Capitalism and democracy work together to power economic growth and sustain our standard of living; capitalism, with all of its faults, is still the best generator of investment and human capital in the world. Years from now, when we look back on 2017, we expect to find that Donald Trump’s presidential election underscored a profound shift in the political ideology of our time, which in turn impacted our democracy, economy, and our capital markets.

We expect Donald Trump will exercise the office of the President of the United States differently than any other U.S. President. Already, based on his direct involvement in issues such as the cost of manufacturing Air Force One with Boeing, the cost of military planes with Lockheed Martin, jobs in Indiana with United Technologies, political bureaucracy and task forces will be secondary to confronting the issues and direct negotiation. While we are admittedly not sure what impact this will have on the financial markets, we expect that there will be periods where investors are surprised with heightened volatility.

We believe the key drivers to economic growth and price movements in financial assets for 2017 will be regulatory and tax reform, fiscal stimulus and a marginal shift in monetary policy toward higher interest rates. The domestic economy still shows imbalances and is supported by an aggressive asset purchase program that has kept interest rates near historic low levels, stifling capital investment and hurting savers. Banks play an important role in our financial system as the primary facilitators of credit. Incentivizing banks to extend credit to small business is critical to sustained economic growth. By lowering the risk for entrepreneurs to start businesses, we will incentivize business growth, create jobs, and broaden the tax base. Ultimately, small business creates jobs. We expect to see a shift in the domestic agenda, where a focus on structural reform will allow for increased bank lending to small business which, in turn, will increase business formation and job creation.

Also, the shape of regulatory and tax reform next year will impact opportunities for investors. There appears to be a consensus around lowering corporate taxes which will have a direct impact on profit margins. In addition, any tax repatriation will help spur investment capital, share repurchase, and dividend distributions for shareholders.

The larger risks to domestic growth are from global forces outside of the United States. These include the growing populism in Europe and the credit bubble in China. While their direct impact on the U.S. economy may not be readily apparent, to the extent that capital flows are impacted, it will effectively stifle risk taking and capital investment.

Investing is about managing risk, not just taking risk. With the Federal Reserve buying bonds in the open market, the central bank is effectively manipulating and distorting the price of risk for investors. Since the economic recovery is still unbalanced, we believe there is a natural ceiling to how high interest rates will move next year. Any movement to lower taxes—both corporate and individual—will push municipal bond yields higher as banks and other investors reduce their holdings. This could create a wonderful buying opportunity for investors.

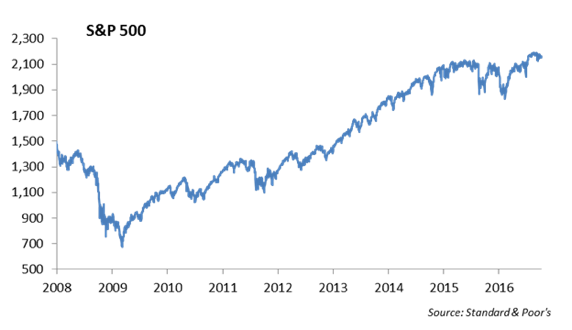

By some measures, equities appear overvalued heading into the earnings season next month. We are in that camp. We favor domestic stocks over developed and emerging-markets stocks next year. Small-cap stocks will likely outperform large-cap stocks. With higher interest rates and the potential for thoughtful regulatory reform, we favor an overweight to financial, industrial and technology stocks. Additionally, the repatriation of large cash balances will create opportunities for some global companies for capital investment and share repurchases.

At the end of the day, the equity market and the bond market are still being supported by the monetary policies of the Federal Reserve. We do not expect the Federal Reserve will be in a position to exit those policies over the next four years. With a pro-business agenda moving into the White House next year, we are cautiously optimistic for investment in domestic equities.

The Economy

While the economic recovery since the Financial Crisis is one of the slowest ever recorded, the domestic economy has been showing signs of improved strength over the second half of 2016. The US economy, measured by growth in Gross Domestic Product (GDP), grew at roughly 1.6% in 2016. We would expect growth to improve to 2.6% in 2017 depending on the fiscal stimulus the Trump administration is able to put forth.

We expect there will be initial excitement around the stimulative impact of rolling back Obamacare and Dodd-Frank, which will provide some optimism around economic growth. Ultimately, we believe there are two key initiatives required for sustained economic growth which are increased lending to small business and improvement in the labor market.

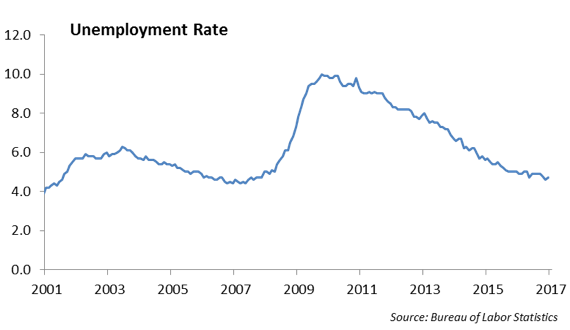

U.S. households are facing challenging times. Clearly, over the past several years, employment opportunities have grown and the unemployment rate is now at 4.7%. But, while the economy has produced 2.2 million jobs in the past year, these jobs are largely lower paying service sector jobs. The result is that wage growth has been slow and households have not been able to keep up with the rising cost of living. With wage growth hitting 2.9% last month, we are now beginning to see signs of wage growth in the economy. We are now seeing wage pressure across all income levels. According to a recent release from the Economic Policy Institute, there are now twenty states with proposals to increase the minimum wage in 2017.

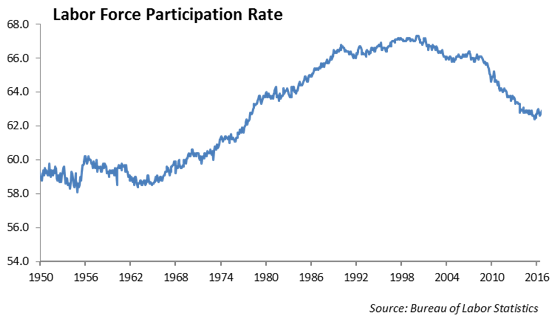

One of the structural problems in the labor market is the low labor force participation rate. During the Financial Crisis, the economy lost over eight million jobs. As individuals have grown frustrated in finding new employment, people ceased looking for work. The result is the labor force participation rate dropped to its lowest level since 1978.

In addition, productivity growth has remained stubbornly slow. In spite of advances in technology which have helped to make corporate America more efficient, actual economic output appears to be moving in direct correlation with the number of hours people put in, rather than increasing as we would have expected.

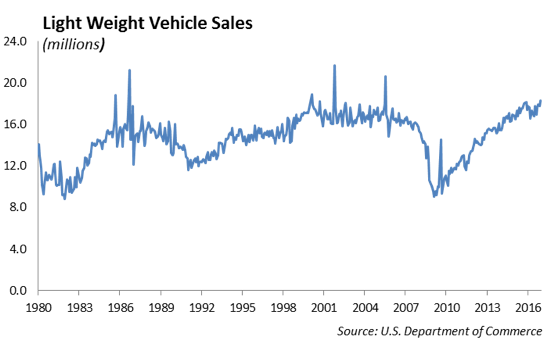

The bright spot in the economic recovery has been manufacturing. The auto industry has produced record light-vehicle sales in 2016 with 18.3 million units. However, after seven consecutive years of consistent growth, inventory buildup and heavy discounting in the fourth quarter of 2016, future sales growth from these levels appears challenging.

Monetary & Fiscal Policy

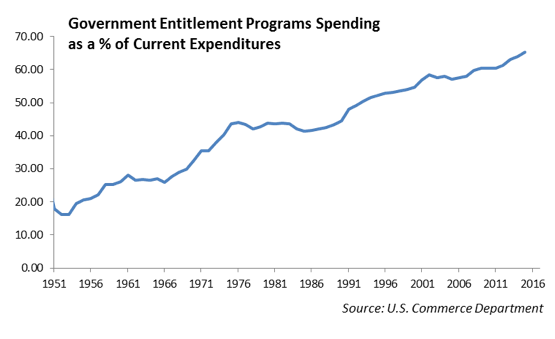

Our federal government is spending more than we are taking in. We expect to see tax reform this year which will lower corporate taxes. The hope is that we can sustain tax revenue through more robust economic activity. Yet, we have not addressed entitlement spending. Congress is still avoiding the political debate around our entitlement programs and whether it should be the government’s role is to continue to support and grow these programs. Entitlement programs have grown to $1.84 trillion per year since 2000 and represent over 60% of expenditures. Trump got elected, in a large part, by avoiding dealing with this issue. Speaker of the House Paul Ryan considers fixing the problem of entitlement programs a major issue.

So, the challenge that president-elect Trump will face is to spur economic growth while at the same time balancing the budget and allowing interest rates to move higher. We have been of the view that the economy desperately needs a fiscal stimulus initiative to work alongside of the simulative monetary policy in order to move economic growth above its anemic levels of the past several years. Fiscal stimulus will do more to help increase global demand and employment. Monetary policy does not create jobs, companies and government create jobs. We expect that the Trump administration will sacrifice any foreseeable improvement on the fiscal position of the United States for increased debt to fund fiscal stimulus.

We expect that we are approaching the apex of quantitative easing and its ability to impact economic growth. As the Federal Reserve contemplates higher interest rates, the question becomes what to do with the $4.2 trillion bond portfolio on its balance sheet. This bond portfolio represents the cumulative purchases from its three asset purchase programs initiated as a result of the Financial Crisis. While the Fed continues to reinvest coupon and prepayment cash flows, we expect the next move will be the release of cash flow into the market. This will signal the initial unwinding of this massive portfolio. However, under this new monetary regime we are operating under, we do not expect asset purchases in the open market as a tool to manipulative the level of interest rates will go away. It has proven to be a powerful tool and we believe it is here to stay.

Europe

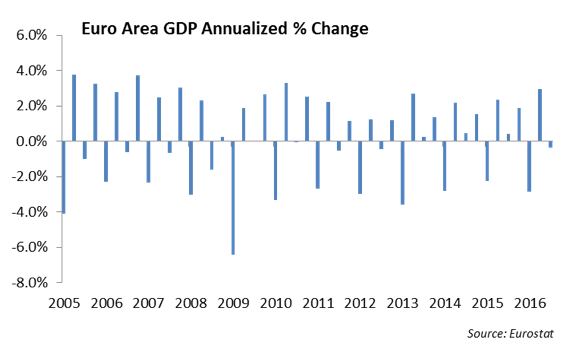

In spite of the Brexit vote, the growing populism movement that has destabilized European governments, and problems in its banking sector, the recovery in the Eurozone economy has remained on course. Unemployment across the region declined to 9.8% which is the lowest level since July of 2009 while Germany’s industrial production increased by 0.4% in November building on a solid October. In addition, purchasing manager surveys and business sentiment are also on the rise.

As the Federal Reserve’s policy has shifted toward increasing interest rates, the European Central Bank recently voted to extend its €1.2 trillion quantitative easing program to December 2017 but reduced its monthly purchase from €80 billion to €60 billion. Monetary stimulus alone will not boost economic growth in the Eurozone given the structural problems that the European Union faces. In December, the euro reached its lowest level against the US dollar since 2003 falling to $1.0352 and is down 8.8% from its peak in May. We expect the euro will hit parity with the US dollar in 2017.

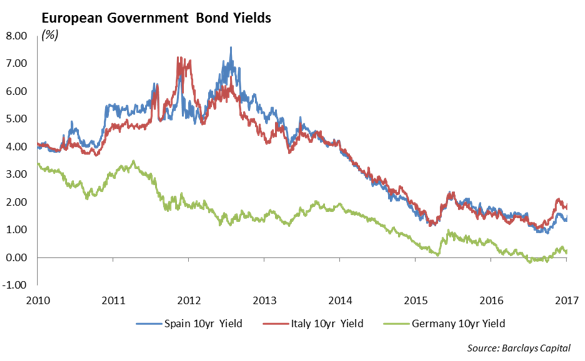

Our focus is on Italy which is on its fourth government in six years. In December, the Italian people voted against a change in the constitution which would have simplified their government structure put in place following World War II. As a result, Italian Prime Minister Matteo Renzi has voluntarily stepped down and Italy is now forced to put a new government in place.

At the same time they are facing a bank crisis as two of the major Italian banks, UniCredit SpA and Monte dei Paschi di Siena SpA, are stacked with problem loans and are on the brink of collapse. Italy’s largest bank, UniCredit SpA, plans to shed thousands of jobs and raise €13bn in the country’s biggest share issue in a bid to shore up its reserves and boost profits by the end of the decade. Yet, it is the imminent failure of Italy’s third-largest bank, Monte dei Paschi di Siena SpA, that is finally bringing the country’s long-festering banking crisis to the center of the European Union’s focus. Italy’s financial woes have been decades in the making. Cronyism, poor lending standards and an extended recession produced over €

350 billion in bad loans. Successive governments avoided a day-of-reckoning, in part because European bank rules would require them to impose losses on creditors which Italy avoided. We believe Italy remains the epicenter of Europe’s problems for 2017.

However, we expect to see improvement in 2017 with a weaker euro and some improvement in economic growth. As the Eurozone economy improves, we expect to see some upward pressure on interest rates which have been trading near historic lows this past year. Unemployment rate in countries like Spain are showing improvement which will help consumption. There has been marked improvement in the banking sector which will help loan growth and credit expansion. We expect European equities will outperform US equities in 2017. Long term, we still believe the euro will be reconstituted as the co-op currency faces increasing challenges in its current form. The growing populist movement across Europe may impact elections this spring where populist candidates are on the ballots including France, Germany and the Netherlands.

China

China’s pace of economic growth continues to slow and the central government’s tool kit to stimulate growth appears to be having less impact. We expect growth in China to come in below 6.5% this year. China has become a powder keg for the global economy. Over the past several years now we have seen the growing leverage in their economy, we have heard the stories of the government cracking down on speculators and short sellers, and we have watched the capital flows out of China and into other countries including the United States. We see the empty buildings in their cities. Everything we see tells us that this is a bubble that is ready to burst. But, we do not know when. China is still the largest buyer of commodities such as steel, iron ore and copper. Any serious pull back from China’s purchase of commodities will have a meaningful impact on the global capital markets. It’s enough for us to be concerned. Combined with dismal growth in Brazil and India, global demand from emerging market economies will likely remain slow.

Investment Strategy

Our general orientation is to not change our asset allocation at this point. We are coming into the year with volatility in equities at low levels and valuations at high levels. With a more pro-business agenda coming with the new administration, we expect there are more opportunities in domestic equities, specifically energy, financials, transportation and technology. We are focused on earnings and valuations. Earnings grow for three reasons: revenue growth, margin improvement and increased leverage. We are believe that tax reform and reduced regulation will support margin improvement; however, leverage and top line growth may still be missing.

We also believe there is more opportunity in small and mid-cap stocks over large cap this year. At the same time, horizon returns in domestic large cap equities will be likely be mid-single digits and not a repeat of last year.

With OPEC cutting back production, we expect to see oil prices trade over $50 per barrel this next year. In turn, we expect to see expansion in the energy sector including drillers, exploration, field services and pipelines. In addition, we expect Trump to take a more passive regulatory approach to carbon emissions and fossil fuels which will help coal industry. This, in turn, will help the railroad and railcar leasing industries since rail is the primary means to ship coal in the United States.

The financial sector will show meaningful improvement as interest rates increase. Retail banking will show improved earnings growth as deposit growth and net interest margins improve. We have not seen the full impact of the rate rise in the fourth quarter through bank earnings yet. Also, life Insurance earnings will improve as earnings from portfolio investments grow.

Investments in the healthcare sector will likely prove more difficult next year. With the pull back of Obamacare, hospitals may show some margin improvement through efficiency gains. However, pharmaceutical and benefit management companies are in the political cross-hairs due to some egregious pricing practices which have hurt consumers. How this shakes out right now is not clear; however, it will impact earnings. Pharmaceutical is coming off a tough year with major drug test failures in front of the FDA for Bristol Myers, Eli Lilly and Abbott Labs.

We believe there is opportunity in investments in developed countries even with the uncertainty over the potential for restructuring of trade agreements. With the increased capital levels of the European banks, we expect any improvement in economic growth will help European equities.

Fixed Income

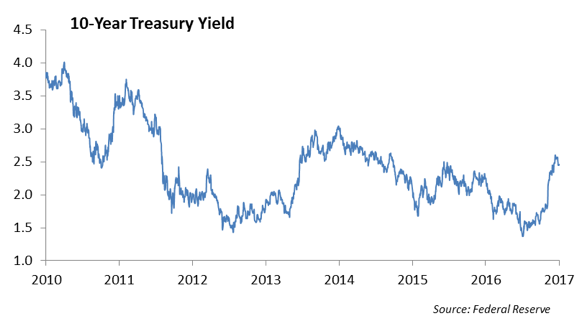

While there is a clear path to allow interest rates to move higher given the momentum in the economy, we believe there as a natural ceiling to how high domestic interest rates can rise. As long as the US dollar is strong relative to other major currencies, we will attract capital into dollars which, in turn will suppress interest rates. The yield on the 10 year US Treasury note increased 95 basis points during the fourth quarter of last year, a huge move in rates by historic measures. While we don’t expect to see that pace sustained, we do believe the trend toward high rates is real.

We expect corporate bonds to perform well in 2017. New issue activity will likely slow from previous years if foreign repatriation of cash is allowed for domestic companies. This cash will become the fuel for share repurchase programs and capital investment. We expect corporate credit should remain stable this year and defaults remain near historic low levels.

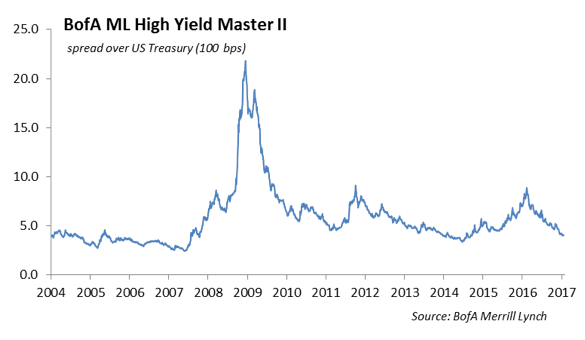

We still see value in the high yield market as corporate balance sheets remain strong and companies have recovered from the melt down in the energy sector last year. Solid BB rated credits in the five year area with 5% yields make some sense for income oriented investors. We like specific investments that are rated below investment grade in the energy, telecom, financial and manufacturing sectors.

We also believe there are opportunities in the hybrid securities market as interest rates push higher, particularly in preferred stocks which underperformed last year.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2017 Winthrop Capital Management

Read more commentaries by Winthrop Capital Management