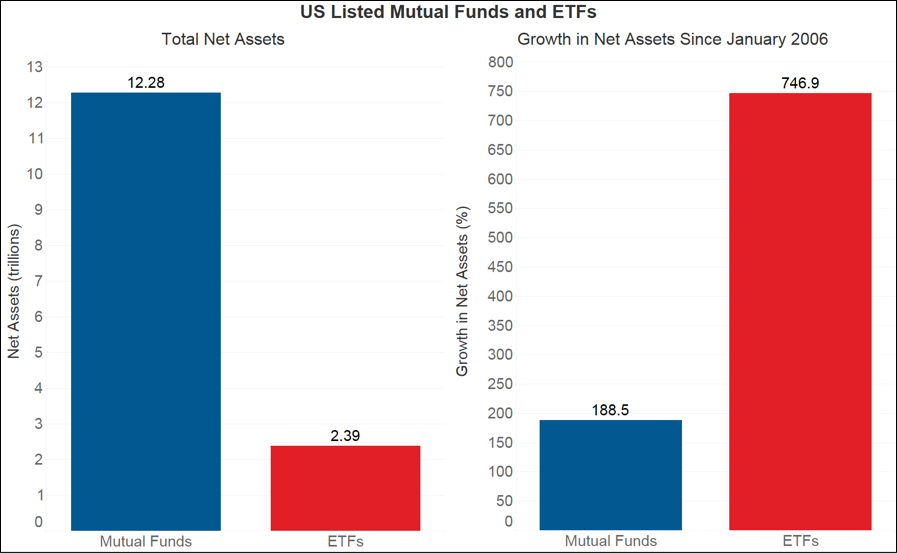

At long last the fund rating company, Morningstar, has decided to put mutual funds and exchange traded funds (ETFs) on a level playing field when it comes to fund ratings and comparisons1. Beginning on November 30, 2016, Morningstar did away with segregated categories for mutual funds and ETFs and merged both types of open-ended investment vehicles into all-encompassing categories. This change is rooted in migrating investor preferences as assets flow into ETFs at the expense of often-times poorer performing, higher cost, and tax-inefficient actively managed mutual funds. Indeed, according to the Investment Company Institute, ETF assets have grown more than seven-fold since 2006 while mutual fund assets have grown less than two-fold over the same period.

Source: FactSet. As of 9/30/2016.

So, what does all this mean for financial advisors and why is it important?

As fiduciaries, financial advisors have the burden and responsibility to allocate client funds in a way that suits clients’ best interests. Morningstar’s tearing down of the wall that once divided mutual funds and ETFs means that no longer can the legal structure of an investment product be reason enough to segregate analysis of the two vehicles. Instead, the benefits and features of the investment – the historical performance, fees, transparency, tax consequences, capacity constraints, etc. – must now be considered for all open-ended vehicles equally, regardless of the legal wrapper under which the product operates. Once the differences between mutual funds and ETFs are brought into the spotlight, suitability analysis may squarely favor ETFs over mutual funds in many cases.

1Morningstar announced in a letter to clients effective November 30, 2016 it will combine ETFs and open- end mutual funds into a single peer group. Read Morningstar’s FAQ.

How ETFs and Mutual Funds Contribute to Performance Outcomes

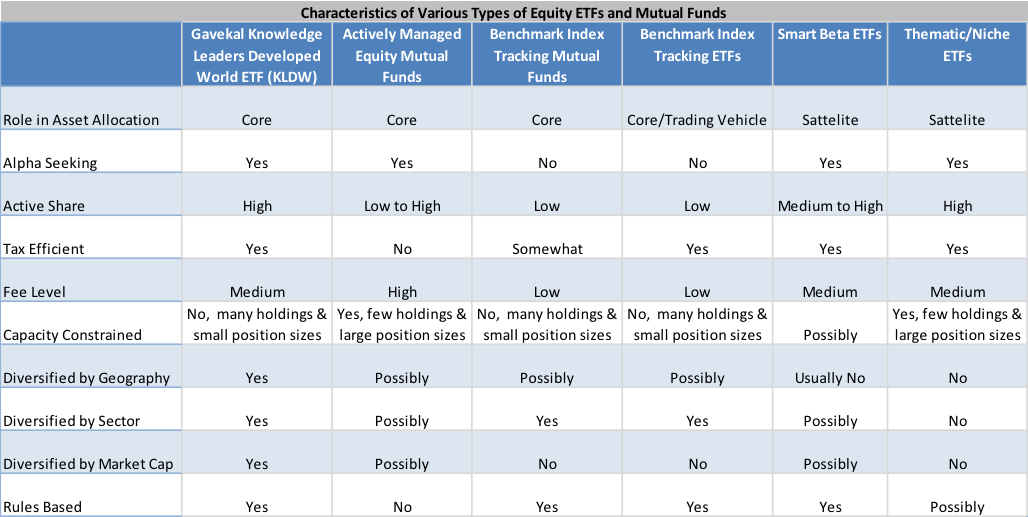

Let’s begin by isolating the distinctive characteristics of the various types of ETFs and mutual funds to equip fiduciaries to determine which types of vehicles most adequately serve the client’s best interest in the context of asset allocation. In our analysis, the change in the fund rating environment may help shine a spotlight on preferable elements of ETFs, making clear that in some cases an ETF could suit a client’s best interest more appropriately than a mutual fund.

The below table summarizes some of the key features associated with the most widely used classes of equity mutual funds and ETFs. The unique characteristics of each class of fund define its most appropriate place in the asset allocation. In general, equity funds that are tax-efficient, have low-to-medium fees, are not capacity constrained, and are diversified may be best used as core allocations. Conversely, equity funds that are tax inefficient, have medium-to-high fees, are capacity constrained, or are undiversified may be best used as satellite allocations due to possessing one or several deficiencies, or niche exposures. Furthermore, the performance goal of the fund classes should be considered, as well as whether or not that particular vehicle is operating in a way that allows it to achieve its goal. For example, if a fund class is alpha-seeking (it seeks to outperform the market on a risk-adjusted basis), it should also have high active share (a measure of how different a portfolio is relative to its benchmark), since high active share is a prerequisite to outperformance.1

Source: Gavekal Capital. These are the opinions of Gavekal Capital. See disclosures for further information on differences between ETFs and mutual funds.

1Martjin Cremers and Antti Petajisto, “How Active is Your Fund Manager?” March 31, 2009.

Each class of fund has a most appropriate place in the asset allocation and that in some cases mutual funds can be replaced with similar ETFs that have more acceptable features. Index-tracking ETFs can be used as substitutes for index-tracking mutual funds because the features and goals are typically identical except that ETFs will generally not distribute a capital gain on which taxes must be paid. Actively managed mutual funds possess several unfavorable characteristics including being tax inefficient, having high fees and being capacity constrained. In addition, many of them have low active share, which hinders their goal of outperformance(source:Morningstar). Some unique ETFs, like diversified smart beta ETFs, seek to correct for those deficiencies and have the same goal of outperformance. These ETF scan be used as substitutes for actively managed mutual funds as a core allocation. Smart beta and thematic/niche ETFs are generally tax efficient, but many of them are capacity constrained or undiversified and thus may be best used as satellite assets. In addition, some thematic/niche ETFs lack a completely defined rules-based process, which calls into question repeatability.

How ETFs and Tax Analysis Can Help Stack the Deck in Your Client’s Favor

Next let’s analyze the tax efficiency of ETFs relative to mutual funds. Below we describe the mechanics of the tax efficiency of ETFs and provide a real world example of the wealth compounding that accrues to ETF investors relative to mutual fund investors. The end result is that in some cases, the tax efficiency of ETFs may lead to an ETF serving clients’ best interests more efficiently than a mutual fund with a similar performance goal.

It’s common knowledge among investors that ETFs are tax efficient, but the underpinnings of the tax efficiency are rarely discussed. The primary reason ETFs are tax efficient is that many do not realize capital gains within the portfolio. Conversely, a preponderance of mutual funds do realize capital gains within the portfolio. So why is the realization, or not, of capital gains so important? Net realized capital gains in a mutual fund or ETF portfolio must be distributed to shareholders at least annually. Shareholders must then pay taxes on the amount of short and long-term gains that have been distributed to them, at the applicable tax rates. The act of paying taxes on annual capital gains and income distributions necessarily reduces the principle value of the investment and with it the rate at which the principle is permitted to compound through time.

How ETFs Avoid Realizing Capital Gains

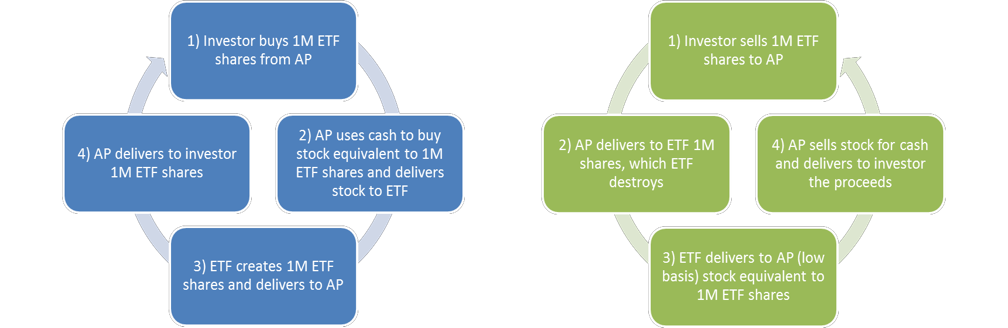

One unique feature of ETFs relative to mutual funds is that shareholders do not transact directly with a fund, but rather with an independent third party called an “authorized participant” or AP. It’s useful to think of the AP as a stock broker who acts as the middleman between the shareholders of the ETF and the fund itself. In the case of a purchase order, the AP interacts with the shareholders by exchanging ETF shares for cash. But, the AP being just a middleman doesn’t usually have many shares in inventory and must obtain them from the fund. To do so, the AP uses the cash from the investor to buy a predetermined basket of stocks – called a “creation basket” – corresponding to the holdings of the ETF, and then exchanges with the fund the creation basket for newly created shares of the ETF, called a “creation unit.” Finally, the AP delivers those shares to the investor. The process is called the “in-kind creation” process.

Fig. 1: “In-kind creation” process Fig. 2: “In-kind redemption” process

The “in-kind redemption” process, is at the heart of tax efficiency of ETFs. Readers should note that capital gains in comingled investment vehicles are usually generated from one of two actions: the portfolio manager having to sell stock to raise the necessary cash to meet redemptions and the portfolio manager selling stock to rotate/rebalance the portfolio. When an investor in an ETF decides to redeem his or her shares for cash, stock must be sold. Just like the in-kind creation process, the AP is responsible for carrying out the cash transaction, this time by selling stock to raise cash for delivery to the investor. To do so the AP must first obtain the stock from the fund itself by exchanging the investor’s redeemed ETF shares (which are subsequently destroyed) for a creation basket of equivalently valued stock. The AP can then sell the stock on the open market and deliver the cash proceeds to the investor.

The most important part of the in-kind redemption process is that the ETF portfolio manager may deliver to the AP its lowest cost basis creation basket, which is the basket with the largest unrealized capital gain. Because the AP is executing the cash sale and not the fund itself, the fund never must realize a capital gain to meet redemptions and the cost basis of the fund is simultaneously raised.

The repeated process of in-kind redemptions ensures that the ETF’s portfolio never accrues large unrealized gains because low basis stock is periodically recycled out of the portfolio in a tax-exempt way. This is also important to the tax efficiency of ETFs, because quarterly or semiannual rebalancing trades are actually executed by the fund in the cash market, and the resulting cash sales trigger realized gains and losses. In general, good portfolio management technique can ensure that portfolio level net realized capital gains are neutralized or substantially mitigated.

Capital Gains Taxes and the Impact on Wealth Compounding

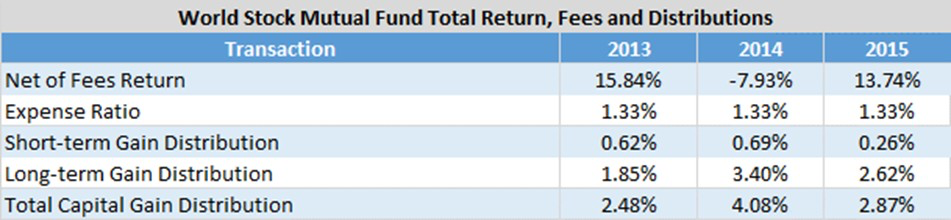

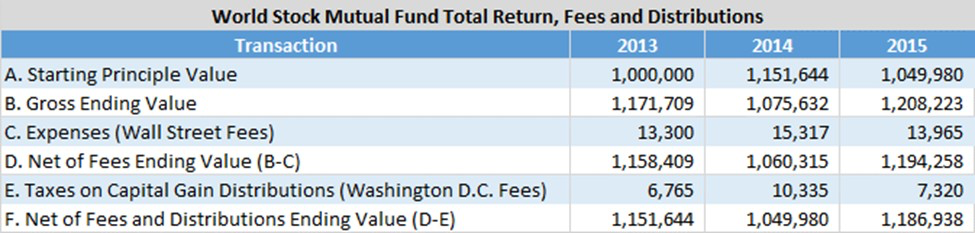

Let’s look at an actual example of how taxes can impact wealth creation over time. Over the trailing three years the Morningstar World Stock mutual fund category has returned 15.84%, -7.93% and 13.74%, respectively. Fund expenses were 1.33%, and total long and short-term capital gain distributions ranged from 2.5% to 4.1%.

Source: Morningstar, Gavekal Capital

As the next table below depicts, a $1M investment in 2013 would have netted an investor $187K by 2015, assuming a 20% long-term capital gain tax rate and a 39.6% short-term capital gain tax rate. An investor’s net return is of course the gross return, less fund expenses (Wall Street’s take) less taxes paid on capital gains distributions (Washington D.C.’s take).

Source: Gavekal Capital

Not bad for three years, right? Here’s the kicker: a deeper analysis of the division of gross returns reveals who’s really getting paid, and a big chunk is not going to the investor. Yes, a $1M investment would have yielded nearly $187K in gains, but Wall Street also collected nearly $43K in fees and the federal government took a cool $24K. To put those numbers into perspective, $43K is about the value of a brand new 2017 Audi A6 and $24K is about the value of a brand new 2017 Toyota Prius.

Source: Gavekal Capital

At the end of the day the investor accrues only 74% of the total return, but they are taking nearly all the risk. The fund issuer has some level of business risk, but the federal government bears zero risk and yet Washington D.C. takes almost 10% of the pie. Further to this point, because fees and taxes on distributions are a constant while returns can be either positive or negative, Wall Street and Washington D.C. get paid no matter what, even if the investor loses money, so long as the fund makes distributions.

Could Prospective Capital Gains Distributions be Going Up and Returns be Going Down?

One’s assumptions for the level of prospective forward returns and capital gain tax distributions are a function of at least several variables: stage of the business cycle, market valuations and interest rates. As the business cycle matures and the stock market appreciates, mutual funds are forced to sell low basis stock (with high embedded capital gains) to meet redemptions or to rebalance the fund. This necessarily implies higher levels of capital gain distributions, especially as tax loss carry forwards from the financial crisis are exhausted. In addition, the historically high level of stock valuations and the low level of interest rates suggests that the bulk of market appreciation must now primarily be a function of higher earnings. These three variables suggest that future capital gains tax distributions may become elevated and future returns mutated relative to history. The net result would be an even greater portion of an investor’s gross return accruing to Wall St. and Washington D.C. given the inflexibility of these two entities’ “fee structures.”

How ETFs Can Help

Luckily, ETFs in general have lower fees than mutual funds (the average fee for Morningstar’s World Stock ETF category is only 0.42%), but also do not generally distribute any capital gains due to the features described above. Indeed, average total distributions in the Morningstar World Stock ETF category were only 0.05% for the last three years. Eliminating Washington D.C.’s high fee from the equation allows for greater wealth accumulation to the investor, as the above real world example showed. On an after-tax basis, the deck is stacked firmly against the mutual fund, which in some cases may contribute to an ETF being the asset that most aptly serves clients’ best interests.

How to Buy ETFs: Everything You Need to Know About Trading and Liquidity

In this section, we discuss how to trade ETFs optimally in client portfolios. We’ll also debunk common fears, uncertainties and doubts about issues of trading and liquidity that may stand between financial advisors and the potentially superior outcomes ETFs may deliver.

ETF Prices are Not Subject to the Same Supply and Demand Dynamics as Stocks

ETFs are basically “mutual funds that trade like stocks,” right? Wrong! This simple analogy is responsible for a tremendous amount of confusion about the mechanics of ETF trading. What is true is that ETFs, like mutual funds, are open ended vehicles, meaning there are not a fixed number of shares. Unlike mutual funds, ETFs offer liquidity continuously throughout the trading day as opposed to just once at the closing NAV. Importantly, the open-ended nature of ETFs ensures that ETF prices are not subject to the same supply and demand dynamics that dictate the price of a stock. This is because shares are created and redeemed as demand and supply presents itself in the marketplace. The net result of this structure is that an ETF’s NAV and price are primarily dictated by the value of the underlying holdings, not the demand or supply of ETF shares.

ETF Volume and Market Cap are Poor Indicators of ETF Liquidity

Similarly, because volume and market capitalization are often used to gauge the liquidity of a stock, there is a common misunderstanding that these metrics play an important role in the liquidity of ETFs. This is untrue. The liquidity of most ETFs is primarily a function of the liquidity of the underlying holdings, not ETF volume or market cap. The most useful measure of the liquidity of the underlying holdings of an ETF is called “implied liquidity” and is published daily by Bloomberg for most equity ETFs. Implied liquidity is the single day dollar value of flows into or out of an ETF that could occur without the ETF exceeding 25% of the average daily volume of the least liquid stock in the fund. In other words, as cash comes into the fund and more shares of the underlying holdings are purchased, implied liquidity tells us the level of single day flows that the fund could sustain without pushing around the value of the underlying holdings, and by extension the value of the ETF itself. The interesting aspect about the implied liquidity of ETFs is that there is literally no relationship between either turnover (trading volume multiplied by price) or market cap.

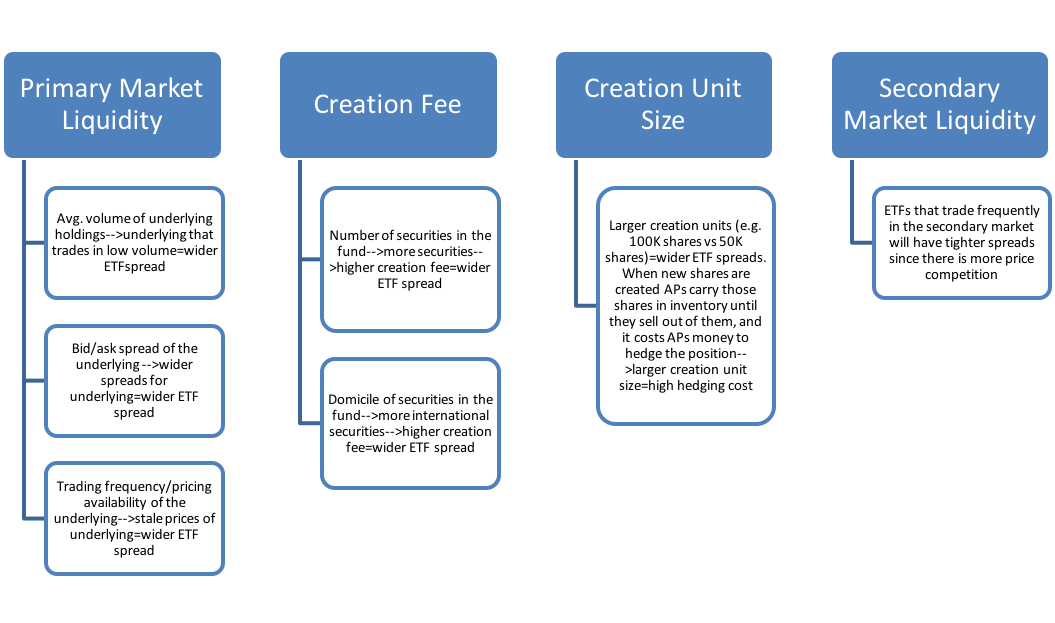

What about Bid/Ask Spreads?

The bid/ask spread is a measure of execution costs and a function of a number of complicated factors. The graphic below lists some individual factors that affect each variable of the bid/ask spread, as well as a list of important definitions. Just like ETF liquidity, the bid/ask spread of ETFs bears little, if any, relationship to either turnover or market cap. Indeed, using the largest 20 World Stock ETFs as an example, we observe a -27% correlation between turnover and bid/ask spread and a -20% correlation between market cap and bid/ask spread.

Factors that Influence ETF Bid/Ask Spreads

How do I Ensure Best Trade Execution for my Clients?

ETF trade execution is a function of at least three variables: market impact, transaction costs, and timeliness. Investing in ETFs with high levels of implied liquidity increases the likelihood that even orders of enormous size will not have a market impact on the underlying holdings of an ETF, and by extension the ETF itself.

Choosing ETFs with tight spreads can help to mitigate a substantial portion of transaction costs. Readers should note that ETF spreads have a tendency to be wider during the first and last fifteen minutes of trading as APs open and close their books, so trading during these periods should be avoided whenever possible.

Finally, having the order filled in a timely manner reduces the risk of market movements adversely affecting the execution price. Here we draw a distinction between timely order execution and order urgency and suggest that investors use limit orders, rather than market orders. Limit orders usually get executed within several minutes and reduce the risk that an order gets filled at an unfavorable price.

Conclusion

As ETFs likely gain even greater acceptance in the marketplace due in part to Morningstar’s merging of ETFs and mutual funds into the same peer group, it is important that financial advisors have a keen understanding of the mechanics of ETF trading.

In general, there is a broad based misconception that volume and AUM are important factors dictating the tradability, liquidity and/or spreads of ETFs. In reality, the factors that drive ETF liquidity and spreads have more to do with the construction and portfolio management of the product than either volume or AUM. Instead of focusing on volume and AUM of ETFs, investors should gauge liquidity by using the implied liquidity calculation, and they should judge execution costs by observing the average bid/ask spread percentage. Choosing ETFs with high levels of implied liquidity and tight spreads generally results in excellent execution. With the understanding that some of the data items mentioned in this writing may not be readily available to all advisors, we want to be a resource to our clients and are happy to consult with advisors upon request.

We hope the Gavekal ETF Tool Kit series was informative and provided useful tools to fiduciaries amid a changing investment landscape with the promotion of ETFs to the big leagues. It should be clear that ETFs have a place in the asset allocation and in many cases may offer superior alternatives to mutual funds. Please don’t hesitate to contact us with questions about ETFs or assistance with implementing an ETF strategy.

This article was originally published as a 5-part series and included analysis of our ETF relative to each topic discussed. For compliance reasons, this extended version of the article is available to institutional investors only. If you’d like to receive it, please email us at [email protected].

© 2015 Morningstar, Inc. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

The differences between ETFs and Mutual Funds include: ETFs are traded on major stock exchanges, and their prices will fluctuate throughout the day. Mutual funds are priced only once a day. ETFs carry an unavoidable cost called the bid-ask spread which is the difference between the price a buyer is willing to pay (bid) for a security and the seller’s (asking) price. Often times mutual fund’s have purchase and redemption fees as part of their transaction costs. An ETF can be bought for the cost of a single share, which can vary throughout the trading day. Mutual fund’s typically have a minimum investment amount. In regards to transparency, ETFs generally disclose holdings daily whereas mutual funds are only required to disclose holdings quarterly.

The information contained herein is provided for informational purposes only and should not be regarded as an offer to sell or a solicitation of an offer to buy the securities or products mentioned. The strategies discussed in the presentation may not be suitable for all investors. Gavekal makes no representations that the contents are appropriate for use in all locations, or that the transactions, securities, products, instruments or services discussed are available or appropriate for sale or use in all jurisdictions or countries or by all investors or counterparties. PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

Definitions

Active Share is the percentage of stock holdings in a portfolio that differ from the benchmark index. Active Share determines the extent of active management being employed by managers: the higher the Active Share, the more likely a fund is to outperform the benchmark index. Researchers in a 2006 Yale School of Management study determined that funds with a higher Active Share will tend to be more consistent in generating high returns against the benchmark indexes.

Alpha is a measure of the portfolio’s risk adjusted performance. When compared to the portfolio’s beta, a positive alpha indicates better-than-expected portfolio performance and a negative alpha worse-than-expected portfolio performance.

Authorized participant (AP): The middle man between the ETF shareholders and the ETF itself. The AP, which can be thought of as market maker, is responsible for providing ETF liquidity continuously by quoting bids to buy and sell ETF shares every several seconds. Further, the AP is responsible for carrying out purchase and sell transactions of the underlying ETF holdings on behalf of the ETF. The AP exchanges with the ETF the basket of stocks in which it transacts for shares of the ETF.

Creation unit: The prospectus-specified minimum number of shares of an ETF that can be created or redeemed by the ETF in one instance. For example, if an ETF has a 50,000-share creation unit then it must create or redeem shares in multiples 50,000.

Creation basket: The pre-specified portfolio of securities (and share quantities) that the AP purchases or sells on behalf of the fund in exchange for creation units.

Creation fee: The transaction costs borne by the AP each time it purchases or sells a creation basket. The creation fee is the same regardless of whether the AP transacts in one unit worth of basket securities or 10 units. For example, if a creation fee is $3,500 the AP will pay $3,500 to the ETF custodian regardless of whether it purchases the quantity of shares equivalent to one creation unit or 10 creation units.

Primary market liquidity: The ultimate liquidity ETF shareholders have access to as APs buy and sell creation baskets on behalf of the fund. This is the liquidity of the underlying holdings.

Secondary market liquidity: Liquidity of the ETF between current shareholders of the ETF. This is a measure of how frequently an ETF’s investors trade the ETF amongst themselves.

© GaveKal Capital

Read more commentaries by GaveKal Capital