Post-election excitement is rising, but valuations continue to signal opportunity

Being a deep value investor can be a lonely endeavor. We crunch the numbers to find unloved companies that we believe have bright futures ahead — years ahead, in many cases. But if you wait long enough, market sentiment can shift and your previously unloved holdings may suddenly appear on everyone’s radar screen. That’s exactly what the deep value Invesco Comstock Fund is experiencing right now. But it’s not just two or three names that have recently gained investors’ attention; more than half of the portfolio has been pushed into the spotlight following the election of President Donald Trump.

That’s because more than 50% of the fund is invested in financials and energy, which are dominating the news right now as investors anticipate new policies from the Trump administration that could potentially provide a boost to these sectors. But our positioning isn’t a response to current events — we’ve been invested in energy and financials for years. We built our positions by buying on weakness following the 2008 credit crisis and the 2014 downturn in energy prices. Along the way, we’ve often been a contrarian among contrarians, differing even from other value managers in our peer group.

Given our long-standing view of these sectors, and the current flurry of attention they’re receiving, we’ve been fielding questions from investors who are concerned that they’ve missed the opportunity in financials and energy. As value investors, we always come back to the numbers; this blog will explain why we still have high conviction in these two sectors.

Energy: Spending cuts may shrink supply and boost prices

As of Dec. 31, 2016, Invesco Comstock Fund had a 17% allocation to energy stocks, while our peers in the Lipper Large-Cap Value Funds Category were at 11%.1

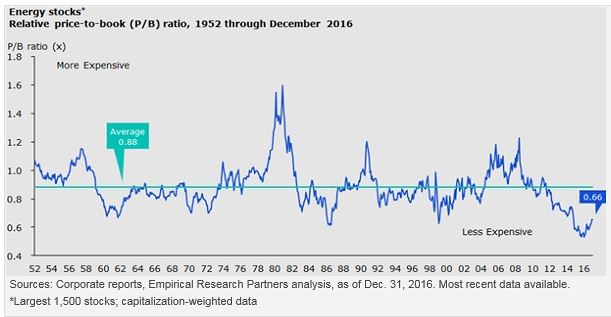

As the chart below shows, despite recent excitement about the sector, energy stock valuations remain very close to historical lows. In fact, energy stocks are even cheaper than they were in the 1980s, which was an extremely difficult time for the industry.

Energy stock valuations are close to historical lows

I would argue that we’re in the early stages of an energy turnaround, with further upside ahead:

- Oil producers have significantly cut back on capital spending (capex) as compared with the peak levels of capex we experienced in 2007. The cuts have been particularly sharp following the collapse of oil prices in 2014. Energy industry consultant Wood Mackenzie Ltd. noted in 2016 that $380 billion of investment in exploration and production projects, representing about 2.9 million barrels a day of production, was being deferred to early next decade.2 It takes time for spending cuts to affect supply and, in turn, prices. I believe the full impact of these cuts lies ahead.

- After years of flooding the market with oil, which drove down crude prices, the Organization of Petroleum Exporting Countries (OPEC) reached an agreement on Nov. 30, 2016, to cut its crude oil output. This was the group’s first production cut in eight years, and it reinforces the fact that Middle Eastern nations need higher oil prices to balance their budgets.

As of Feb. 1, 2016, the futures price for West Texas Intermediate crude oil was about $53 per barrel, according to the US Energy Information Administration. I would not be surprised if we see meaningfully higher prices once the full effects of capex cuts are felt and supply drops.

Financials: Deregulation could help promote growth in banks

As of Dec. 31, 2016, Invesco Comstock Fund had a 36% allocation to the financials sector, while our peers in the Lipper Large-Cap Value Funds Category were around 27%.1

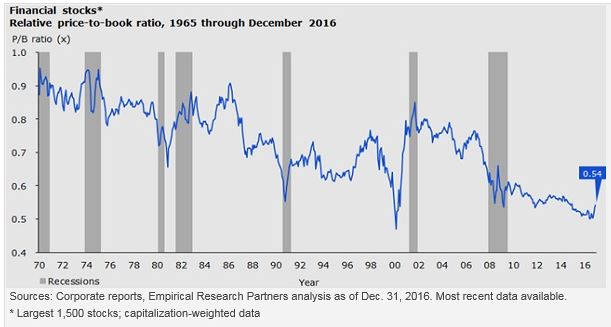

As the chart below shows, financial stock valuations remain very close to historical lows.

Financial stock valuations are close to historical lows

The biggest game-changer we see within financials is the potential for deregulation and pro-growth policies from the Trump administration. This could have a particular impact on big banks and diversified financial companies, which together comprise most of our financials exposure. As we’ve moved further away from the 2008 credit crisis, balance sheets have greatly improved, leverage ratios are significantly lower and many banks are sitting on meaningful excess capital. If the regulatory environment eases, banks should have the flexibility to put that money to work.

Low valuations + favorable policies = potential upside

The trends discussed above have been very long in the making, and their effects won’t be felt overnight. If investors are concerned that the opportunity has passed in these two sectors, simply because they’ve entered the post-election spotlight, I would point to the valuation charts above. In my view, we’re only in the second inning — it’s time to get a hot dog and a Coke, but the game’s not over yet.

Learn more about Invesco Comstock Fund.

1 Source: FactSet Research Systems Inc.

2 Source: Bloomberg News, “Oil Slump Seen Delaying $380 Billion Worth of Developments,” Jan. 13, 2016

Kevin Holt, CFA

CIO, US Value Equities

Senior Portfolio Manager

Kevin Holt is Chief Investment Officer for Invesco US Value Equities and a Senior Portfolio Manager for the large-cap value strategies. He is lead manager for Invesco’s large-cap value products.

Mr. Holt joined Invesco in 2010 when the firm combined with Van Kampen Investments, where Mr. Holt was a portfolio manager for the US value strategy. Before joining Van Kampen in 1999, he served as a senior research analyst at Strong Capital Management and as a portfolio manager/research analyst at Citibank Global Asset Management. He entered the industry in 1989 as a senior financial analyst for Harris Trust and Savings Bank.

Mr. Holt earned a bachelor’s degree from the University of Iowa and an MBA from the University of Chicago Graduate School of Business. He is a CFA charterholder and a member of the Houston Society of Financial Analysts.

Important information

Blog header image: Zocchi Roberto/Shutterstock.com

Price-to-book (P/B) ratio is calculated by dividing the market price of a stock by the book value per share.

A value style of investing is subject to the risk that the valuations never improve or that the returns will trail other styles of investing or the overall stock markets.

Businesses in the energy sector may be adversely affected by foreign, federal or state regulations governing energy production, distribution and sale as well as supply-and-demand for energy resources. Short-term volatility in energy prices may cause share price fluctuations.

The profitability of businesses in the financial services sector depends on the availability and cost of money and may fluctuate significantly in response to changes in government regulation, interest rates and general economic conditions. These businesses often operate with substantial financial leverage.

Derivatives may be more volatile and less liquid than traditional investments and are subject to market, interest rate, credit, leverage, counterparty and management risks. An investment in a derivative could lose more than the cash amount invested.

The risks of investing in securities of foreign issuers, including emerging markets, can include fluctuations in foreign currencies, political and economic instability, and foreign taxation issues.

Stocks of small and mid-sized companies tend to be more vulnerable to adverse developments, may be more volatile, and may be illiquid or restricted as to resale.

The fund is subject to certain other risks. Please see the current prospectus for more information regarding the risks associated with an investment in the fund.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

Before investing, investors should carefully read the prospectus and/or summary prospectus and carefully consider the investment objectives, risks, charges and expenses. For this and more complete information about the fund(s), investors should ask their advisors for a prospectus/summary prospectus or visit invesco.com/FundProspectus.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. Each entity is an indirect, wholly owned subsidiary of Invesco Ltd. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC, investment adviser. Invesco PowerShares Capital Management LLC (PowerShares) and Invesco Distributors, Inc., ETF distributor, are indirect, wholly owned subsidiaries of Invesco Ltd.

©2017 Invesco Ltd. All rights reserved.

Financials and energy: Have value investors missed the boat? by Invesco