We have a rather light week for economic data. The biggest reports came last week. Earnings season continues. Everyone is keeping a close eye on President Trump, wondering what might happen next. Meanwhile, stocks are at all-time highs and interest rates have stabilized. This combination creates more questions than answers, which will lead the punditry to wonder:

Is the market optimism justified?

Last Week

Last week the economic news was strong, but (once again) with little reaction from stocks.

Theme Recap

In my last WTWA two weeks ago I predicted a focus on volatility, wondering whether policy uncertainty would have a reaction in stocks. That was a good call, although overshadowed by the policy moves themselves. There were several articles on volatility, mostly noting the lack of reaction in the VIX.

The Story in One Chart

I always start my personal review of the week by looking at this great chart from Doug Short via Jill Mislinski. She notes that the week’s gain was all from early action on Friday. Some attributed this to the employment report, but the timing is more consistent with a reaction to Trump actions on Dodd-Frank.

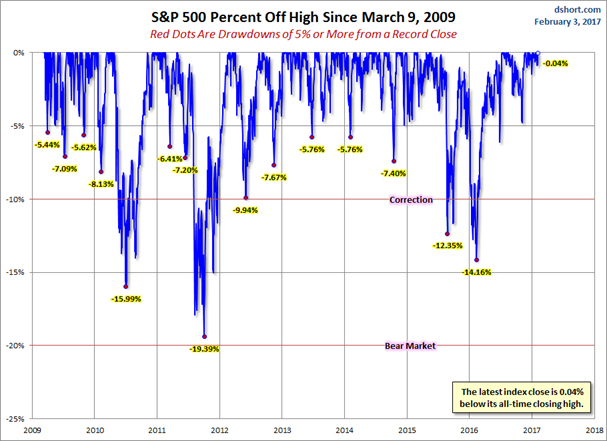

Let us also update another chart from this useful weekly article — a graphic picture of drawdowns. You can readily see both the frequency and magnitude.

Doug has a special knack for pulling together all the relevant information. His charts save more than a thousand words! Read his entire post for several more charts providing long-term perspective.

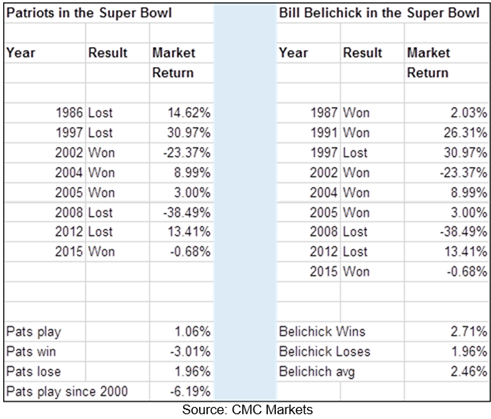

Some Super Bowl Fun with Two Hidden Lessons

Most readers will be watching the Super Bowl today. Did you know how important this is for market performance in 2017? The old AFC/NFC forecast is passé. We now must “dig deeper” into the data. By email I received an analysis that looked at Manning’s, Broncos, and other factors. I’ll focus on this year’s table.

And here is the recommended interpretation:

Looking at the averages, one might think that having New England or Bill Belichick in the big game is no big deal. A look at the year by year results shows that this could be a huge deal since the averages mask big swings in both directions.

For New England, just being in the big game could be a bearish sign as the market has dropped 6% on average in years where the Patriots have played in the Super Bowl since the turn of the century. During the Tom Brady dynasty years, the Patriots have won four of six times so far while the market is tied 3-3. Two of the years the Patriots have made the big game, 2002 and 2008 have coincided with major bear markets, an ominous sign.

Markets have also been volatile in years where Bill Belichick has coached in the big game both with New England and the New York Giants. Following his coaching appearances, the market has finished up 30% once, down 30% once, up 20% once and down 20% once.

Conclusion: What Super Bowl matchups could mean for the market in 2017

Based on the volatile reaction by markets to seeing New England and Bill Belichick in the Super Bowl, combined with the short-term positive, long- term negative reaction to last year’s win by Peyton Manning and the Denver Broncos, it looks like we could be in for a highly volatile for the markets this year. The bull market of recent years could be due for a setback. While signs are mixed over what direction the market may finish the year, there is a strong possibility of a 20% plus move this year.

Jane Wells asked some questions (What milestone did the Dow recently pass? Who is Janet Yellen?) to the high-income Super Bowl Participants. You will enjoy their answers.

Oscar likes the Falcons, but Vince insists that football picks are not part of his programming! Mrs. OldProf likes the Falcons as well, but that is just because they beat her Packers. I’ll stick with the Michigan man.

Use the comments to suggest the “hidden” lessons. WTWA readers should not need me for this oneJ

The News

Each week I break down events into good and bad. Often there is an “ugly” and on rare occasion something very positive. My working definition of “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

This week’s news was again quite good—almost all positive. I make objective calls, which means not stretching to achieve a false balance. If I missed something for the “bad” list, please feel free to suggest it in the comments.

The Good

-

Consumer spending rose 0.5% in December, beating November’s increase of 0.2% and expectations of 0.4%.

-

Pending home sales rose 1.6%, beating expectations for a 0.6% gain.

-

Consumer confidence remained high at 111.8, although slightly slower than the December reading.

-

Initial jobless claims remained low, at 246K. (Calculated Risk).

-

Factory orders increased 1.3% beating expectations and much better than the 2.3% loss from November.

-

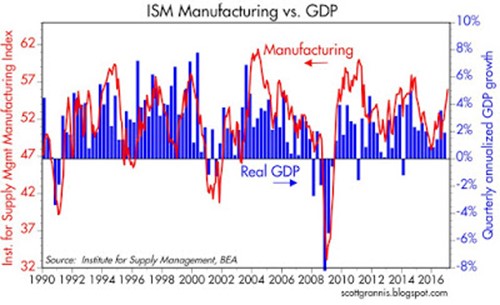

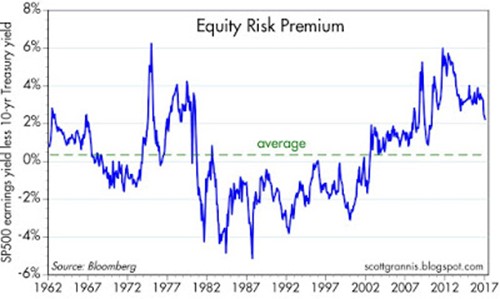

ISM manufacturing registered 56, beating expectations and reaching a level not seen for more than two years. (Scott Grannis). This chart shows why it is important.

-

Auto sales remained at record levels. (Phil LeBeau, CNBC). There is also a shift to the more profitable vehicles.

-

Nonfarm payrolls showed a net gain of 227K. The headline solidly beat expectations, so I am scoring this as “good.” The details were a bit more mixed, with some slight negatives. This is my own summary after reading many sources.

-

Positive

- Headline job gain.

- Increase in labor force participation.

- Benchmark revisions confirming that prior data was something of an under-estimate– also showing healthy growth of jobs from new businesses. (This parallels the Business Dynamics report, which I wrote about here).

-

Negative

- Small negative revisions to prior months.

- No gain in the “household survey” employment.

- Slight uptick in unemployment.

- Sluggish increase (O.1%) in wage gains.

The Bad

-

Personal income increased by 0.3% in December, slightly missing expectations for a gain of 0.4%, but much stronger than the prior month’s 0.1% gain.

-

Construction spending for December declined 0.2%, missing expectations for a slight gain and dramatically lower than the prior month’s 0.9% pop.

-

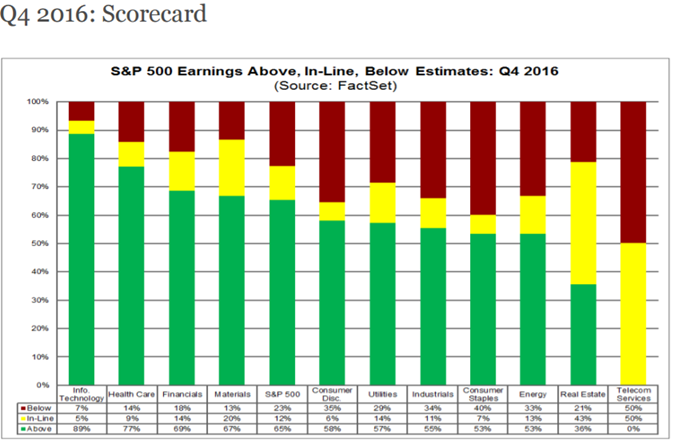

Earnings beats are slightly below recent averages. (Factset).

The Ugly

A possible Chinese stress test for Trump. Jennifer M. Harris, Senior Fellow at the Council on Foreign Relations has an Op-Ed piece, with the full article at CNN. Here is the key quote:

Major geopolitical crises have a way of greeting US presidents soon after taking office. Nazi Germany’s withdrawal from the League of Nations in 1933, the Soviet-led construction of the Berlin Wall in 1961, the Gulf of Tonkin incident in 1964 — all were among the most daunting tests of US foreign policy in the past century, and all came less than a year into the tenures of new US administrations.

This is no accident. Foreign governments often like to test a new White House early on.

Russia, Iran, and North Korea are other obvious candidates.

The Silver Bullet

I occasionally give the Silver Bullet award to someone who takes up an unpopular or thankless cause, doing the real work to demonstrate the facts. Jacob Wolinsky has a terrific review of Harry Dent predictions. Here is one of the most dramatic, from just a year ago.

Time to redraw that one. The power of graphs with red lines and arrows is amazing. Jacob’s article also includes the results of a Google search for Dent’s predictions. You must see it to believe it!

I especially appreciate that Jacob was inspired by his Silver Bullet award in 2013. I only wish that more would join me in highlighting people doing this kind of valuable work.

Meanwhile, Mr. Dent’s business model is working just fine. Check out the speaking fees.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react. That is the purpose of considering possible themes for the week ahead. You can make your own predictions in the comments.

The Calendar

It is back to normal for the volume of economic data, but the most important reports came last week.

The “A” List

- Michigan Sentiment (F). Continued strength anticipated. Special interest in future expectations.

- Trade balance (T). December data with impact on Q4 GDP adjustments. Will be watched more closely as Trump policy is clarified.

- Initial jobless claims (Th). How long can the amazing strength continue?

The “B” List

Fed speakers are back on the trail. Questions will probe the new political environment and hints about future rate hikes.

Earnings reports will remain important. Early actions from the Trump Administration have captured the spotlight and will continue to do so.

Next Week’s Theme

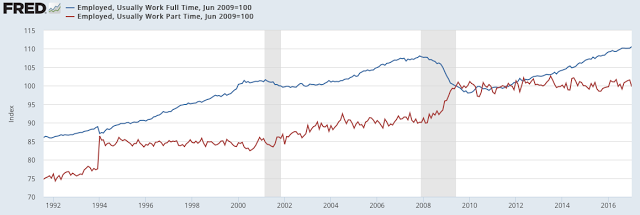

There is plenty of good economic news. A nice chart-packed review from Steven Hansen (GEI). And also from Urban Camel. Here is just one example comparing full-time and part-time jobs. There are plenty of great charts in both posts.

The earnings recession is over and future growth looks good. (Brian Gilmartin).

And yet everyone is nervous. (Great piece from Josh Brown).

While President Trump will continue to grab the spotlight this week, I will continue my focus on the stock market fundamentals. In today’s Final Thought I will offer some suggestions about how to implement this approach. Meanwhile, expect the key question for this week to be:

Is market optimism justified?

The basic positions cover a wide range. Even if one or more of them seem incredible to you, be assured that someone passionately maintains that viewpoint.

- You must be kidding! Market valuations are in nosebleed territory. Investors are like Wile E. Coyote.

- It is only a matter of time before the new Administration does something to spark a crisis.

- Technical indicators have moved to neutral. (Charles Kirk and Guy Ortmann of Scarsdale Equities. Both are excellent, but require a relationship).

- Markets can expect solid earnings growth with upside of 10% or so. (Ed Yardeni, Barron’s).

- Companies are getting more comfortable with Trump and more confident about the future. (Avondale digest of conference calls – a great resource).

- Tax cuts, repatriation of corporate profits, and lower regulations will create an explosion in economic growth.

What does this mean for investors? As usual, I’ll have a few ideas of my own in today’s “Final Thought”.

Quant Corner

We follow some regular great sources and the best insights from each week.

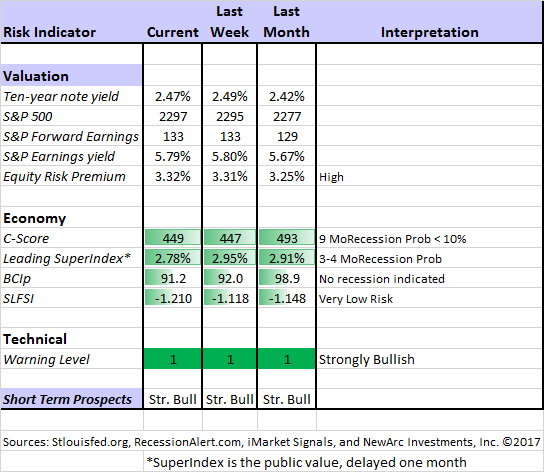

Risk Analysis

Whether you are a trader or an investor, you need to understand risk. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update.

The Indicator Snapshot

Although dropping last week, the yield on the ten-year note has increased significantly since the election. This has lowered the risk premium a bit. I suspect much more to come. By this I mean that the relative attractiveness of stocks and bonds will continue to narrow.

The C-Score has also dropped. The relationship is not linear, and it remains in the “safe” zone.

The Featured Sources:

Bob Dieli: The “C Score” which is a weekly estimate of his Enhanced Aggregate Spread (the most accurate real-time recession forecasting method over the last few decades). His subscribers get Monthly reports including both an economic overview of the economy and employment. (see below).

Holmes: Our cautious and clever watchdog, who sniffs out opportunity like a great detective, but emphasizes guarding assets.

Brian Gilmartin: Analysis of expected earnings for the overall market as well as coverage of many individual companies.

Doug Short: The World Markets Weekend Update (and much more).

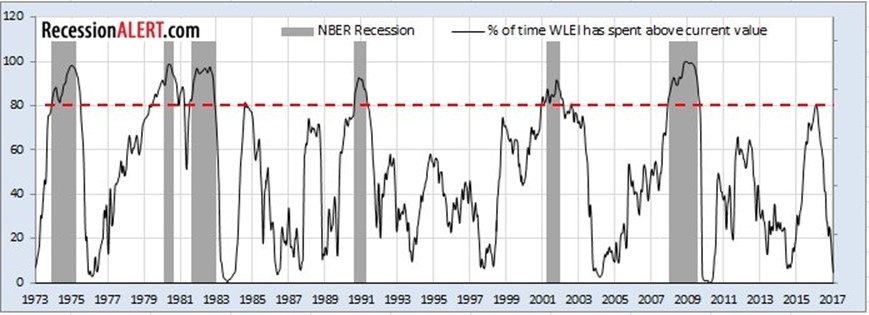

RecessionAlert: Many strong quantitative indicators for both economic and market analysis. While we feature his recession analysis, Dwaine also has several interesting approaches to asset allocation. Try out his new public Twitter Feed, the source of this interesting chart:

This illustrates Dwaine’s take on leading indicators, asking about time above the current value.

Georg Vrba: The Business Cycle Indicator and much more.Check out his site for an array of interesting methods. Georg regularly analyzes Bob Dieli’s enhanced aggregate spread, considering when it might first give a recession signal.

Scott Grannis: The market is not very optimistic. This shows the importance of our weekly coverage of the equity risk premium, showing the relative attractiveness of investors’ two major choices – stocks and bonds.

How to Use WTWA (especially important for new readers)

In this series, I share my preparation for the coming week. I write each post as if I were speaking directly to one of my clients. Most readers can just “listen in.” If you are unhappy with your current investment approach, we will be happy to talk with you. I start with a specific assessment of your personal situation. There is no rush. Each client is different, so I have eight different programs ranging from very conservative bond ladders to very aggressive trading programs. A key question:

Are you preserving wealth, or like most of us, do you need to create more wealth?

Most of my readers are not clients. While I write as if I were speaking personally to one of them, my objective is to help everyone. I provide several free resources. Just write to info at newarc dot com for our current report package. We never share your email address with others, and send only what you seek. (Like you, we hate spam!)

Best Advice for the Week Ahead

The right move often depends on your time horizon. Are you a trader or an investor?

Insight for Traders

We consider both our models and the top sources we follow.

Felix and Holmes

We continue with a strongly bullish market forecast. All our models are now fully invested. The group meets weekly for a discussion they call the “Stock Exchange.” In each post I include a trading theme, ideas from each of our four technical experts, and some rebuttal from a fundamental analyst (usually me). We try to have fun, but there are always fresh ideas. Last week Holmes made a timely call on Macy’s (M). Many of the stocks cited are worth your consideration.

Top Trading Advice

As I suspected a few weeks ago, Dr. Brett Steenbarger is taking a sabbatical to work on his next book. Most traders have probably not matched me in reading all his posts. Many of them have enduring value, so you should take some time to review his archives. My favorite this week helps you to explore you best trading strengths and virtues.

Ralph Vince has a warning about Trump Effects:

While everyone is in a lathered-up blather about executive orders and screeching, we gotta keep our eyes on the ball. I for one can’t get sucked up into political noise when there’s money to be made.

Nearly everyone I speak to is looking for three things:

1. A pullback in equities.

2. Interest rates have bottomed and will now approach more historically normal levels.

3. Volatility is bound to increase in the coming months and perhaps years.

And the degree of which I am hearing this makes me quite certain none of these are in the cards.

A colorful YOLO story – possibly fake – about a trader going “all-in” on poor earnings from Apple (AAPL). His collection of puts and short call spreads would make $5 million if it worked, recovering the $2.5 million inheritance he lost in two years. With the strong report, he was completely blown out, as witnessed on a live stream. There are many lessons here whether it was true or not. Handling wealth. Position size, whatever your confidence. Suspicion about those making dramatic calls to sell their services.

Insight for Investors

Investors have a longer time horizon. The best moves frequently involve taking advantage of trading volatility!

Best of the Week

If I had to pick a single most important source for investors to read this week it would be Davidson (via Todd Sullivan), who pulls together economic data and conclusions in his explanation of why stronger Employment Reports Indicate Higher Equity Markets.He includes several important indicators, emphasizing the need to look at several. This illustrates the right way to do financial research. He writes:

One must continuously test indicators against each other to be intellectually honest.

Stock Ideas

Barron’s likes Chili’s (Brinker International – EAT) but not Chipotle (CMG).

Our trading model, Holmes, has joined our other models in a weekly market discussion. Each one has a different “personality” and I get to be the human doing fundamental analysis. We have an enjoyable discussion every week, including four or five specific ideas that we are buying. This week the dip-buying Holmes (who has been very hot) liked Macy’s (M). That worked well for those who did their own research and agreed.

Seeking yield?

How about health care REITs? Blue Harbinger analyzes twenty candidates, two of which we own.

Personal Finance

Professional investors and traders have been making Abnormal Returns a daily stop for over ten years. If you are a serious investor managing your own account, this is a must-read. Even the more casual long-term investor should make time for a weekly trip on Wednesday. Tadas always has first-rate links for investors in his weekly special edition. My personal favorites this week are two entries I see as related. Josh Brown points out the opportunity for young people to start saving and investing, enjoying compound interest. Tony Isola shows the flip side – the cost of an impulsive purchase paid off on a credit card. This is a great lesson!

Seeking Alpha Editor Gil Weinreich’s Financial Advisors’ Daily Digest has quickly become a must-read for financial professionals. Somewhat to my surprise, the topics are also especially relevant for active individual investors. They frequently join in the comments, adding to the value of the posts for both groups. Gil has several good topics, but I especially liked this discussion of the fiduciary rule. Most people do not understand what this means, and what is at stake. I strongly support Gil’s argument.

Watch out for…

Binary options. Another product that seems simple but few understand or trade successfully. (FT).

BDC’s. BDC Buzz has the story.

VIX trading. Bill Luby provides data on the poor results of VIX ETPs. Many are tempted to buy the VIX as a hedge without even knowing how it is calculated or whether it is a leading indicator.

Final Thoughts

Like Josh Brown, I am hearing a lot of worry about what might happen in the Trump Administration. Over the last several months I have highlighted all of the following:

- An expectation that the Market would rally no matter who won the election – just removing one element of uncertainty.

- The earnings recession ended in Q316.

- Forward earnings are the most effective way to forecast the market, and 8-10% higher is quite plausible.

- P/E multiples are strong when people have confidence in earnings.

- This could be conservative if repatriation, better growth, or reduced regulation come to pass.

- The best sectors are financials, tech, home builders, and some biotech.

- The biggest market worry is a battle over trade, especially with China.

To my surprise I opened Barron’s and found Dr. Ed Yardeni making exactly the same points. Anyone reading WTWA for the last few months could have done the interview. I generate my own ideas and reach my own conclusions, but I always like it when astute analysts look at the same evidence and agree.

In a similar vein, my Seeking Alpha colleague Bill Kort has a great analysis of the danger of mixing your opinions about news with your investments. I am delighted that some of my work and my highlighting of Morgan Housel encouraged him to pursue this valuable topic.

Policy uncertainty remains the most important investor worry. We can mitigate this in two ways:

-

De-emphasize the social issues. Yes, they are important. Feel them passionately if you wish. As an investor, you must ask whether they affect your portfolio.

- Consider timing. We cannot know about and react to a military attack. We can monitor the progress of trade negotiations. The most important investor threats still leave us time to react. I am watching closely, and so should you.

© NewArc Investments, Inc.

Read more commentaries by NewArc Investments, Inc.