Every great growth company hopes to make the transition from fast growth pioneer to sustainable growth blue chip. When the transition occurs, a grand divorce happens between the price-to-earnings (P/E) ratio and the future success of the business. What made us think of this was the annual forecasting dinner of the CFA Society of Seattle on the evening of January 19, 2017.

The keynote speaker was Amity Schlaes, a historian and writer. Her book, The Forgotten Man, provides one of the best historical accounts of the Great Depression and was a blessing to us back in the depths of the financial crisis. By her allowing us to understand what went on from 1929 through 1939, she helped us establish an optimism in the future that has been very useful since 2009.

During the dinner, the audience was asked to submit questions. My question was: “What is the difference between the RCA Corporation at the end of 1928 and Amazon and Netflix in early 2017?” This question naturally leads us to the following series of questions. How does total domination in a sector of the economy play out for the shareholders of the leading company involved? Are maniacal large-cap U.S. equity episodes and ultra-high P/E ratios worth the risk? Why should large-cap value stock pickers like Smead Capital care about what goes on with these market favorites?

RCA Corporation was the nation’s leading wireless communication company in the 1920s. They were the largest sellers of radios, the largest radio broadcasting company, and the most popular radio content provider of the era. As Governor Pappy O’Daniel said in the classic film, O Brother Where Art Thou, “We are mass communicating.” They had a complete monopoly on the main thing that Americans did to entertain themselves during leisure time.

My father was born in 1925 and told me many times about the radio shows he listened to and how important the radio was to society. RCA’s stock rose from $11 to $114 per share in the five years prior to the stock market crash in the fall of 1929; a 60% compounded return. It had never paid a dividend and at its peak in 1929 it traded at an astronomical P/E multiple of 72.1.1

The stock of RCA fell 95% from the market’s peak in 1929 to less than $5 share in 1932 at the bear market lows.2 However, nothing stopped the actual economic success of their business. RCA continued to be the dominant radio and wireless business in the U.S., and became one of the early leaders in the television industry as it emerged in the late 1940s and 1950s. In effect, at the company’s height of admiration in 1929, a grand divorce occurred between the economic viability of the radio business, RCA Corporation’s profitability, and the stock price.

Amazon has traded as high as $850 per share in the last year after trading around $170 five years ago. It has completely dominated online commerce in the U.S. and was the first mover and dominant player in cloud computing services. Amazon constantly seeks out new things to sell online to its army of customers, many of whom pay $99 per year for Amazon Prime membership to get their purchases delivered for free. The stock does not pay a dividend and trades at a P/E multiple of 185 based on last year’s profits.

Most analysts and investors who recommend owning Amazon shares base their enthusiasm on two theories. First, they both assume that Amazon will reap dramatically higher levels of profitability after they capture an immensely larger critical mass, henceforth, crushing enough of the retailing establishments with whom they compete. Second, investors dually believe that Amazon will end up with a hugely profitable share of a much larger cloud computing services business, and that its subsequent profit margins will still be very high despite competition from other companies like Microsoft.

Netflix has gone from $13.25 to around $137 per share in the last five years. They have revolutionized the delivery of movies and programming online to the delight of millennials, generation Xers, and baby boomer Americans alike. They have reduced the cost and hassle of watching movies and eliminated the need to watch advertisements, unless intentionally planted in the shows. Their stock trades at a P/E multiple of 346. Those who own and recommend Netflix do so under the belief that as Netflix grows to control a large enough portion of the worldwide entertainment flow, it will achieve profit margins that justify its monumental P/E ratio.

Will Amazon and Netflix reach the profit potential anticipated by its owners and enthusiasts? The history of RCA and other fast growth darlings of the past argues that it doesn’t make any difference whether they do or not.

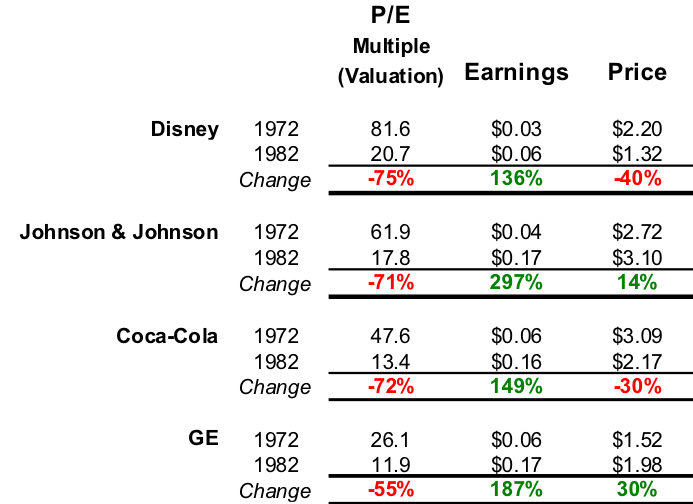

You can see from the chart above that the grand divorce for Disney, Johnson and Johnson, Coca Cola and General Electric occurred in the bear market of 1973-1974.3 These companies have succeeded for decades since and have never gone back to the high P/E ratios of the Nifty Fifty Era.

In doing the research for this piece, I ran into an article written in late 1997 about Microsoft (MSFT). In the aftermath of that article, Microsoft stock climbed the last two years of the tech bubble before it peaked in early 2000.

From 2000 to 2016 their profits grew from $.86 per share to an $2.75 per share. The stock hit $60 in 2000 and trades at $62.60 on the 19th of January, 2017. Microsoft went through the grand divorce in the year 2000 by falling from $60 per share on March the 10th of 2000 to $20.75 on December 20th. It traded below $30 in early 2013. RCA rebounded to $40 per share in the 1950s, but that was of little solace to those who bought it during the last three years while it was still married to its ultra-high P/E ratio.

All the glamorous growth stocks of the past once stood in the shoes now worn by Amazon and Netflix. Shareholders must be conscious of the upcoming grand divorce between share prices and the business success of the underlying company. Warren Buffett likes to explain this through the fairy tale, Cinderella. He says, “The party goes on until midnight and then it all turns into pumpkins and mice.” We believe it isn’t a question of whether the grand divorce occurs, but rather, a question of when. History argues that the remaining appreciation in these two issues could come at a huge potential long duration price to owners.

Why should large-cap value investors like Smead Capital Management care about the grand divorce in the stock price of glamorous stock market favorites? The grand divorce usually happens in one of two ways. Either investors lose confidence in all stocks (1929-1932, 1973-1974, 1987), or investors lose confidence in those stocks trading in a maniacally high P/E bubble (2000-2001). Therefore, it is important to understand that there are currently some unusually large risks at hand in the U.S. stock market. In a world of passive investing in mutual funds and ETFs, the speed at which the grand divorce happens and the damage it does to unsuspecting common stock investors could be shocking!

Warm Regards, William Smead

1 Source: http://www.gold-eagle.com/article/rca-1925-1929-and-microsoft-1993-1997

2 Source: http://www.worststockmarketcrashes.com/crash-of-1929/rca-stock-price-after-the-1929-stock-crash/

3 Source: Bloomberg

The information contained in this missive represents Smead Capital Management's opinions, and should not be construed as personalized or individualized investment advice and are subject to change. Past performance is no guarantee of future results. Bill Smead, CIO and CEO, wrote this article. It should not be assumed that investing in any securities mentioned above will or will not be profitable. Portfolio composition is subject to change at any time and references to specific securities, industries and sectors in this letter are not recommendations to purchase or sell any particular security. Current and future portfolio holdings are subject to risk. In preparing this document, SCM has relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources. A list of all recommendations made by Smead Capital Management within the past twelve-month period is available upon request.

© 2016 Smead Capital Management, Inc. All rights reserved.

This Missive and others are available at www.smeadcap.com

Follow us on Twitter @SmeadCap