrade to MSCI's Emerging Markets index in 2018.2 With so much wind at its back, investors would be wise to pay attention to Argentina for the foreseeable future.

See Chart 5, 6 and Table 3

Investment Recommendation: Overweight and/or long Argentina in FM; add strategically to EM portfolios as well.

VIETNAM

In 2016, Vietnam's market finally delivered on what the economic growth has been portending for over five years with a healthy 17% return. The MSCI Vietnam did not do as well, largely due to its timing in adding the Vietnam Dairy Products Corporation ("Vinamilk") as the largest position in its benchmark in September (now roughly —52% of MSCI Vietnam). Vinamilk, which is generally regarded as the leading blue-chip stock in the market and a darling of foreign investors, was the first test case in the market under Vietnam's more permissive openness to foreign investment and was allowed to scrap its foreign ownership limits in the summer, leading to MSCI's inclusion on September 1. Unfortunately for the index, August was Vinamilk's price apex for the year after a 50% run-up to that point.

Vinamilk's pioneering move was just the tip of the excitement iceberg for Vietnam's historically stolid market in 2016, as a flurry of prominent IPOs hit the market in the final few months of the year with more on deck for 2017.These include, most prominently, two of the top three brewers in the country, which were privatized after years of speculation and expectation (see TABLE 3). Together, these high profile listings have added another $13 billion to Vietnam's market cap, roughly 1.7x the current market cap of the MSCI Vietnam (though only about a 15% increase in Vietnam's overall market cap, given the limited representation of the Vietnamese market in the MSCI index). Given the foreign ownership limits in place for these firms (notably 49% for Sabeco and Habeco), these won't enter the index at par weights to their market cap anytime soon (if at all), but they have certainly expanded the opportunity set of consumer stocks of most interest to foreign investors. This portends a meaningful improvement in market depth, liquidity, and a virtuous cycle to encourage further IPOs and privatizations.

Economically, Vietnam continues to hum nicely. 2016 GDP growth seems likely to come in at 6.2% (just shy of the projected 6.6% we published last year), though Q4 holiday sales were well above trend at 9.4%, so some upside surprise may yet emerge from the final data. Looking ahead, growth next year is projected at another solid 6.4%. As an oil exporter (190,000 barrels/day), Vietnam will also benefit from the recovery in oil prices, which should add another 4-5% to the government budget, independent of organic growth. Some analysts have tried to argue that the election of Trump, and the concomitant death of the Trans-Pacific Partnership trade deal, will slow Vietnam's roll, but the upside to this deal was never really priced into the market. Moreover, the U.S. accounts for only about 20% of Vietnam's total exports, half of which are textiles and shoes, which count more on Vietnam's low wage manufacturing base much more than any special market access. Vietnam's cost basis on products is so low compared to China that whereas manufacturers are revaluating investments in China, no such hesitation exists for Vietnam and foreign direct investment continues apace. Indeed, American frictions with China could, especially if escalated to a trade war, ironically produce a net positive for Vietnam as more manufacturing work flows its way. But if there were a rollback of existing market access for Vietnam in Europe, Japan, or the U.S., this could slow GDP growth by as much as 3% per year over the long-term, which would be a risk to our view.

For now, we see no reason to price any of this policy uncertainty into our market call, and merely see a growing economy, improving market liquidity, expanding market access in stocks that foreigners gravitate towards most, and few estimable macroeconomic risks. Of course, black swan events such as a foolhardy military confrontation with China over the South China Sea could pause this rising tide, but these possibilities appear at least as remote as any other risks across other concomitantly attractive markets. To be sure, really good corporate governance in the market remains rare and the policy apparatus continues as opaque as ever, but As Russia, China India, and other emerging markets have consistently demonstrated, these are not significant barriers to foreign portfolio investments.

Investment Recommendation: Overweight and/or Long Vietnam in FM and possibly even EM portfolios.

PAKISTAN

In 2016, the MSCI Pakistan surged 41.5% in line with the local KSE-100 index on little to no currency appreciation. This was driven almost exclusively by a surge of demand from local investors as foreigners were net sellers during 2016.3 Various reports peg the uptick in demand to a positive review from the IMF, new FDI from China via the China-Pakistan Economic Corridor (CPEC), reversal in sentiment across emerging and frontier markets, and of course the June announcement by MSCI that they will re-upgrade Pakistan to Emerging Market status in May 2017. But a deeper analysis of the market gains over the course of 2016 see a steady increase in demand all year long and reveals a much more organic and sustainable turn in the Pakistani market.

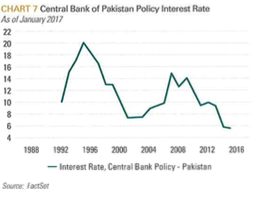

First and foremost, Pakistan's macro-economic stability has brought interest rates down to their lowest level in over 30 years (see CHART 7). This encourages risk assets over fixed income both for direct savers and among discretionary mutual funds and insurance-linked plans. And indeed it is these two sub-markets of local investors that constituted the majority of equity market inflows in 2016 (see CHART 8). In 2015, the government also lowered corporate tax rates from 35% to 30%, which will of course buoy earnings.

Looking ahead, there is ample reason to believe that this is the tip of the iceberg for Pakistan's market. The Securities and Exchange Commission of Pakistan (SECP), under Chairman Muhammad Zafar-ul-Haq Hijazi since December 2014, has undertaken a series of assertive reforms to revitalize Pakistan's capital markets and much of this came in flurry of activity in late 2015 and throughout 2016. This included a new securities law that brought Pakistan much more closely in line with the international standards set forth by the International Organization of Securities Commission (10SCO), as well as further reforms in the areas of corporate restructuring, futures markets regulations, insurance-linked unit trusts, REITs, mutual fund oversight, reporting and disclosure for market participants (including directors, executive officers, and senior shareholders of listed companies), voting rules, dispute settlement, and brokerage licensing, among others. The SECP also unified the country's three exchanges (Karachi, Lahore, and Islamabad) into the single Pakistan Stock Exchange (PSX) and will now pursue a divestment program for the exchange in 2017 to a combination of international investors and a local IPO. The 2016-17 readmission of Pakistan into MSCI's Emerging Markets list is the first big victory in this program, but there is much more room for this trade to run. In 2017, the SECP plans to develop a derivatives market, to establish a central KYC organization to streamline both new account openings and account transfers between investors, and to liberalize new account rules for very small deposit takers in low risk (i.e. money market and fixed income) funds.

All of these reforms are designed to ultimately develop a strong local investor base in Pakistan, which the government now regards as pivotal to their economic development plans. Though growth in the non-banking financial industry (led by mutual funds, see CHART 9), has been strong over the past few years (see CHART 10), Pakistan is starting from a very low base. Pakistan’s mutual fund AUM as a percentage of GDP 2% also compares poorly to other emerging markets such as India and Malaysia, which are around 10% and 57% respectively. Insurance penetration of less than 1% also remains very nascent, though growing fast, and can be compared to a penetration rate of around 4% in India or just over 6% globally.

(See CHART 11)

In our 2016 outlook, though we were aware of Pakistan's macroeconomic improvements and improving market liquidity, we discounted these much too dismissively based on our geopolitical assessments. While Pakistan's political risks remain substantially higher than Argentina, valuations are also on par with Argentina at an undemanding 11.8x forward PIE and a 5.5% dividend yield (5x Argentina's meager 1.1%).4 Some local estimates put valuations at an even more reasonable 9.6x forward P/E,5 which would be a 23% or 29% discount to the MSCI FM Index forward PE of 12.4x or MSCI EM Index forward PE of 13.6x, respectively. The political risks, including an economic dependence on remittances from their large GCC-based population of foreign laborers, which is coming under increasing stress, ongoing insurgencies both domestically and in Afghanistan, and the seemingly endless propensity for political upheaval in Islamabad, of both the democratic and undemocratic varieties, temper what would otherwise be unbridled optimism.

Short-term, going into the market's upgrade in May, we see little downside, as local sentiment should put a floor under anything short of a major economic or political black swan. But if the lessons learned from other upgrade or inclusion situations in the UAE, Qatar, and even individual stocks such as Vinamilk (see above) are any guide, expect a sideways or even falling market for a few months following EM index inclusion as investors pull back from their hot money positions. But Pakistan looks like a strategic buy over the next several years and EM investors would be wise to start the longer than average process of gaining custody and begin studying this market on the rise.

Investment Recommendation: Tactical overweight Pakistan in FM portfolios through May, underweight thereafter before initiating a strategic overweight in EM portfolios after a few months for a market correction.

FRONTIER EUROPE

Briefly, frontier Europe should continue to benefit from an improving macro-economic position of the Eurozone, but even more so by the improved outlook for the Russian market (see FIS Market Outlook). Spillover effects from both neighbors will simultaneously buoy economic fundamentals and market liquidity as both wealth and assets circulate more freely. Already, Romania has single-handedly added meaningful depth to the market by increasing its six-month average daily trading volume from $1.5m at the end of 2015 to about $2.2m at the end of 2016.The hope for the Romanian bourse is to secure an upgrade to Emerging Markets status by MSCI, something the FTSE/Russell providers have already set their sights on. Furthermore, the region remains reasonably priced (10.8x NTM P/E with a 5.5% dividend yield).

Investment Recommendation: Overweight frontier Europe in FM portfolios. Watch Romania for EM upgrade.

GCC (SAUDI ARABIA, KUWAIT, AND OMAN)

Oil prices rebounded strongly in 2016, which gave the GCC markets a reprieve for the year, but these markets still tracked far behind the recovery in oil, as correctly predicted here. What did surprise us is the apparent seriousness of Saudi Arabia's reform efforts under the leadership of deputy crown prince Mohammed bin Salman. His efforts to restructure the economy, shake up the indolent bureaucracy, and reduce subsidies amount to a re-writing of the Saudi social contract. This is a bold agenda in a conservative country that promises to either reshape the landscape of the Middle East, or fail spectacularly such that is stifles reform for a generation. Either way, with a forward PIE of 14.3x (the highest in the region) and a PE/G ratio of 1.4x, we still don't feel that we'd be getting paid for so much uncertainty. Moreover, the market is still only accessible either via derivatives or their nascent qualified foreign investor program, which remains limited to investors with greater than $5 billion AUM, so quick exits in a crisis could be difficult to find. We applaud and encourage bin Salman's efforts, but will stay on the sidelines for now, though with so much positive reform on the agenda, we will be paying close attention from those sidelines.

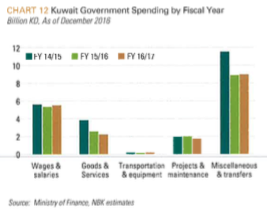

In Kuwait, we see a lot less uncertainty, but equally a lot less upside. The Kuwaiti budget remains in a tight squeeze given the fallout in oil prices (see CHART 12). Moreover the parliamentary elections in November, where opposition candidates won 24 of the 50 seats, promises even more political tensions between the monarchy and the legislature over Kuwait's unsustainable subsidies, which bodes ill for any significant medium-term changes to the status quo. Oil would need to rebound back to $70-$80 a barrel and stay there for a year or so, in order to restart any significant economic growth without further political compromise.

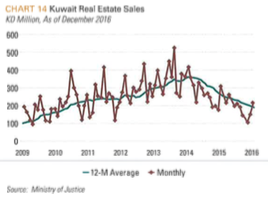

The market, however, is less geared towards the economy than towards credit, which in turn is highly geared towards real estate (see CHART 13). Unfortunately, real estate prices are also in a freefall (see CHART 14 and CHART 15) and show no signs of ebbing anytime soon. Across the Arabian peninsula, Oman is also facing its own fiscal challenges and a potential currency crisis. Surely with all this pessimism and uncertainty, there will be some great opportunities for niche managers to find fallen angels and deep value asset plays at firesale prices across the region, but there is no beta here worth buying anytime soon.

AFRICA (NIGERIA, KENYA, AND MOROCCO)

In 2016, to nobody's surprise (except perhaps Nigerian President Mohammed Buhari) the Nigerian authorities eventually capitulated to the market and devauled the naira by a little over 50%. In this outlook last year we noted that the black market rate was at about 300 naira/USD, and as of this writing the naira has settled in at about 315/USD, proving again the futility of fighting the market. But the transition could have scarcely been handled worst, with months of pointless handwringing and denial culminating in a sudden capitulation the week before the Brexit vote.

Yet even then, the devaluation was incomplete and ultimately resulted in massive selling pressure on the naira and virtual queues at the forex counter as many foreign investors were left without any liquidity in their Nigerian holdings, sometimes for weeks at a time. For their part, FTSE/Russell did not think much of these shenanigans and placed Nigeria on a watchlist for expulsion from the frontier index altogether.

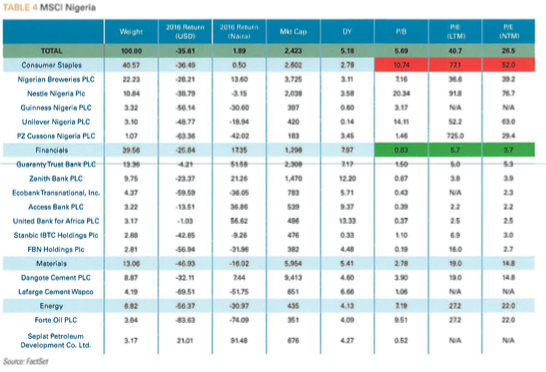

Today, liquidity is restored to the forex market, only for everyone to remember that Nigeria is in a recession, with an estimated -2.4% growth expected from the final 2016 data. Analysts forecast a rebound to 2% growth in 2017, but in an economy with 3% population growth, this is not an optimistic outlook for Nigeria's famed consumer story. Indeed, we believe that consumer stocks in Nigeria continue to look pricey (see Table 4), and like a crowded trade from 2014 that still remains all too crowded.

We are reiterating our (correct) call from last year that these consumer companies remain especially overbought relative to Nigerian banks, which still appear deeply underowned and are even cheaper today than at this time last year (2.5x trailing earnings vs 3.6x last year). And while real growth in Nigeria remains elusive for at least the next year, the rebound in oil prices should alleviate most of the pressure on NPLs at these banks which produced their initial selloff.

Meanwhile an 8% dividend yield pays you to wait for a recovery. But the Naira probably has more room to fail and is already trading at 400-450 in some parallel markets, so this optimism for Nigerian banks is only a call relative to Nigeria. We would expect the blue-chip banks in Nigeria, like Guaranty, to recover to par on any further devaluation as they did in 2016, and with some (any) positive surprises in Nigeria, the banks could be a good absolute call as well.

Investment Recommendation: Underweight GCC in FM portfolios

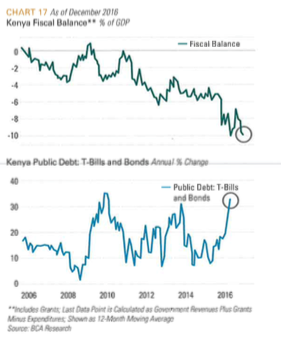

In Kenya, the government surprised markets in August after passing a law that caps interest rates that banks can charge to a mere 4% above government rates (currently at 10.5%), which sent bank shares plummeting to 7-year lows. Though the shares recovered a little from their bottoms, they still finished down 30% on the year. Beyond the banks, the accessible Kenyan market largely consists of Safaricom, which is a great company by all accounts, it's just a question of what is a reasonable price for it and beyond the scope of our macro views. Government debt is rising (see CHART 16 and CHART 17) and a deteriorating fiscal balance will likely lead to some stress on the currency in the near future.

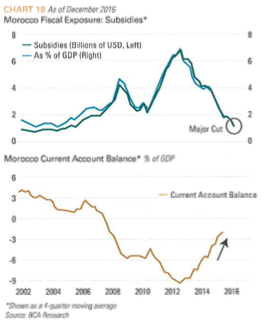

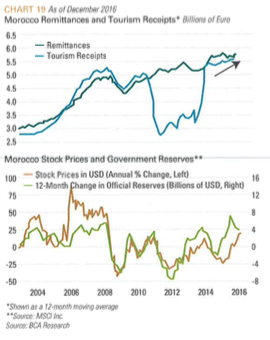

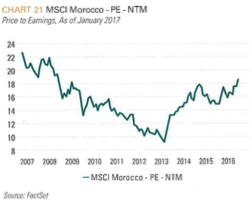

Morocco surged ahead 36% in 2016 as the economy made significant fiscal improvements in cutting the deficit, improving the current account balance and expanding credit (see CHART 18, CHART 19 and CHART 20), but valuations already appear stretched at 20x forward P/E, which is one of the most expensive markets in the frontier (see TABLE 1) and a post GFC high for the market (see CHART 21). Morocco is always a little more expensive than other frontier markets given that its local pension system is essentially a captive market to buy Moroccan assets, but for our part we are happy to let the Moroccans pay for that premium. But the market also has momentum, so we will not be too blinded by valuations and will call for a neutral to slight underweight for now.

1TPCG Research.

2 Already, JP Morgan is set to include Argentine bonds in its flagship GBI-EM Global Diversified index group for emerging currency bonds from February 28.

3 Pakistan Market Outlook 2017: Topine Securities

4 Source: Factset, using the MSCIPakistan.

5 Source:Topline Securities.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All