Happiness is wanting what you have

And not wanting what you don't have.

— Shakyamuni Buddha, 500 B.C.

The three grand essentials of happiness are: something

To do, someone to love, and something to hope for.

— Alexander Chalmers

Happiness runs in a circular motion...

Happiness runs, happiness runs.

— Donovan, 1968

I think a lot about happiness - what makes a person happy, whether or not happiness should even be a life's priority - things like that. A good high school friend stunned me at the early age of 17 by suggesting we should not necessarily try to be happy. Sacrifice, service, devotion to a cause were higher orders, he felt, although presumably, since those were choices, their pursuit could secondarily lead to happiness.

Through the years I've accumulated a short list of quotes that express a personal view of what makes people happy. You, I'm sure, have your own candidates, but most of them probably resemble some of the ones listed above: Stay busy doing something you enjoy; be mindful of other people and the world in, around, and above you; don't let your reach exceed your grasp; find someone to share your happiness with. My favorite of all of these is the one above by Donovan - that somewhat kooky "love generation" folk singer of the late 1960s. "Happiness runs in a circular motion...happiness runs, happiness runs." There may be more to this refrain, however, than appears at first glance, the entirety of which I've tried to encapsulate artistically in my open-ended smiley face that wasn't ever-popular when Donovan crooned the tune. For years I thought that the gist of Donovan's phrase was the obvious - the "pay it forward" allusion that suggests what goes around, comes around - and it undoubtedly is. But there are hidden nuances, at least to me. The "running in a circular motion" also connotes a self-contained, inward-looking, self-satisfaction that equates happiness to being content with yourself as a person. And the last phrase - "happiness runs, happiness runs" may speak to the Buddhist philosophy of impermanence and the priority of the moment. Donovan might not rank up there with Kant and Spinoza, but his little song packs a powerful message. Rock on, flower child, wherever you are.

For years I thought that the gist of Donovan's phrase was the obvious - the "pay it forward" allusion that suggests what goes around, comes around - and it undoubtedly is. But there are hidden nuances, at least to me.

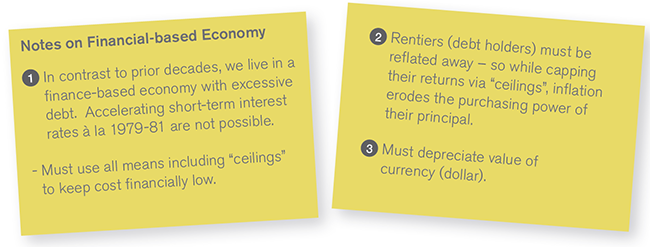

And while happiness may run in a circular motion, it seems history may too - or at least it may rhyme, as Mark Twain once said. Pictured below are two of my notes written not recently, but in 2003. They are as relevant today as they were then. "Financial repression" runs...in a circular motion, it seems. In 2003, though, central bankers had rarely contemplated the monetary policy instruments that could lower and then artificially cap interest rates. Although my notes correctly allude to "all means including 'ceilings' " to keep the cost of financing low, the expansion of central bank balance sheets from perhaps $2 trillion in 2003 to a now gargantuan $12 trillion at the end of 2016 is remarkable. Not only did central banks buy $10trillion of bonds, but they lowered policy rates to near 0% and in some cases, negative yields. All of this took place to save our "finance-based economy" and to raise asset prices upon which that model depends. As any investor would admit, these now ongoing policy panaceas have done just that - promoted higher asset prices and engendered a modicum of real growth. In the process however, as I have frequently written, capitalism has been distorted: savings/investment has been discouraged by yields/returns too low to replicate historic productivity gains; zombie corporations have been kept alive in contrast to Schumpeter's "creative destruction"; debt has continued to rise relative to GDP; the financial system has not been cleansed and restored to a balance where risk and reward are on a level plane; disequilibrium has replaced equilibrium, although it is difficult to recognize this economic phantom as long as volatility is contained.

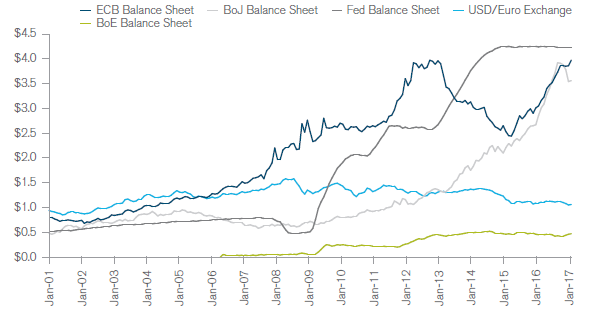

But in order to control volatility, and keep a floor under asset prices, central bankers may be trapped in a QE-forever cycle, (in order to keep the global system functioning). Withdrawal of stimulus, as has happened with the Fed in the past few years, seemingly must be replaced by an increased flow of asset purchases (bonds and stocks) from other central banks, as shown in Chart I. A client asked me recently when the Fed or other central banks would ever be able to sell their assets back into the market. My answer was "NEVER". A $12 trillion global central bank balance sheet is PERMANENT - and growing at over $1 trillion a year, thanks to the ECB and the BOJ.

Central Bank Balance Sheet (US$)

Source: Bank of England website "Following Bank of England money market reform on 18 May 2006 theBank of England 'Bank Return' was changed. This series forms part of the new Bank Return, with datastarting on 24 May 2006."

An investor must know that it is this money that now keeps the system functioning. Without it, even 0% policy rates are like methadone - cancelling the craving but not overcoming the addiction. The relevant point of all this for today's financial markets? A 2.45%, 10-year U.S.Treasury rests at 2.45% because the ECB and BOJ are buying $150 billion a month of their own bonds and much of that money then flows from 10 basis points JGB's and 45 basis point Bunds into 2.45% U.S. Treasuries. Without that financial methadone, both bond and stock markets worldwide would sink and produce a tantrum of significant proportions. I would venture a guess that without QE from the ECB and BOJ that 10-year U.S. Treasuries would rather quickly rise to 3.5% and the U.S. economy would sink into recession.

An investor must know that it is this money that now keeps the system functioning. Without it, even 0% policy rates are like methadone - cancelling the craving but not overcoming the addiction.

So what's wrong with financial methadone? What's wrong with a continuing program of QE's or even a rejuvenated U.S. QE if needed? Well conceptually at first blush, not much. The interest earned on the $12 trillion is already being flushed from central banks back to government fiscal authorities. One hand is paying the other. But the transfer in essence means that monetary and fiscal policies have joined hands and that the government, not the private sector, is financing its own spending. At an expanding margin, this allows the private sector to finance its own spending and fails to discriminate between risk and reward. $600 billion in the U.S. for instance goes into the repurchase of company stock, whereas before, investment in the real economy might have been a more lucrative choice. In addition, individual savers, pension funds, and insurance companies are now robbed of the ability to earn rates of return necessary to maintain long-term solvency. Financial Armageddon is postponed as consumption is brought forward and savings suppressed and deferred.

For now, investors must go with, indeed embrace this financial methadone QE fix. Quantitative easing will continue even though the dose may be reduced in future years. But while a methadone habit is far better than a heroin fix, it has created and will continue to create an unhealthy capitalistic equilibrium that one day must be reckoned with. Yields will likely gradually rise (watch 2.60% on the 10-year Treasury), yet they will stay artificially low due to the kindness of foreign central bank quantitative easing policies. But that is not a good thing. Happiness runs...Happiness runs, and so one day, will asset markets, artificially supported by quantitative easing.

Investing involves risk, including the possible loss of principal and fluctuation of value.

Returns quoted are past performance and do not guarantee future results; current performance may be lower or higher.

The views expressed are those of the author, Bill Gross, and do not necessarily reflect the views of Janus. They are subject to change, and no forecasts can be guaranteed. The comments may not be relied upon as recommendations, investment advice or an indication of trading intent.

There is no assurance that the investment process will consistently lead to successful investing.

In preparing this document, Janus has relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources.

Fixed income securities are subject to interest rate, inflation, credit and default risk. The bond market is volatile. As interest rates rise, bond prices usually fall, and vice versa. The return of principal is not guaranteed, and prices may decline if an issuer fails to make timely payments or its credit strength weakens.

Investing in derivatives entails specific risks relating to liquidity, leverage and credit and may reduce returns and/or increase volatility.

Statements in this piece that reflect projections or expectations of future financial or economic performance of the markets in general are forward-looking statements. Actual results or events may differ materially from those projected, estimated, assumed or anticipated in any such forward-looking statements. Important factors that could result in such differences, in addition to the other factors noted with such forward-looking statements, include general economic conditions such as inflation, recession and interest rates.

Janus makes no representation as to whether any illustration/example mentioned in this document is now or was ever held in any Janus portfolio. Illustrations are only for the limited purpose of analyzing general market or economic conditions and demonstrating the Janus research process. References to specific securities should not be construed as recommendations to buy or sell a security, or as an indication of holdings.

This material may not be reproduced in whole or in part in any form, or referred to in any other publication, without express written permission. Send email requests to [email protected]. Janus is a registered trademark of Janus International Holding LLC. © Janus International Holding LLC.

Investment products offered are: NOT FDIC-INSURED | MAY LOSE VALUE | NO BANK GUARANTEE

© Janus Henderson Investors

Read more commentaries by Janus Henderson Investors