“If you want to catch beasts you don't see every day,

You have to go places quite out of the way,

You have to go places no others can get to.

You have to get cold and you have to get wet, too.”

- Dr. Seuss

As we enter 2017 and the beginning of the Trump presidency, the US equity bull market is almost eight years old. In fact, the eight years since the “great recession” has been a bull market not just in domestic equities, but in almost every global financial asset class. This is particularly interesting given how weak actual economic growth has been over the same timeframe.

Writing in July 2016, Kevin Kliesen of the Federal Reserve Bank of St. Louis commented:

“Although the current expansion keeps plugging along, the U.S. economy's pace of growth during the past seven years has been extraordinarily weak. Since the second quarter of 2009 (when the Great Recession officially ended), real growth in gross domestic product (GDP) has averaged 2.1 percent per year. By contrast, growth in the previous three expansions (1982-90, 1991-2001 and 2001-2007) averaged 4.2 percent, 3.6 percent and 2.7 percent, respectively.”1

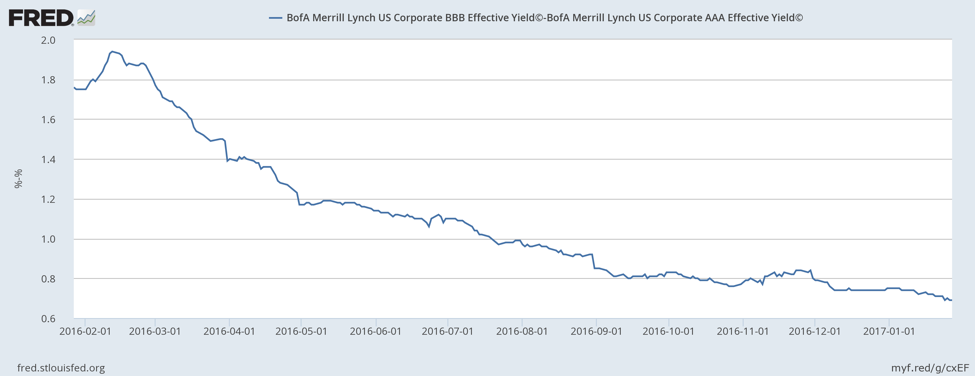

Despite the bull market’s age and weak economic growth, the coordinated central bank interventions in February of 2016 seem to have (once again) successfully quelled any threat of a global recession that appeared possible as commodity prices collapsed and industrial production shrunk for well over a year. Further, as far as markets are concerned, President Trump’s economic proposals are bullish for real growth and risk taking.2 Credit spreads have been narrowing for almost a year now and the trend continues.

Yet whether or not President Trump’s agenda is successful at reinvigorating economic growth, financial assets and domestic equities in particular are priced to provide poor returns going forward. As of January 30, 2017 Research Affiliates projects an average annual real return over the next 10-years of just 0.8% for the S&P 500.3 Even more pessimistic, GMO’s 7-year forecast published on December 31, 2016 estimates a -3.1% annual real return for large capitalization US equities over that period.

No Real Growth? There’s Always Financial Engineering

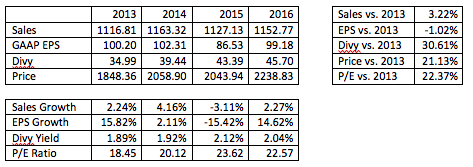

While the economic expansion has been weak, for the largest corporations, the last three years have been even worse. S&P 500 sales are up just 3.2% from 2013 to 2016. Earnings are DOWN 1%. Yet dividend distributions are up 30% and the price to earnings multiple is up 22.4% driving the S&P 500 Index up 21.1%.

S&P 500 Index Statistics4

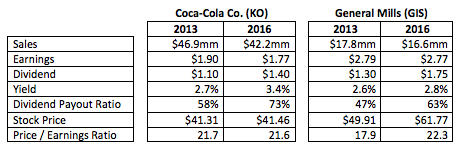

The same phenomenon is visible, in many cases, on the individual company level. This is particularly acute in “consumer staples.” Prior to President Trump’s election and the rally in US-centric and industrial companies, the staples sector was an investor favorite – it offered “stability” and a reasonable yield when compared to sovereign debt. Yet business fundamentals have been deteriorating and most of the growth is via financial engineering – stock buybacks and increasing dividend payouts as a percentage of earnings. Just look at two of the largest and oldest consumer staples: Coca-Cola and General Mills.

According to the most recent Factset Dividend Quarterly (September 22, 2016)5, 42 of the S&P 500 companies paid out MORE in dividends than they earned over the past twelve months. This is the third highest number in the past 10 years. More shockingly, across the entire S&P 500, companies paid out 123% of the past twelve months earnings in both dividends and share buybacks combined. How long can that continue?

Conclusion

While US equities in particular and most global financial assets are expensive (at least according to the historically accurate analytic processes of Research Affiliates, GMO, and the like), there are pockets of opportunity due to idiosyncratic characteristics of individual companies. Hanesbrands and TripAdvisor are the most recent examples we have uncovered.

If valuation does not matter, indices are a viable investment option. On the other hand, if valuation does matter and “you want to catch beasts you don't see every day, you have to go places quite out of the way.”

Broad asset class valuations are certainly at levels that warrant caution. However, credit spreads indicate investors currently have a significant desire for risk taking. For now, it appears the bull market has more room to run.

*****

Sincerely,

Grey Owl Capital Management

Grey Owl Capital Management, LLC

This newsletter contains general information that is not suitable for everyone. The information contained herein should not be construed as personalized investment advice. Past performance is no guarantee of future results. There is no guarantee that the views and opinions expressed in this newsletter will come to pass. Investing in the stock market involves the potential for gains and the risk of losses and may not be suitable for all investors. Information presented herein is subject to change without notice and should not be considered as a solicitation to buy or sell any security. Any information prepared by any unaffiliated third party, whether linked to this newsletter or incorporated herein, is included for informational purposes only, and no representation is made as to the accuracy, timeliness, suitability, completeness, or relevance of that information.

The stocks we elect to highlight each quarter will not always be the highest performing stocks in the portfolio, but rather will have had some reported news or event of significance or are either new purchases or significant holdings (relative to position size) for which we choose to discuss our investment tactics. They do not necessarily represent all of the securities purchased, sold or recommended by the adviser, and the reader should not assume that investments in the securities identified and discussed were or will be profitable. A complete list of recommendations by Grey Owl Capital Management, LLC may be obtained by contacting the adviser at 1-888-473-9695.

Grey Owl Capital Management, LLC (“Grey Owl”) is an SEC registered investment adviser with its principal place of business in the Commonwealth of Virginia. Grey Owl and its representatives are in compliance with the current notice filing requirements imposed upon registered investment advisers by those states in which Grey Owl maintains clients. Grey Owl may only transact business in those states in which it is notice filed, or qualifies for an exemption or exclusion from notice filing requirements. This newsletter is limited to the dissemination of general information pertaining to its investment advisory services. Any subsequent, direct communication by Grey Owl with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status of Grey Owl, please contact Grey Owl or refer to the Investment Adviser Public Disclosure web site (www.adviserinfo.sec.gov).

For additional information about Grey Owl, including fees and services, send for our disclosure statement as set forth on Form ADV using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

1 https://www.stlouisfed.org/publications/regional-economist/july-2016/despite-weakness-economic-expansion-marks-seven-years

2 Deregulation and tax cuts are certainly pro-growth. Infrastructure spending – hard to say. Trade restrictions are anti-growth.

3 https://www.researchaffiliates.com/en_us/asset-allocation.html

4 http://us.spindices.com/indices/equity/sp-500/

Read more commentaries by Grey Owl Capital Management