We have a normal calendar for economic data. There will be important news will come from corporate earnings reports. Since this earnings season is part of an inflection point – the end of the earnings recession– it is special. That said, the uncertainty over policy change has market observers both divided and on edge. I expect the earnings news to get less attention than normal. With the queasy, uncertain feeling, the pundits will be asking:

Will policy uncertainty lead to greater stock volatility?

Last Week

Last week the economic news was strong, but with little reaction from stocks.

Theme Recap

In my last WTWA I predicted a close watch on earnings to see if these reports confirmed the improvement in economic data. There was plenty of attention to earnings, but not much on the economic strength theme. Pundits loved to discuss the various Trump appointees and speculate on the stock implications. At some point the market will refocus on the regular themes. For now – like it or not – the Trump effect is a big part of the daily discussion.

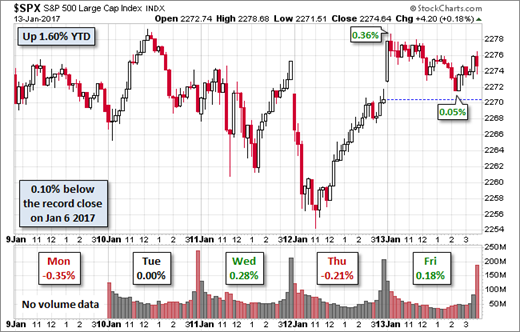

The Story in One Chart

I always start my personal review of the week by looking at this great chart from Doug Short. As has been the recent case, both the range and the weekly change were very small. Doug attributes the Friday pullback to an Inaugural Address that offered little for the wealthy. He offers more analysis in his commentary. (Personally, I do not find any of the moves big enough to merit discussion, but there was plenty of commentary).

Doug has a special knack for pulling together all the relevant information. His charts save more than a thousand words! Read his entire post for several more charts providing long-term perspective.

Personal Note

Since I will be enjoying a Winter weekend away with Mrs. OldProf and friends, I will probably not write next weekend. As always, I’ll be watching, and may post a brief update if it seems necessary.

The News

Each week I break down events into good and bad. Often there is an “ugly” and on rare occasion something very positive. My working definition of “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

This week’s news was again quite good—almost all positive. I make objective calls, which means not stretching to achieve a false balance. If I missed something for the “bad” list, please feel free to suggest it in the comments.

The Good

-

Industrial production rose 0.8%. This beat expectations of 0.6%, but the prior month was revised lower by about the same amount. This series is difficult to interpret in the short run.

-

Philly Fed improved to 23.6 versus the prior month 21.5. This is an exceptional gain for two consecutive months in a diffusion index. It handily beat expectations of 16 or so.

-

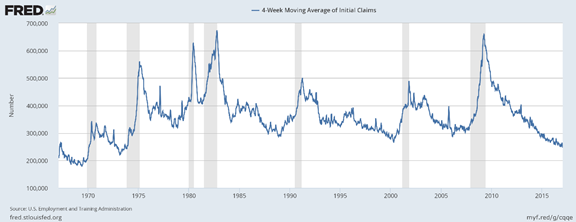

Initial jobless claims fell yet again. The series is now at the lowest level since 1973. To my surpriseamazement, some of the punditry is actually finding a way to make this into bad news!

-

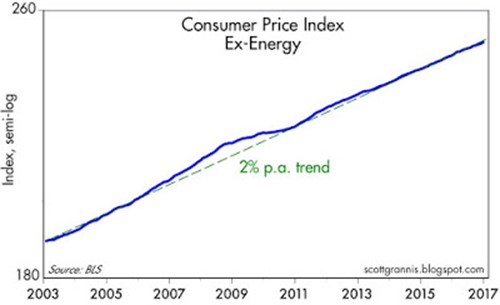

Inflation is higher. I understand that many view this as bad news. At some level, it would be. At a time when deflation (more dangerous and harder to fight) has been threatening, a modest rate of inflation is preferred. Scott Grannis has the story, and good charts on other data as well.

-

Homebuilder confidence remains strong. Calculated Risk, our go-to source on all things housing, notes that the reading was “below consensus, but another solid reading.” Anything over 50 indicates that most builders view conditions as good.

-

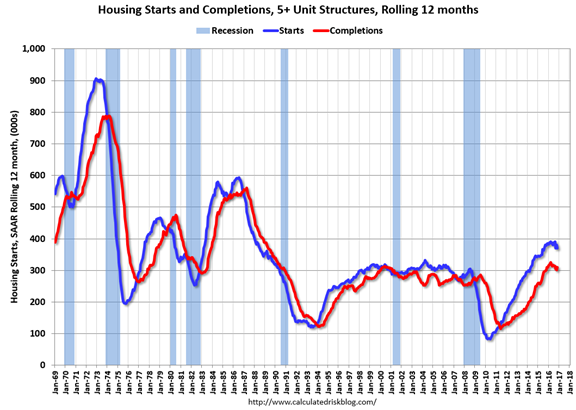

Housing starts showed a big increase, but mostly because of multi-family. The volatile series remains in the range Bill McBride predicted at the start of the year (4% to 8%). The actual was 4.9%, so the bottom end of the range. More encouraging is that multi-family was down 3.1% for the year while the gains came from the 9.3% increase in single-family.

The Bad

-

Building permits had a slight decline to a seasonally adjusted annual rate of 1,210,000. This is down 0.2% from last month but a gain of 0.7% over last year. I tend to place more weight on this series than most other analysts, so I watch it closely.

-

Earnings season began on a soft note. Both earnings and revenue surprises are below the long-term averages. Only 12% of the S&P 500 companies have responded so far, and there is specific sector concentration. I’ll save the charts until we have more data, but you can check for yourself at FactSet. Also, see specific company commentsfrom Avondale, which follows the conference calls.

The Ugly

California budgeting. I have criticized my own state (Illinois) so often. This week the award goes to California for a $1.5 billion “math error.” Put enough of these together and you eventually have real money. (Everett Dirksen).

The Silver Bullet

I occasionally give the Silver Bullet award to someone who takes up an unpopular or thankless cause, doing the real work to demonstrate the facts. No award this week. I welcome nominations from readers. As always, ZH is a fertile source of ideas. Write something!

We also published our annual review of winners. If you take a look at the excellent work reviewed (here and here) you will see the advantage of following these contrarian sources. You will be surprised at how much it can help your investing.

There was a popular recent post about “neglected topics.” The article highlighted the heavy hitters who basically control the agenda of what you see. I tried to respond here. I despair! I welcome suggestions about how to get more exposure for those who do great but unpopular work.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react. That is the purpose of considering possible themes for the week ahead. You can make your own predictions in the comments.

The Calendar

It is back to normal for the volume of economic data, but fewer of the most important reports.

The “A” List

- New Home Sales (Th). More strength expected in this important sector.

- Michigan Sentiment (F). Continued strength anticipated. Special interest in future expectations.

- Q4 GDP (F). The first estimate gets major adjustments, but still attracts plenty of attention.

- Leading Indicators (Th). Expected rebound from last month’s “No change.” Some swear by this report.

- Initial jobless claims (Th). How long can the amazing strength continue?

The “B” List

Fed speakers are still on the trail. Questions will probe the new political environment, with everyone trying to dodge.

Earnings reports will remain important. Early actions from the Trump Administration will capture attention, if only because few know quite what to expect.

Next Week’s Theme

It would be nice to have a clean turn to our regular analysis of economic data and earnings. I understand that many (including my readers) are tired of thinking about the Trump Effect. I sympathize, but it is not a good investment strategy. We need to think carefully about what is likely to work, and what isn’t. Since no one really knows what is going to happen (as I suggested a year ago,) the current dubious pundit forecast is more volatility. That will steal the spotlight next week. The key question will be:

Will uncertainty about policy changes lead to more volatility?

The basic positions are simple.

- Some see the new administration as negative for the market, and some see it as positive. This is frequently interpreted as more volatility.

- There are several policies on a “hit list.” How rapidly will policy changes occur? Higher volatility?

- Some speculate that the Presidential Inauguration will represent a market top. The sources look like a list of serial top-callers, but many are embracing the idea.

- Various worries are somewhat offsetting. Extreme possibilities do not always lead to major changes.

- President Trump may still prove different from Candidate Trump.

- There are already executive orders. What are the implications?

What does this mean for investors? As usual, I’ll have a few ideas of my own in today’s “Final Thoughts”.

Quant Corner

We follow some regular great sources and the best insights from each week.

Risk Analysis

Whether you are a trader or an investor, you need to understand risk. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update.

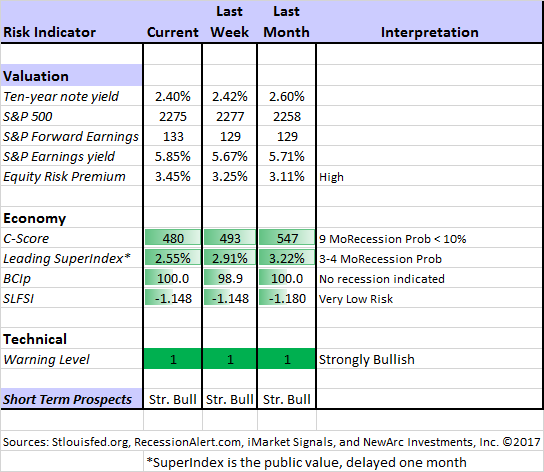

The Indicator Snapshot

Although dropping last week, the yield on the ten-year note has increased significantly since the election. This has lowered the risk premium a bit. I suspect much more to come. By this I mean that the relative attractiveness of stocks and bonds will continue to narrow.

The C-Score has also dropped. The relationship is not linear, and it remains in the “safe” zone.

The Featured Sources:

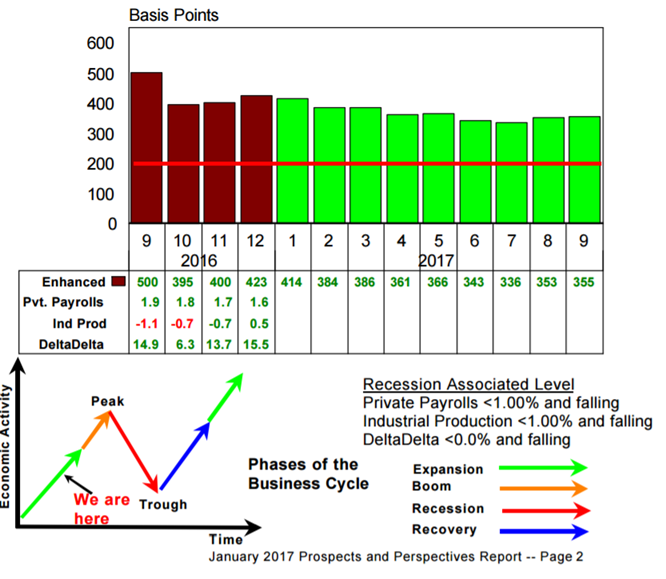

Bob Dieli: The “C Score” which is a weekly estimate of his Enhanced Aggregate Spread (the most accurate real-time recession forecasting method over the last few decades). His subscribers get Monthly reports including both an economic overview of the economy and employment. (see below).

Holmes: Our cautious and clever watchdog, who sniffs out opportunity like a great detective, but emphasizes guarding assets.

Brian Gilmartin: Analysis of expected earnings for the overall market as well as coverage of many individual companies.

Doug Short: The World Markets Weekend Update (and much more).

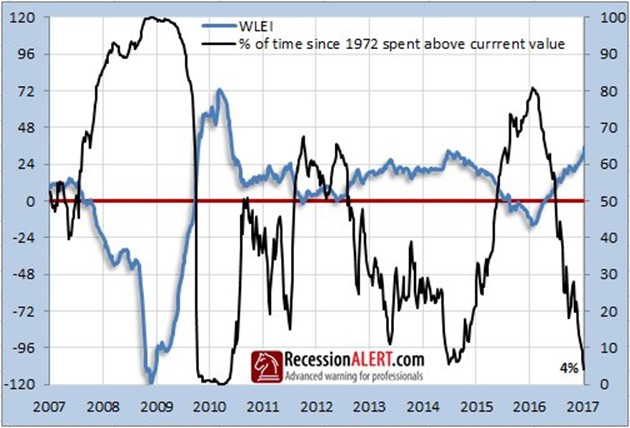

RecessionAlert: Many strong quantitative indicators for both economic and market analysis. While we feature his recession analysis, Dwaine also has several interesting approaches to asset allocation. Try out his new public Twitter Feed, the source of this interesting chart:

This illustrates the improvement in economic indicators – a consistent recent theme.

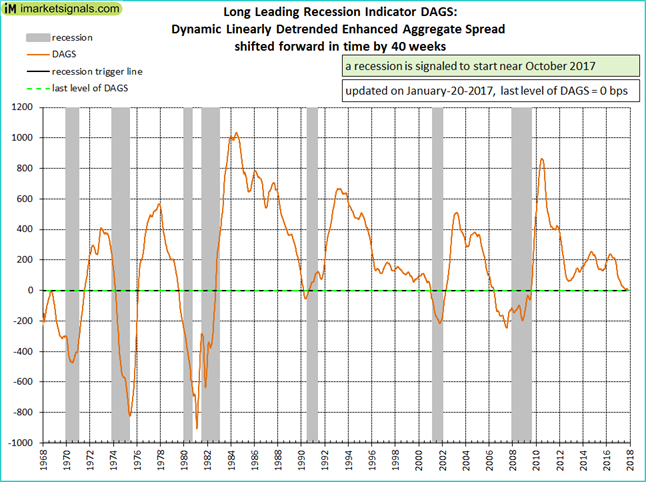

Georg Vrba: The Business Cycle Indicator and much more.Check out his site for an array of interesting methods. Georg regularly analyzes Bob Dieli’s enhanced aggregate spread, considering when it might first give a recession signal. Georg has been suggesting that the measure still shows a one-year led time. His most recent take has a wide time horizon, but an onset date of October (the chart below). Please note that Georg’s other indicators are still “friendly.”

The question is whether this improves over Dr. Dieli’s original concept, which has worked for decades in real time. He is quite open to new ideas, and is constantly questioning whether anything has changed in the key relationships he studies. Even before I saw Georg’s most recent work, I was planning to share this chart from Bob’s regular monthly update. I regard it as the single most important current concept for investors of all types.

A costly investor mistake has been fear, often incited by those with little knowledge and no track record. Stay tuned!

How to Use WTWA (especially important for new readers)

In this series, I share my preparation for the coming week. I write each post as if I were speaking directly to one of my clients. Most readers can just “listen in.” If you are unhappy with your current investment approach, we will be happy to talk with you. I start with a specific assessment of your personal situation. There is no rush. Each client is different, so I have eight different programs ranging from very conservative bond ladders to very aggressive trading programs. A key question:

Are you preserving wealth, or like most of us, do you need to create more wealth?

Most of my readers are not clients. While I write as if I were speaking personally to one of them, my objective is to help everyone. I provide several free resources. Just write to info at newarc dot com for our current report package. We never share your email address with others, and send only what you seek. (Like you, we hate spam!)

Best Advice for the Week Ahead

The right move often depends on your time horizon. Are you a trader or an investor?

Insight for Traders

We consider both our models and the top sources we follow.

Felix and Holmes

We continue with a strongly bullish market forecast. Felix is fully invested. Oscar is fully invested, but the sectors are somewhat less aggressive. The more cautious Holmes has taken some profits, but is still about 90% invested. The group meets weekly for a discussion they call the “Stock Exchange.” In each post I include a trading theme, ideas from each of our four technical experts, and some rebuttal from a fundamental analyst (usually me). There are always fresh ideas. You can also ask questions and have a little fun. Give it a try.

Top Trading Advice

Tweets activate algorithms! High frequency traders pounce on any piece of information. (MarketWatch). Is there a way to benefit? You cannot beat the HFTs once the news is out. You must either anticipate or react. Please also note that the fundamental news does not really matter. It is quite clear that the new administration will be using the Twitter as a bully pulpit, both issuing warnings and claiming credit for the responses. It is a new world for trading.

Are you making success into a habit? A trading journal helps on that front, as Dr. Brett Steenbarger explains. His near-daily posts are must-reads for every trader, and often for investors as well. This week he also inspired our Stock Exchange gang with this one. Whether your trading is close to our approach, you will find it helpful.

Those who join us in reading Brett Steenbarger’s regular posts will enjoy his appearance on Barry Ritholtz’s acclaimed MiB series.

Insight for Investors

Investors have a longer time horizon. The best moves frequently involve taking advantage of trading volatility!

Best of the Week

If I had to pick a single most important source for investors to read this week it would be Chuck Carnevale’s analysis of Broadcom Limited (AVGO). It combines all the many things that Chuck does so well – a great stock idea, a lesson in several types of fundamental analysis, and a tutorial on his first-rate market tools. I usually do not like videos since I can read fast. In this case I recommend that DIY investors grab a cup of coffee and watch the entire video. While Chuck’s tools allow for a lot of flexibility, his approach is very like what we use in screening our candidates. If you are not doing something like this, you should stick to ETFs!

Stock Ideas

Exxon Mobil (XOM) is buying up Permian Basin assets “on the cheap.” This may not show up in an immediate stock price change, but it is something I have been expecting. Investors should understand the long-term needs of big integrated oil companies, and the floor placed under reserves.

Where should you look? Eddy Elfenbein considers United States Lime and Minerals. (USLM). Eddy writes:

Fourteen years ago, USLM was going for $3 per share. Today it’s at $77. So how many analysts follow it? Zero.

The stock has a market cap of $425 million. I also have to say that I love that name.

Keep that in mind while considering this post from Eli Hoffman, CEO and Editor-in-Chief at Seeking Alpha. Starting with a WSJ article, he carefully explains the motives of many analysts.

I feel quite strongly about these ideas. We NEVER use sell-side research as the basis for ideas. In fact, it is a negative factor in our general rating system. Individual investors need a similar method. I also agree with Eli that Seeking Alpha provides plenty of grist for the mill. While I have my own methods for generating ideas, it is always a valuable checkpoint on the way.

Our trading model, Holmes, has joined our other models in a weekly market discussion. Each one has a different “personality” and I get to be the human doing fundamental analysis. We have an enjoyable discussion every week, including four or five specific ideas that we are buying. This week the dip-buying Holmes (who has been very hot) liked Fomento Economico (FMX) a distributor of soft drinks and an investor in the Heineken Group. I objected. In an action of man over model, or person over dog, or boss over worker, I vetoed the trade. Holmes has gone to Mexico (true!) for further investigation. We will be checking his expense account. FMX does not sell Margaritas!

Seeking yield?

How about Blue Harbinger’s latest CEF idea, Diversified Real Asset Income (DRA). This is another fund trading at a discount to NAV. I am always interested in Mark’s well-researched ideas and always curious about the reason for the discount.

Personal Finance

Professional investors and traders have been making Abnormal Returns a daily stop for over ten years. If you are a serious investor managing your own account, this is a must-read. Even the more casual long-term investor should make time for a weekly trip on Wednesday. Tadas always has first-rate links for investors in his weekly special edition. My personal favorite this week is the FT article about the six different investor personalities. There is a lesson in each!

Seeking Alpha Editor Gil Weinreich’s Financial Advisors’ Daily Digest has quickly become a must-read for financial professionals. Somewhat to my surprise, the topics are also especially relevant for active individual investors. They frequently join in the comments, adding to the value of the posts for both groups. Gil has several good topics, but I especially liked this treatment of goals-based investing. I have started following the author, Marshall Jaffe. This is a topic that every DIY investor should consider carefully. There is a lot at stake.

Watch out for…

Tweet targets. This company, a 14% loser, came into the sights a noted short-seller. There is an interesting dynamic here. The reputation of the source would have an immediate effect. Any “in the know” pals would be on board. There is plenty of money to be made, whether you have a short position before the announcement, or like the company and buy into the selling.

Final Thoughts

Despite the uncertain environment, volatility has been a matter for individual stocks. The overall market forces seem to have found a balance. I do not view volatility as a concern, and suggest caution to those using this as a hedge.

The improving economic data have not (yet?) shown up in the earnings reports. Perhaps it is because the improvement came so late in the quarter. I see more sources noting that earnings seem to be trailing the improving economic news.

There is plenty of temptation to link your investments to the electoral change. My base position is that you should not regard it as important, instead figuring out how to profit from the new policies. Be politically agnostic.

What I am watching.

A psychological element worth following is the improvement in business and consumer sentiment. This was also suggested in reports from the Davos world economic forum. Just as the pre-election negative environment weighed on the economy, confidence could also become a self-fulfilling prophecy.

Sentiment sometimes trumps the reality of economic data.

© NewArc Investments, Inc.

Read more commentaries by NewArc Investments, Inc.